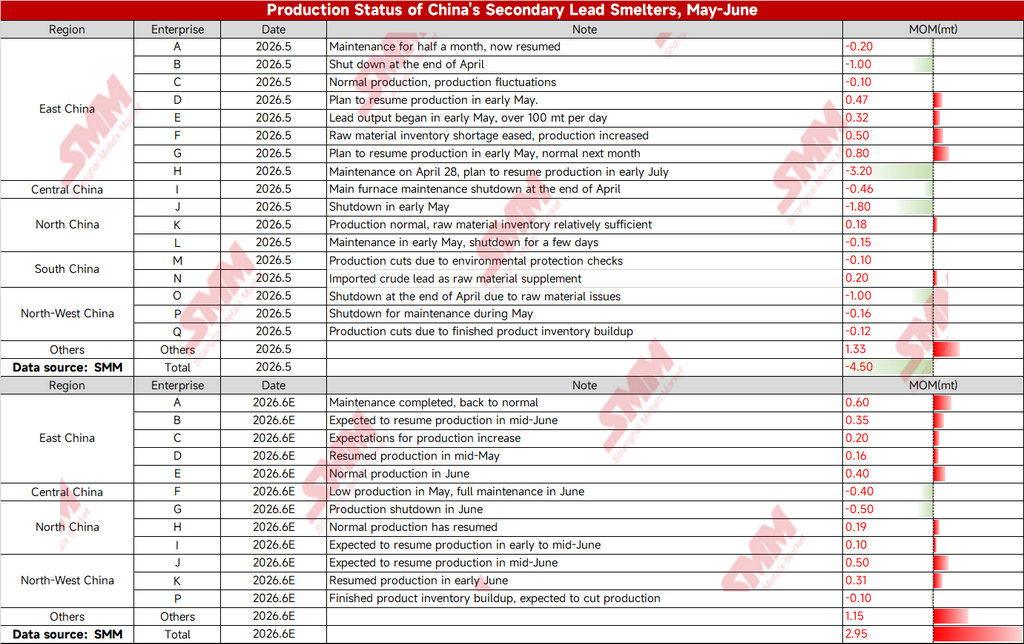

Data from SMM shows that in May, the MoM impact on refined lead from secondary lead enterprises in China totaled -45,000 mt, with the supply contraction widening further. Smelters in east China, central China, and north China, affected by production halts, maintenance, raw material shortages, and environmental protection checks, saw production cuts continue to spread.

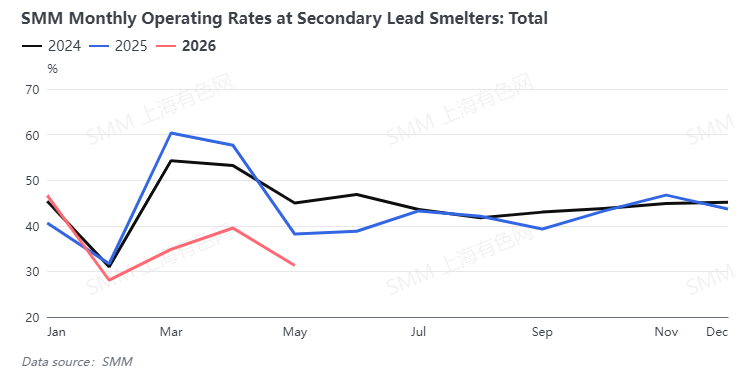

The enterprise operating rate declined significantly YoY, falling to a low level seen in recent years.

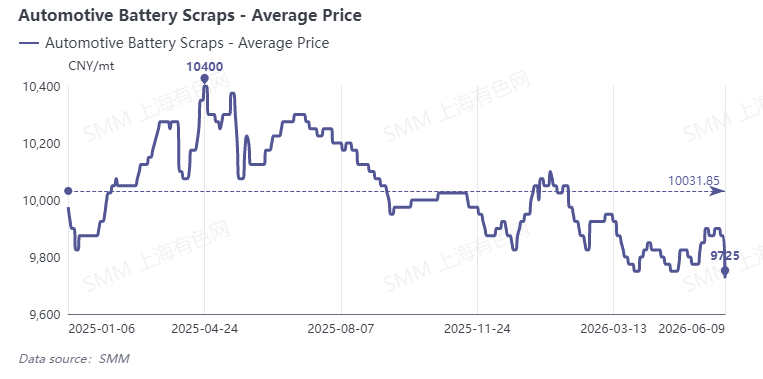

Raw material side, although the average price of scrap EV batteries retreated from highs, it remained at a relatively high level of 9,725 yuan/mt.

Elevated procurement costs continued to squeeze smelter margins, and coupled with finished product inventory buildup at some enterprises, the willingness for passive production cuts strengthened further.

While June production schedules indicate supply is expected to recover MoM, with the total MoM impact on refined lead at +29,500 mt and clear expectations for production resumptions and increases among smelters in east China and northwest China, the pace of recovery remains highly dependent on raw material arrivals. The tight supply pattern in the scrap battery recycling sector persists, limiting supply elasticity.

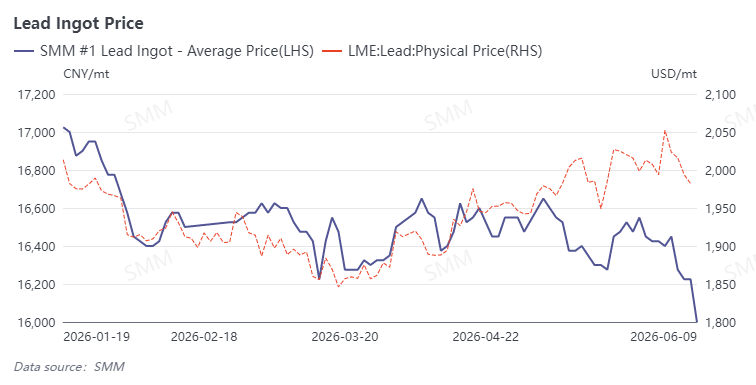

Consumption side, the downstream lead-acid battery market is in the traditional off-season, with sluggish end-use demand. China's spot lead prices continued to fluctuate downward, with the average SMM #1 lead ingot price having fallen below 16,200 yuan/mt. LME lead prices were also in the doldrums, with both domestic and overseas markets lacking clear upward momentum.

Overall, the secondary lead market will remain in a pattern of "weak cost support and strong consumption suppression" in the short term. Smelter production resumptions in June will find it difficult to fully offset previous cuts, with the supply side showing marginal improvement but remaining tight. Lead prices will continue to fluctuate weakly. Going forward, close attention should be paid to improvements in raw material arrivals and the recovery of end-use consumption, as both will jointly determine the pace of secondary lead supply recovery and the trajectory of lead prices.

![Supply Increase and Off-Season Demand Weigh on Lead Prices, Cost Support Limits Downside Room [Lead Futures Brief Review]](https://imgqn.smm.cn/usercenter/XMxKT20251217171720.jpeg)

![[SMM Analysis] Lead Prices Plunge to 27-Month Low – Is the 16,000 "Lifeline" About to Break?](https://imgqn.smm.cn/usercenter/guTSZ20251217171722.jpg)