China’s hydrogen market is showing clear divergence: alkaline electrolyzers are booming with frequent deliveries, PEM electrolyzers stay quiet, and AEM technology is quietly advancing. This “ice and fire” trend reveals competition over technical maturity and market selection. Meanwhile, breakthroughs in storage, transportation and refueling are reshaping the industry, marking a more rational and practical stage for China’s hydrogen sector.

I. Alkaline Electrolyzers: Booming on Cost and Scale

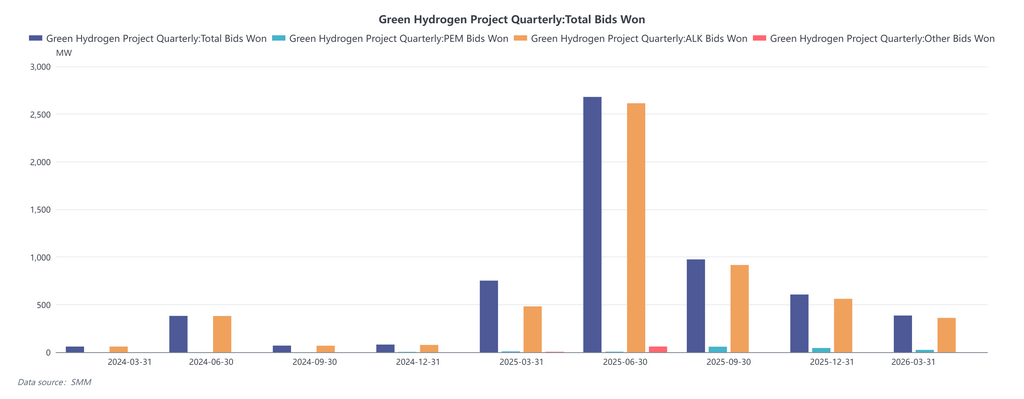

Alkaline electrolyzers dominate the market with surging deliveries and large-scale deployment. CRRC Zhuzhou Institute shipped 12 sets of 1200 Nm³/h alkaline electrolyzers for CHN Energy’s “Liquid Sunshine” project; CFHI delivered a 3,000 Nm³/h system; and PetroChina’s 2,000 Nm³/h unit successfully commissioned with hydrogen purity reaching 99.9995%.Sunshine Hydrogen won a 30,000 Nm³/h contract for a green methanol project, while EVE Hydrogen and Haozhen Hydrogen also completed deliveries. Driven by mature technology, low cost and a complete supply chain, alkaline electrolyzers have become the top choice for large-scale, cost-sensitive green hydrogen projects.

II. PEM Electrolyzers: Silent Strategic Reserve

PEM electrolyzers are largely absent from recent headlines mainly due to high costs from precious metal catalysts and proton exchange membranes. Its strength—fast response to wind and solar fluctuation—is not yet a must-have for most large projects, which prefer grid-supported alkaline systems.Yet PEM development has not stopped. Domestic firms are pushing for localization of core materials, waiting for cost declines and scenario maturity to unleash its advantages.

III. AEM Electrolyzers: Laying Ground for Next-Gen Tech

AEM combines the low cost of alkaline and high efficiency of PEM, seen as a promising next-generation route. It is still in pre-industrial phase, with focus on improving membrane durability and membrane electrode manufacturing. Enterprises are making steady breakthroughs in materials and processes for long-term competition.

IV. Storage & Transportation: Key Breakthroughs for Scaling

Large-scale gaseous hydrogen storage is moving forward: SPIC’s Da’an project plans six 1,850 m³ spherical tanks, greatly improving storage capacity.Liquid hydrogen sees a milestone: China’s first 5-ton/day hydrogen liquefaction plant started operation with 100% domestic equipment and 40% lower energy consumption, cutting costs for long-distance transport.Guofu Hydrogen built a hydrogen-natural gas blending platform supporting 0%–30% blending. SAMR launched safety standards for hydrogen refueling stations, filling gaps in liquid hydrogen refueling rules.Improved storage, transportation and standards expand the economic radius of green hydrogen and lay a foundation for large-scale application.

Conclusion

The divergence of hydrogen production routes reflects market choice based on technical maturity: alkaline leads for near-term economy, PEM reserves strength for flexible scenarios, and AEM targets next-generation innovation. The three routes are complementary rather than substitutive.Breakthroughs in storage and transportation are game-changers. With falling liquid hydrogen costs, better infrastructure and completed standards, the industry will enter a more diversified and dynamic era.