SMM News, May 21:

Metals market:

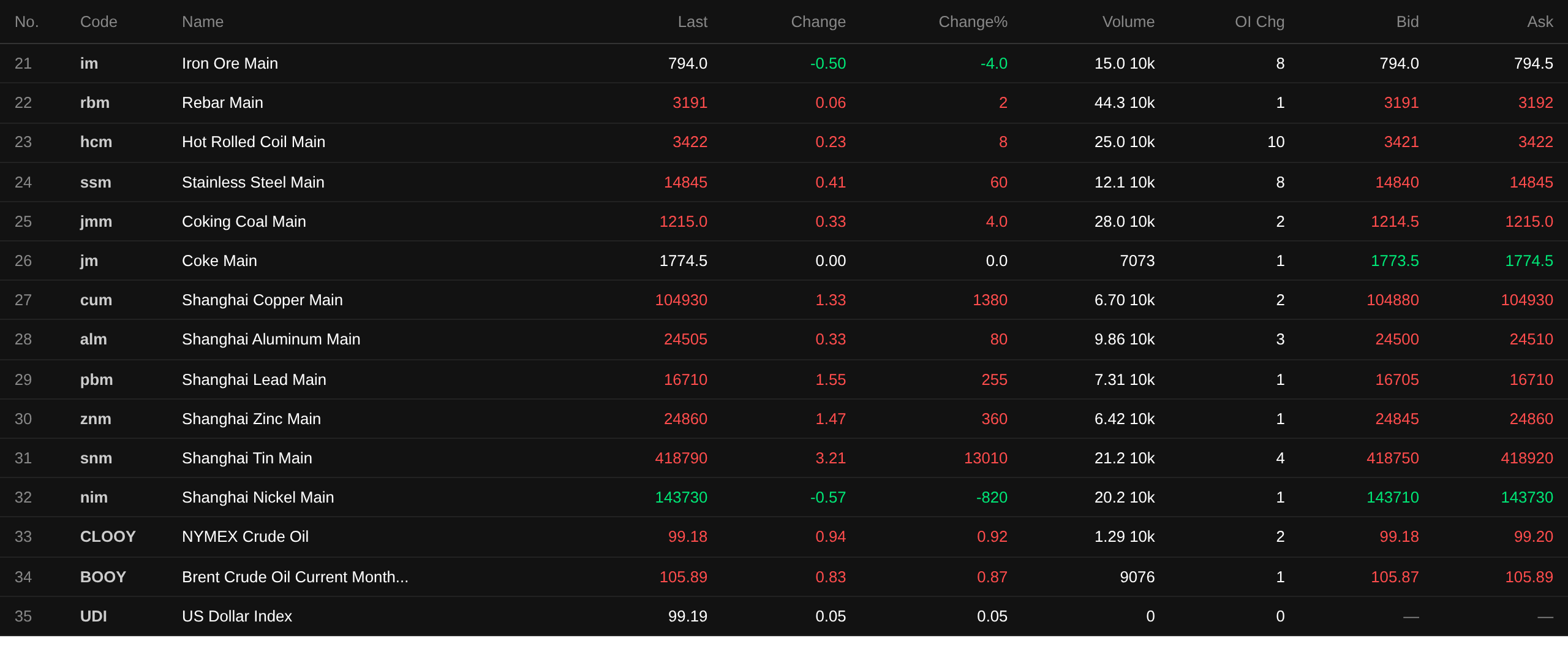

As of the midday close, most base metals on the domestic market rose. SHFE copper gained 1.33%, SHFE aluminum rose 0.33%, SHFE lead climbed 1.55%, SHFE zinc advanced 1.47%, and SHFE tin surged 3.21%. SHFE nickel fell 0.57%.

In addition, the most-traded casting aluminum futures rose 0.39%, the most-traded alumina contract gained 0.37%, the most-traded lithium carbonate contract rose 1.18%, the most-traded silicon metal contract climbed 0.35%, and the most-traded polysilicon futures rose 0.37%.

Ferrous metals mostly rose. Iron ore fell 0.5%, rebar edged up, hot-rolled coil gained 0.23%, and stainless steel rose 0.41%. Coking coal and coke: the most-traded coking coal contract rose 0.33%, and the most-traded coke contract was flat at 1,774.5 yuan/mt.

Overseas base metals: as of 11:32, LME metals generally fell. LME copper dropped 0.15%, LME aluminum was flat at 3,629 yuan/mt, LME lead rose 0.71%, LME zinc fell 0.1%, LME tin declined 0.53%, and LME nickel dropped 0.92%.

Precious metals: as of 11:32, COMEX gold rose 0.12% and COMEX silver fell 0.26%. Domestic precious metals: the most-traded SHFE gold contract gained 0.89% and the most-traded SHFE silver contract rose 1.85%.

In addition, as of the midday close, the most-traded platinum futures rose 0.74% and the most-traded palladium futures gained 0.47%.

As of the midday close, the most-traded Europe containerized freight index contract rose 7.66% to 2,957.5 points.

As of 11:32 on May 21, midday futures quotes for selected contracts:

Spot cargo and fundamentals

Nickel:On May 21, SMM #1 refined nickel prices rose 1,550 yuan/mt from the previous trading day. Spot premiums: Jinchuan #1 refined nickel averaged 1,200 yuan/mt, down 250 yuan/mt from the previous trading day. Domestic mainstream brand electrodeposited nickel premiums ranged from -600 to 500 yuan/mt.

Macro front

China:

[NDRC: To improve policy measures on fair competition, investment and financing, promotion of sci-tech innovation, and business regulation]Li Hui, Director of the Private Economy Development Bureau of the National Development and Reform Commission (NDRC), stated at a press conference held by the State Council Information Office that the NDRC will better leverage its coordination function in promoting private economy development, organize and carry out specific measures outlined in the action plan for safeguarding the private economy through the rule of law, and strengthen the implementation of the Private Economy Promotion Law. The NDRC will improve supporting systems and refine policy measures on fair competition, investment and financing, promotion of sci-tech innovation, and business regulation. It will continue to work with relevant departments to publish typical cases to illustrate the law through cases, conduct assessments of policy implementation effectiveness, promote direct and swift access to enterprise-friendly policies, and guide enterprises in enhancing their governance capabilities.

[China's Enterprise Credit Index Reached 162.41 in April This Year, Maintaining a Positive Trend] According to the State Administration for Market Regulation, China's Enterprise Credit Index stood at 162.41 in April this year, up 0.15 points from March, with enterprise credit levels maintaining a positive trend. In April, the top 5 industries by credit index ranking were finance, electricity/heat/gas and water production and supply, education, manufacturing, and water conservancy/environment and public facilities management. Compared with the previous month, the indices for information transmission/software and information technology services, finance, and health and social work showed relatively notable increases, achieving positive growth for three consecutive months, with credit development trends continuing to improve. (CCTV News)

[Qiushi Commentary Article: How to Thoroughly Address "Involution-Style" Competition in Manufacturing] The article pointed out that thoroughly addressing "involution-style" competition requires institutional innovation to drive competition toward quality upgrading. Only when government behavior is regulated and market mechanisms are streamlined can enterprises shift from low-price disorderly competition to value-based competition. A unified national market should be built to break down market segmentation, policies hindering fair competition should be resolutely eliminated, outdated capacity should be phased out in an orderly manner in accordance with laws and regulations to prevent "bad money driving out good," and competitive enterprises should be allocated resources commensurate with their competitiveness. Performance assessment reform should be used to correct government behavior, shifting assessment focus toward "quality" indicators such as development quality, technological innovation, and industrial coordination, aligning local government incentives with high-quality development, and curbing the impulse for homogeneous investment attraction at the source. Evaluation mechanism reform should be used to rectify competitive behavior, reversing the "price-only" tendency, establishing comprehensive evaluation mechanisms centered on technology, quality, and service, making premium quality at premium prices a market consensus, and guiding resources toward enterprises with strong innovation capabilities and high product value-added.

The PBOC conducted 100 billion yuan of 7-day reverse repo operations in the open market at an interest rate of 1.40%, unchanged from the previous day. Today, 500 million yuan of reverse repos matured.

US Dollar:

As of 11:32, the US dollar index rose 0.05% to 99.19. The US Fed meeting minutes showed that participants anticipated elevated energy prices would continue to exert upward pressure on headline inflation in the near term. Participants generally expected that the impact of tariffs on core goods inflation would gradually diminish over the course of this year. However, some participants noted that tariff rates could rise further above current levels, resulting in greater upward pressure on inflation. Several participants emphasized that, after inflation had remained above 2% for several consecutive years, elevated inflation could have a greater influence on wage- and price-setting decisions. Almost all participants noted that the conflict in the Middle East could persist for an extended period, or even if the conflict ended, oil and other commodity prices could remain elevated for longer than expectations. In such a scenario, participants anticipated that factors such as supply chain disruptions, elevated energy prices, or the pass-through of higher input costs to other prices would continue to push inflation higher. The vast majority of participants noted that the time required for inflation to return to the Committee's 2% target could be longer than they had previously expected, and that risks had increased.

The US Fed meeting minutes showed that regarding the monetary policy outlook, participants generally believed that persistently elevated inflation and uncertainty about the duration and economic impact of the Middle East conflict could necessitate maintaining the current policy stance for longer than expectations. Some participants emphasized that it might be appropriate to lower the target range for the federal funds rate once clear signs emerged that the pullback trend in inflation had steadily resumed, or signs of greater softness in the labour market appeared. However, most participants noted that if inflation remained persistently above 2%, some tightening measures might be necessary. To address this scenario, many participants indicated that they would prefer to remove language from the post-meeting statement that implied the Committee's future rate decisions might lean toward easing. Participants noted that monetary policy was not predetermined and that future policy decisions would be made on a meeting-by-meeting basis. According to the CME "FedWatch" tool: the probability of the US Fed maintaining rates unchanged through June was 97.3%, with a cumulative probability of a 25-basis-point interest rate cut at 2.7%. The probability of the US Fed maintaining rates unchanged through July was 87.2%, with a cumulative probability of a 25-basis-point interest rate cut at 2.4%, and a cumulative probability of a 25-basis-point rate hike at 10.4%. (Jin Shi Data)

On the data front:

Data to be released today include US initial jobless claims for the week ending May 16, US April annualized housing starts, US April building permits, US May Philadelphia Fed Manufacturing Index, US May S&P Global Manufacturing PMI preliminary reading, US May S&P Global Services PMI preliminary reading, Eurozone May Manufacturing PMI preliminary reading, Eurozone March seasonally adjusted current account, Eurozone May Consumer Confidence Index preliminary reading, France May Manufacturing PMI preliminary reading, Germany May Manufacturing PMI preliminary reading, UK May Manufacturing PMI preliminary reading, UK May Services PMI preliminary reading, UK May CBI Industrial Orders balance, and Australia April seasonally adjusted unemployment rate. In addition, attention should also be paid to the following: Bank of England Governor Bailey delivered a speech, and China's refined oil products were set to enter a new round of price adjustment window.

Crude oil:

As of 11:32, oil prices in both markets rose, with WTI up 0.94% and Brent up 0.83%. Supply concerns driven by market worries over the uncertain prospects of a US-Iran peace deal continued to support oil prices. In addition, declining US crude oil inventory also lent support to oil prices.

EIA report: Commercial crude oil inventory, excluding the Strategic Petroleum Reserve, fell by 7.863 million barrels to 445 million barrels, a decline of 1.74%. The weekly EIA crude oil inventory drawdown for the week ending May 15 was the largest since the week of February 13, 2026.

A research report from CITIC Securities noted that global oil inventory was declining sharply, intensifying the risk of energy shortages. The US-Israel-Iran conflict disrupted passage through the Strait of Hormuz, causing global oil inventory to plummet at a record pace and heightening the risk of summer energy shortages. The market temporarily cushioned the pressure by relying on previously surplus inventory, exemptions from Russian oil sanctions, and strategic petroleum reserve releases by multiple countries, while high oil prices also triggered a contraction in global oil demand. International oil prices are currently fluctuating at elevated levels, US refined product prices have hit multi-year highs, oil supplies in multiple energy-importing regions in Asia are on the verge of shortages, dragging down regional economic growth. Oil prices may still have significant upside room, and accelerating the development of renewable energy has become a long-term measure for countries to guard against energy risks.

Sultan Al Jaber, CEO of the Abu Dhabi National Oil Company (ADNOC) of the UAE, said on the 20th that the UAE was building an east-west oil pipeline bypassing the Strait of Hormuz. The project was nearly 50% complete and is expected to be completed and operational by 2027. According to the UAE's Gulf News, Al Jaber said at an online event hosted by the US think tank Atlantic Council that a large volume of global energy transportation still relied on a few critical maritime chokepoints, and the UAE hoped to reduce its dependence on the Strait of Hormuz and enhance the security of energy exports through this project. (Xinhua)

Goldman Sachs stated that as the Middle East war continued and supply remained constrained, global crude oil and refined product inventory was being depleted at a record pace this month. Goldman Sachs analysts noted in a report dated May 20 that since the beginning of May, visible inventory had been declining at a record rate of 8.7 million barrels per day, nearly double the average pace since the outbreak of the conflict. They stated, "The physical market continues to tighten, and oil exports through the Strait of Hormuz are estimated to remain at only 5% of normal levels." Goldman Sachs analysts noted that two-thirds of the inventory decline in May was driven by a reduction in so-called "oil on water," with exports falling more than imports. The sluggish imports are now "spreading from Asia to Europe," they noted, with European jet fuel imports 60% below the 2025 average. (Jin10 Data)

Spot Market Overview:

►

►

►

►

►

►

►

►

►

![[SMM Flash News] Indonesia Appoints Danantara to Form New BUMN Export Agency for Strategic Natural Resources](https://imgqn.smm.cn/usercenter/yhuhG20251217171735.jpg)

![Tight Supply Overlaid with Liquidity Tightening Expectations, SHFE Tin Contract Consolidates at Highs in Stagnant Trading [SMM Tin Midday Review]](https://imgqn.smm.cn/usercenter/fMkfI20251217171752.jpg)

![Slightly Widening Price Spread Between Futures Contracts Bolstered Efforts to Hold Prices Firm, Spot Copper Discounts on SHFE Copper Moved Sideways [SMM Shanghai Spot Copper]](https://imgqn.smm.cn/usercenter/JopQJ20251217171712.jpg)