SMM, June 10:

Metals market:

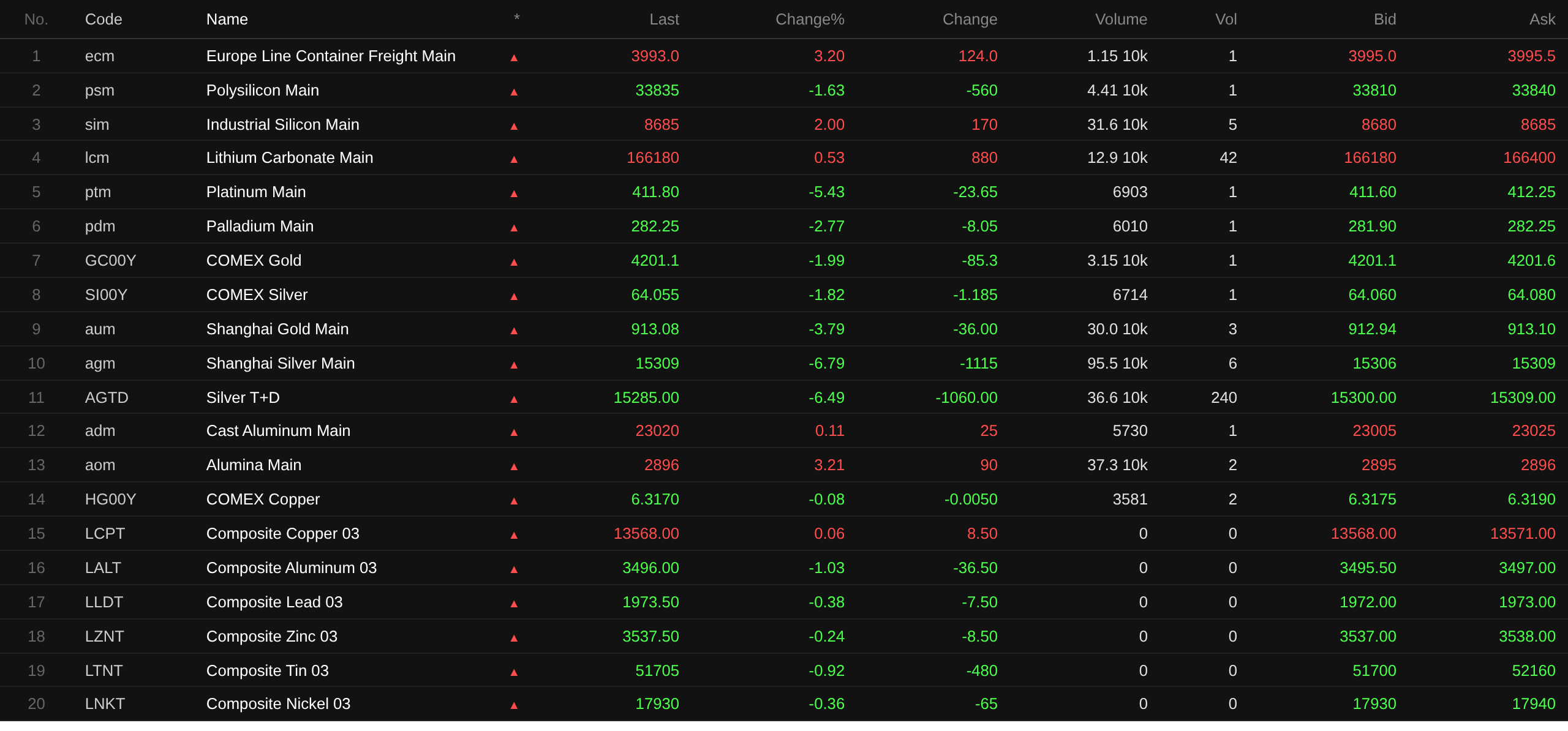

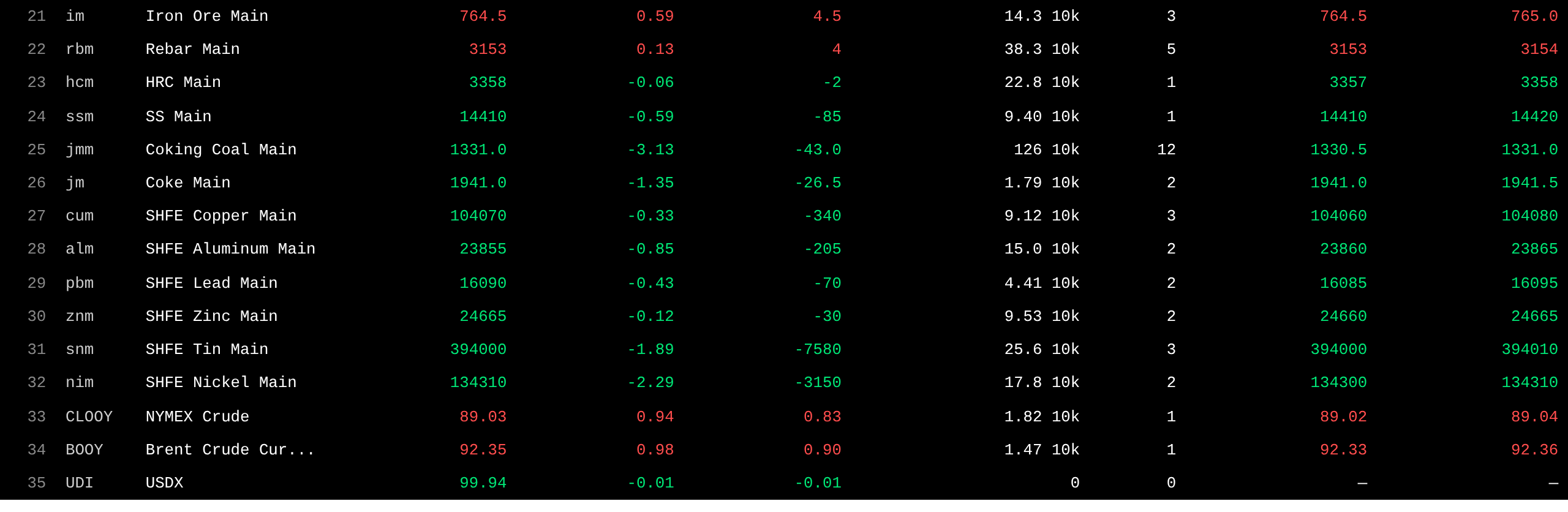

As of the midday close, base metals in the domestic market weakened across the board. SHFE lead fell 0.43%, SHFE tin dropped 1.89%, SHFE nickel lost 2.29%, SHFE copper edged down 0.33%, SHFE aluminum declined 0.85%, and SHFE zinc slipped 0.12%.

In addition, the most-traded foundry aluminum futures contract rose 0.11%, the most-traded alumina contract gained 3.21%, the most-traded lithium carbonate contract added 0.53%, the most-traded silicon metal contract increased 2%, while the most-traded polysilicon futures contract fell 1.63%.

Ferrous metals mostly fell. Iron ore rose 0.59%, rebar added 0.13%, HRC edged lower, and stainless steel fell 0.59%. In the coking coal and coke segment, the most-traded coking coal contract dropped 3.13%, and the most-traded coke contract declined 1.35%.

In overseas base metals, as of 11:39, LME metals were nearly all lower. LME copper edged up 0.06%, LME aluminum fell 1.03%, LME lead dropped 0.38%, LME zinc declined 0.24%, LME tin lost 0.92%, and LME nickel slipped 0.36%.

In precious metals, as of 11:39, COMEX gold fell 1.99%, touching an intraday low of $4,195.5/oz, while COMEX silver dropped 1.82%. In domestic precious metals, the most-traded SHFE gold contract declined 3.79%, and the most-traded SHFE silver contract slumped 6.79%. Ilya Spivak, global macro head at Tastylive, noted that the real drivers lie in shifting expectations around US Fed policy, rising yields, and a stronger US dollar. "I think these factors are all weighing on gold," he said. Spivak added that if gold breaks below the $4,100 mark, support levels would fundamentally change, and by the end of the year, we may be looking at the next threshold of $3,500. (Jin10 Data APP)

Meanwhile, by the midday close, the most-traded platinum futures contract fell 5.43%, and the most-traded palladium futures contract dropped 2.77%.

As of the midday close, the most-traded Europe container freight futures contract climbed 3.2% to 3,993 points.

As of 11:39 on June 10, some futures midday quotes:

Spot and Fundamentals

Zinc: Today, #0 zinc mainstream transaction prices were concentrated in the 24,575-24,745 yuan/mt range, Shuangyan was mainly transacted at 24,675-24,835 yuan/mt, and #1 zinc mainstream deals were at 24,505-24,675 yuan/mt. In early trading, the market quoted premiums of 20-30 yuan/mt against the SMM average price, with no quotes against the futures contract yet...

Macro Front

China side:

[National Bureau of Statistics (NBS): May CPI Rose 1.2% YoY, PPI Rose 3.9% YoY, with PPI Continuing to Increase] NBS data showed that in May 2026, the national consumer price index (CPI) rose 1.2% YoY. Among them, urban areas rose 1.3% and rural areas rose 1.1%; food prices fell 1.7%, while non-food prices rose 1.9%; consumer goods prices rose 1.6% and services prices rose 0.8%. On average for January–May, national consumer prices rose 1.0% YoY. In May, national consumer prices fell 0.1% MoM. In May 2026, national industrial producer ex-factory prices rose 3.9% YoY and 0.5% MoM. Industrial producer purchase prices rose 5.8% YoY and 1.3% MoM. On average for January–May, industrial producer ex-factory prices rose 1.0% YoY, and industrial producer purchase prices rose 1.6%. In May, within industrial producer purchase prices, nonferrous metal materials and wire products prices rose 22.0%, chemical raw material prices rose 11.8%, fuel and power prices rose 10.0%, textile raw material prices rose 2.5%, and ferrous metals material prices rose 0.3%; building materials and non-metallic products prices fell 5.5%, and agricultural and sideline product prices fell 1.6%. Dong Lijuan, chief statistician of the Urban Department of the National Bureau of Statistics (NBS), interprets the CPI and PPI data for May 2026.

The PBOC conducted a 159 billion yuan 7-day reverse repo operation at an interest rate of 1.4%, unchanged from the previous operation. There was no reverse repo maturing today.

Regarding the US dollar:

As of 11:39, the US dollar index fell 0.01% to 99.94. Affected by renewed US-Iran conflict, both the dollar and oil prices moved higher, intensifying market concerns over inflation and interest rate hikes, with markets awaiting key US inflation reports to assess the US Fed's monetary policy stance. (Jin10 Data APP)

At 20:30 Beijing time tonight, the US Bureau of Labor Statistics will release May CPI data. This is also the most closely watched heavyweight inflation data for the market ahead of new US Fed Chair Warsh's policy rate meeting next week. Based on forecasts, the four institutions Goldman Sachs, UBS, Deutsche Bank, and Morgan Stanley project May overall CPI YoY in a range of 4.17%–4.3%, all higher than April's 3.81% . However, core CPI MoM forecasts are generally below market consensus. (Wall Street Insights)

According to CME "FedWatch": The probability that the US Fed will keep interest rates unchanged through June is 98.2%, while the probability of a cumulative 25bp interest rate cut is 1.8%. The probability that the US Fed will keep interest rates unchanged through July is 85.8%, the probability of cumulative 25-basis-point rate hikes is 12.6%, and the probability of cumulative 25-basis-point rate cuts is 1.6%.

CSC Financial pointed out that in the near term, the likelihood of a Fed rate hike remains low, and market concerns about Fed tightening are mainly at the expectations level, built on assumptions of persistent domestic inflation and a continuously hot labor market in the US. Data from CME FedWatch shows that the timing of the most likely Fed rate hike expected by markets outside China begins at end-October 2026. The current global liquidity tightening and market adjustments represent an early reaction to expectations for a Fed rate hike in Q4. For China’s bond market, the increase in expectations of Fed tightening is not bearish. China’s bond market is relatively independent and has a low correlation with US Treasuries. Moreover, amid ample domestic liquidity, the expected tightening of liquidity outside China and adjustments in equity markets could drive capital flows into the bond market, supporting current levels of long-term bonds. The 10-year government bond yield is expected to continue fluctuating around 1.70% going forward; a break below 1.70% will still require the emergence of new incremental information from China.

On the data front:

Today, scheduled releases include US May unadjusted CPI YoY, US May seasonally adjusted CPI MoM, US May seasonally adjusted core CPI MoM, US May unadjusted core CPI YoY, the Bank of Canada interest rate decision for June 10, and China May M2 money supply YoY (pending), among others. In addition, focus will be on: the Bank of Canada’s interest rate announcement; and the monetary policy press conference with Bank of Canada Governor Tiff Macklem and Senior Deputy Governor Carolyn Rogers.

In crude oil:

As of 11:39, oil prices on both exchanges rose, with WTI crude up 0.94% and Brent crude up 0.98%. Renewed Middle East conflicts have raised supply concerns, while a decline in US crude oil inventories also supported prices.

Data: US API crude oil inventories for the week ending June 5 were -9.119 million barrels, compared to an expected -3.421 million barrels and a previous -6.757 million barrels. US API gasoline inventories for the week ending June 5 were -1.191 million barrels, compared to an expected -614,000 barrels and a previous 3.454 million barrels. (Jin10 Data APP)

Furthermore, the US Energy Information Administration (EIA) said on Tuesday local time that due to the loss of over 11 million barrels per day of crude oil production in the Middle East caused by the conflict, major consuming countries are drawing down inventories at an unprecedented pace to fill the supply gap, and commercial oil inventories in the OECD are on track to reach their lowest level since at least 2003. The EIA stated that, based on its current assumption that maritime traffic through the Strait of Hormuz is unlikely to return to pre-conflict levels before early 2027, total OECD oil inventories will fall to slightly below 2.3 billion barrels by December. (Jin10 Data APP)

Spot Market Overview:

►

►

►

►

►

►

►

![Suppliers Hold Prices Firm and Hold Back Selling as Delivery Approaches, Shanghai Spot Copper Premiums Remain Strong [SMM Shanghai Spot Copper]](https://imgqn.smm.cn/usercenter/gCNEi20251217171715.jpeg)

![Middle East tensions resurfaced, the center of the SHFE tin contract continued to decline to around 390,000 [SMM Tin Midday Review]](https://imgqn.smm.cn/usercenter/iLVGs20251217171753.jpg)