SMM, May 26:

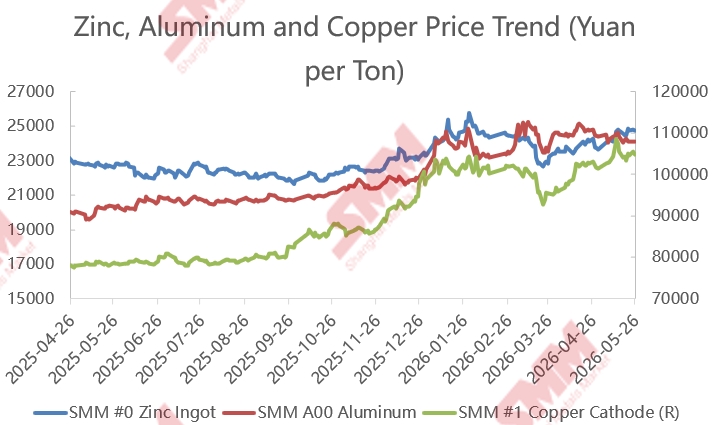

According to SMM data, prices of zinc, aluminum, and copper rose overall starting from the end of last year, and die-casting zinc alloy enterprises continued to face cost pressure. Meanwhile, since March this year, aluminum prices surpassed zinc prices, with the price center steadily running above 23,400 yuan/mt with fluctuations, while copper prices operated above 100,000 yuan/mt for most of the time since entering 2026, intensifying the operational pressure on die-casting zinc alloy producers.

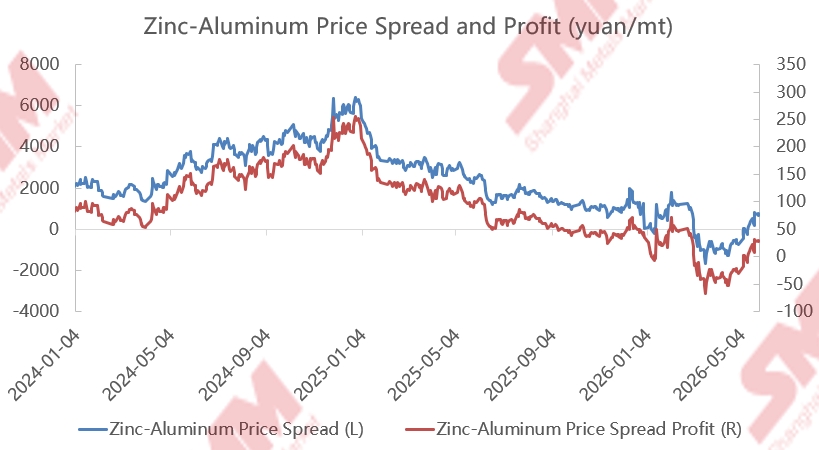

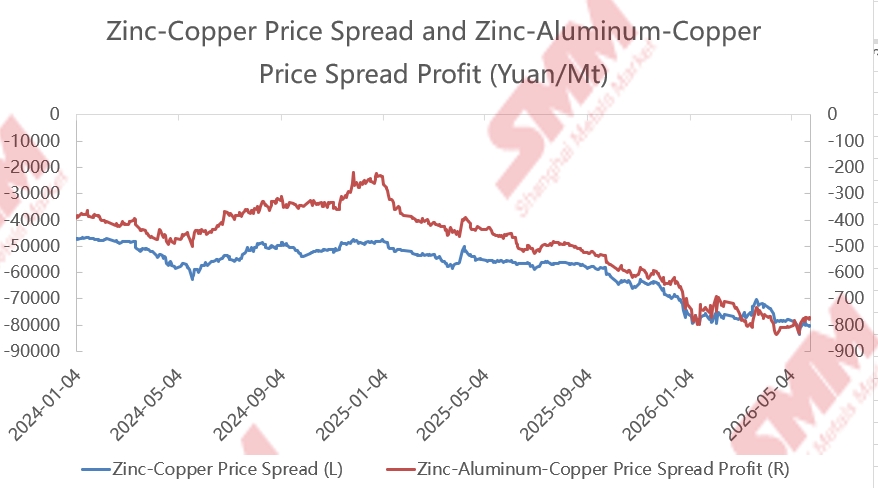

Entering May, the zinc-aluminum price spread improved. As of May 26, the average zinc-aluminum price spread in May rebounded to 209 yuan/mt, up 124% MoM from April's -868 yuan/mt. From the perspective of zinc-aluminum price profitability, the zinc-aluminum price spread profit edged up from -35 yuan/mt in April to around 11 yuan/mt. The profit margin for die-casting zinc alloy producers' #3 products improved somewhat. Meanwhile, for #5 products, although the monthly average zinc-copper price spread widened from -76,519 yuan/mt in April to -80,275 yuan/mt in May, continuing to widen by 5% MoM, the zinc-aluminum-copper price profitability improved amid synchronized fluctuations in zinc and aluminum prices, recovering slightly from -800 yuan/mt in April to -792 yuan/mt, with profits also improving marginally. Based on recent data, although alloy producers' profit margins saw slight recovery recently, downstream alloy consumption remained weak, with order demand across various sectors being lackluster.

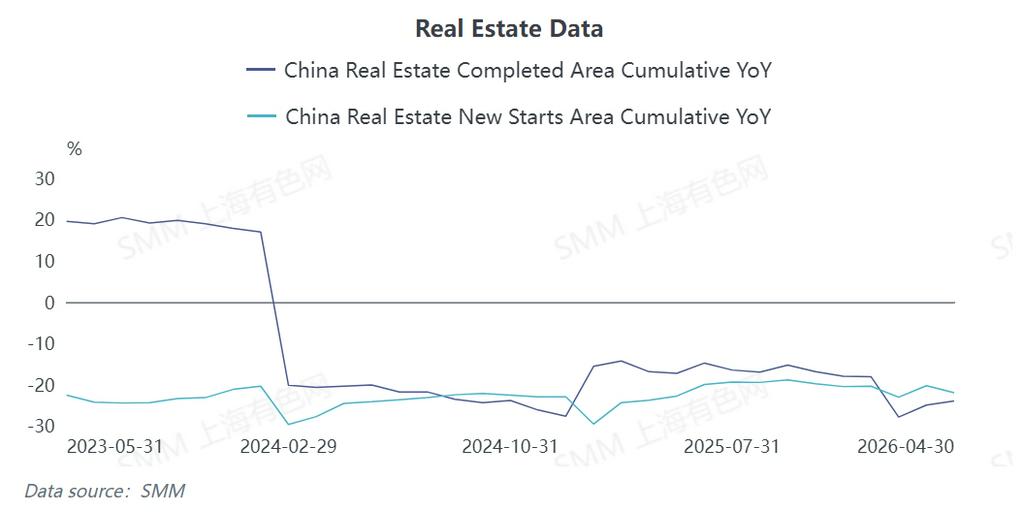

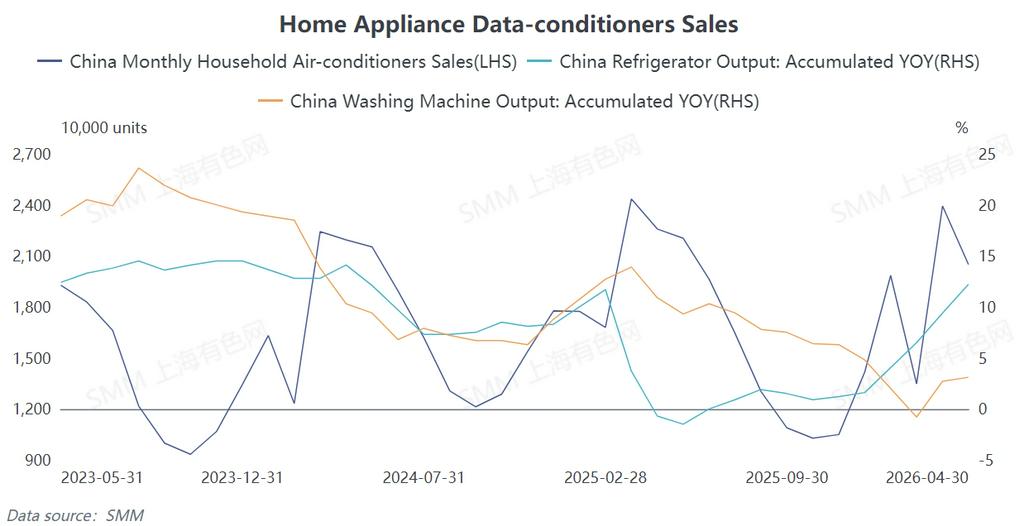

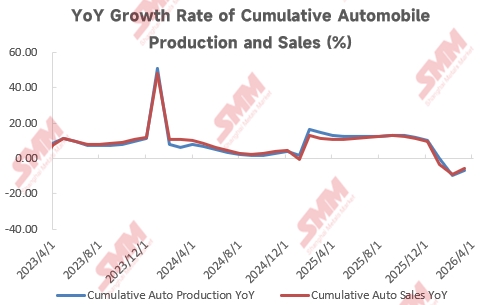

China's die-casting zinc alloy consumption has entered the off-season, with divergent performance across sectors. First, from January to April, real estate completion area and new housing starts declined significantly YoY, with cumulative real estate completion area down 24% and cumulative new housing starts down 22%, pointing to expectations of shrinking demand for architectural hardware. Moreover, from January to April, China's cumulative automobile production and sales fell 5.5% and 4.8% YoY, respectively. Even though auto exports performed strongly, domestic automobile production and sales remained mediocre. In the home appliance sector, only refrigerator and washing machine consumption maintained positive growth, while air conditioner consumption weakened.

At the same time, zinc alloy supplies from smelters are currently circulating in relatively sufficient volumes in the market. Coupled with the arrival of the traditional consumption off-season, end-user procurement has become more cautious. The overall market supply-demand balance leans toward looseness, and there is insufficient momentum for a short-term consumption recovery. Affected by this, die-casting zinc alloy enterprises still face considerable sales pressure.

Overall, although cost pressure on die-casting zinc alloy enterprises has been slightly alleviated at this stage, the issues of overcapacity and weakening end-use demand persist. National-standard die-casting zinc alloy producers as a whole remain in a state of operating under tight margins.

If you have any questions, please feel free to contact me at:jiangmengting@smm.cn