Le 26 mai 2026, l'événement « Salon SMM des métaux ferreux 2026 — Session de Hangzhou », co-organisé par Zheshang Futures Co., Ltd. et SMM Information & Technology Co., Ltd., s'est tenu avec succès. Près de quarante clients de la chaîne industrielle des métaux ferreux ont participé à la conférence, partageant et échangeant leurs points de vue sur des sujets tels que la situation actuelle de l'industrie des métaux ferreux, les opportunités d'exportation d'acier, les sujets brûlants du marché et la gestion des risques des entreprises sidérurgiques, stimulant ainsi de futures idées de coopération et de négoce dans l'industrie de l'acier.

Chen Kaihang, analyste en chef de la série des métaux ferreux au Centre de recherche de Zheshang Futures, estime :

1. La demande en barres d'armature est en déclin, l'offre s'ajustant à la demande. La production des fours électriques reste résiliente, tandis que les hauts fourneaux ne parviennent pas à dégager de bénéfices ;

2. Les bobines laminées à chaud (HRC) sont portées par les prix internationaux de l'acier, mais le prix FOB de la Chine doit rester dans une zone de prix bas pour conserver un avantage à l'exportation ;

3. L'offre de minerai de fer augmente, la demande a peu de chances de croître, les stocks sont à des niveaux élevés, les coûts baissent et la tendance baissière est marquée ;

4. La spéculation sur le charbon à coke ne peut pas entraîner l'acier, les problèmes de livraison persistent et les risques seront plus importants après la fin de la spéculation ;

Résumé : Le prix FOB des HRC détermine le plafond de prix des contrats à terme HRC, et l'écart HRC-barres d'armature restera élevé, voire continuera de s'élargir légèrement. Les prix des matières premières sidérurgiques subissent une pression à la baisse. Globalement, la stratégie sur l'acier reste la vente à découvert sur les rebonds. Les achats à bas prix ne seront envisageables que lorsque la production de barres d'armature des hauts fourneaux reculera à nouveau.

Ding Xiaoli, analyste senior des métaux ferreux chez SMM, a déclaré :

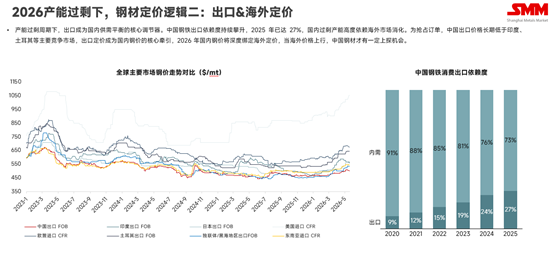

Dans un cycle de surcapacité, les exportations sont devenues le régulateur central de l'équilibre offre-demande en Chine. La dépendance de la Chine aux exportations d'acier n'a cessé de croître, atteignant 27 % en 2025, la capacité excédentaire nationale étant fortement tributaire des marchés hors de Chine pour son absorption. Pour décrocher des commandes, les prix à l'exportation de la Chine sont restés durablement inférieurs à ceux des principaux marchés concurrents tels que l'Inde et la Turquie, faisant de la tarification à l'exportation le moteur principal des prix de l'acier domestique. En 2026, les prix de l'acier domestique seront étroitement liés aux prix hors Chine, et ce n'est que lorsque les prix à l'étranger augmenteront que l'acier chinois disposera d'un potentiel de hausse.

![[Analyse SMM] Les aciéries EAF prévoient de réduire leurs heures d’exploitation](https://imgqn.smm.cn/usercenter/QMaot20251217171719.jpg)