In May, China’s copper billet sector remained in the doldrums. The industry entered the traditional consumption off-season, end-use demand continued to weaken, and multiple bearish factors—tight and expensive raw material supply, severe losses, and downstream clients switching to alternative materials—pushed profit pressure to its worst level in nearly two to three years. Enterprises became less willing to produce and take orders, and overall operating difficulties became pronounced.

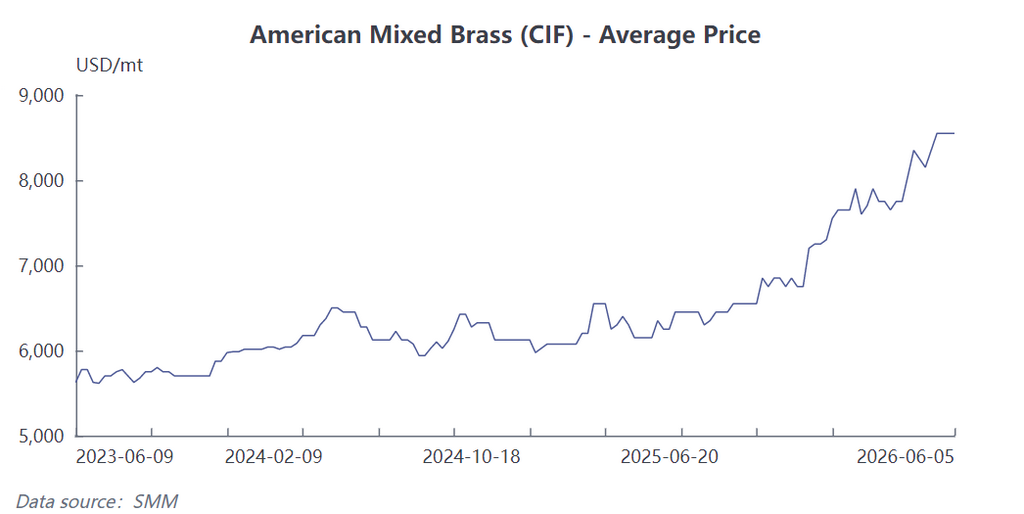

The raw material supply side saw escalating chaos that intensified cost pressure, highlighting a severe supply-demand mismatch. In May, the supply of recycled brass raw materials remained persistently tight with prices staying high, primarily influenced by speculation in the brass scrap market. Copper-zinc separation operations drove up brass scrap prices, compounded by constraints on reverse invoicing and a shortage of imported recycled brass cargoes that were highly sought-after. These factors narrowed enterprises’ raw material procurement channels and caused procurement costs to climb sharply. A comparison with the same period in previous years shows that, at equivalent LME copper price levels, the raw material price increase this year far outpaced the room to adjust finished product prices.

The demand side remained persistently weak, with market substitution effects becoming increasingly evident. Traditional copper billet demand in end-use markets continued to shrink. An increasing number of downstream clients, seeking to control costs and adapt to market requirements, gradually transitioned to using materials such as stainless steel and plastics to replace copper products, directly diverting a large volume of copper billet orders. Meanwhile, demand in traditional core end-use markets like refrigeration and sanitary ware hardware showed no signs of recovery. Downstream enterprises showed low enthusiasm for cargo pick-up, maintaining only just-in-time procurement, which led to a marked contraction in the industry’s overall order volume.

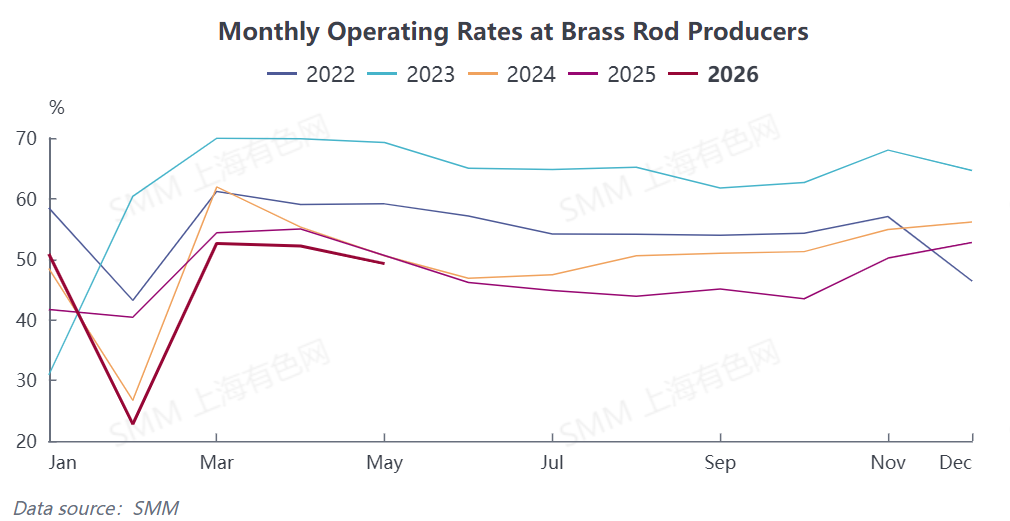

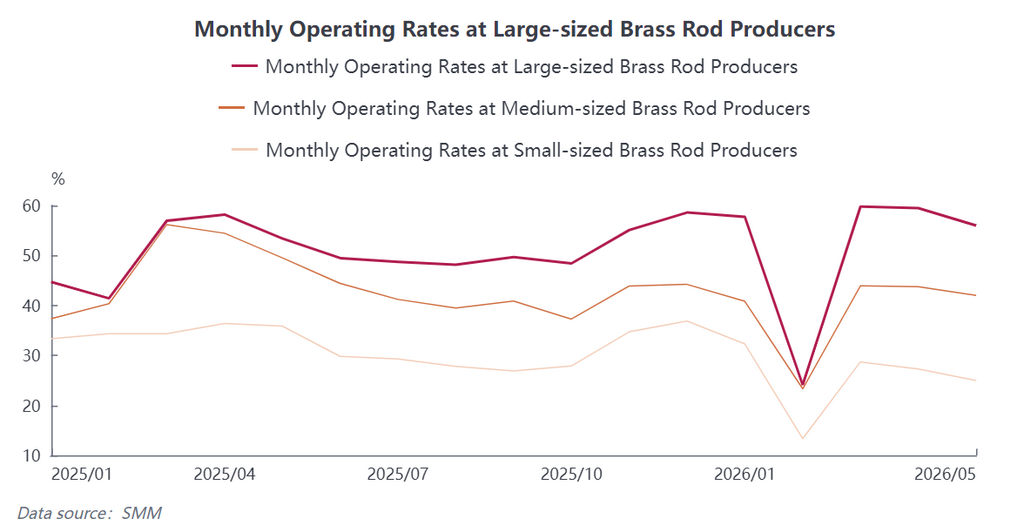

Operating rate data showed a continued pullback, with significant polarization among enterprises. Data indicates that the comprehensive operating rate for copper billet enterprises in May stood at 49.27%, down 2.91 percentage points MoM and down 0.65 percentage points YoY. By enterprise scale, large enterprises leveraged their advantages in raw material channels and capital to maintain relatively stable production, with an operating rate of 56.01%. Medium-sized enterprises were notably under pressure, with their operating rate falling to 42.02%. Small enterprises were hit by the triple shock of raw material shortages, losses, and insufficient orders, bringing production to a near standstill with an operating rate of only 24.96%. The gap in operating rates between large, medium-sized, and small enterprises continued to widen, intensifying industry polarization.

Looking ahead to June, the off-season effect in the industry continues to intensify, and the market lacks momentum for a recovery. Traditional end-user demand remains sluggish, while the substitution trend of stainless steel further deepens, leading to continued shrinkage in rigid demand for copper billets; on the raw material side, tightness in imported supply and the persistently high-price pattern of China's secondary brass are difficult to reverse in the short term, keeping cost pressure on enterprises at highs. Coupled with cautious willingness to take orders and produce amid losses, the industry's production load will continue to decline. SMM expects that in June, the operating rate of the copper billet industry will drop 3.88 percentage points MoM to 45.39%, and fall 1.72 percentage points YoY, with the overall in-the-doldrums operating trend of the industry set to persist.