En avril 2026, le marché chinois d'import-export de cathodes de cuivre a affiché une tendance claire de « hausse des importations et baisse des exportations ». Avec la reprise partielle de la demande de consommation intérieure et l'ajustement de l'écart de prix entre les marchés national et international, les importations de cathodes de cuivre ont enregistré une croissance à deux chiffres en glissement mensuel, tandis que les exportations ont nettement reculé après une base élevée la période précédente. Notamment, les flux entrants de cathodes de cuivre EQ en provenance de pays tels que la RDC et la Russie sont restés élevés, portant la part des importations de cuivre EQ en avril à plus de 70 %, un record historique pour la même période ces dernières années.

Selon les données totales d'import-export publiées par l'Administration générale des douanes, les exportations chinoises de cathodes de cuivre en avril se sont élevées à 25 600 tonnes, en baisse de 56,01 % en glissement mensuel et de 67,05 % en glissement annuel. Bien que les exportations mensuelles aient connu un recul saisonnier notable, combinées à la performance globale du T1, les exportations cumulées de janvier à avril ont maintenu une croissance positive de 30,84 % en glissement annuel. Côté importations, les importations chinoises de cathodes de cuivre en avril ont rebondi à 270 500 tonnes, en hausse de 15,27 % en glissement mensuel et de 8,19 % en glissement annuel. Le rebond des importations en avril a efficacement atténué les tensions sur le marché spot dans certaines régions du marché intérieur. Toutefois, dans une perspective à plus long terme, les importations cumulées de janvier à avril restaient en baisse de 21,10 % en glissement annuel, reflétant les ajustements structurels des flux globaux de contrats à long terme et de cargaisons spot cette année par rapport aux années précédentes.

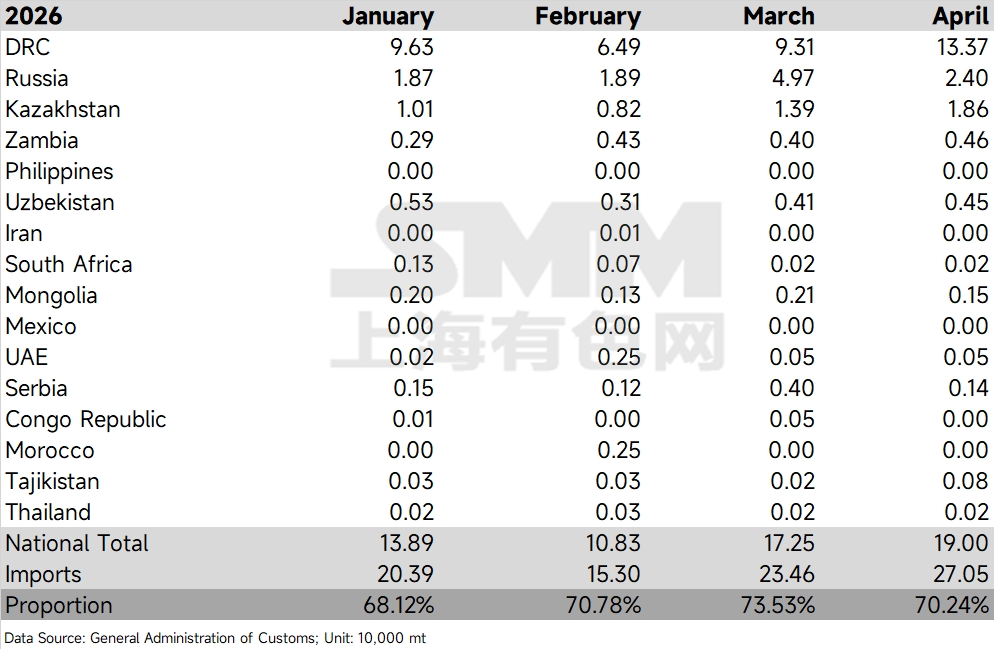

Une analyse approfondie de la structure des importations révèle que les principaux pays sources de cathodes de cuivre EQ dans les statistiques ont collectivement contribué à la grande majorité du volume incrémental, la RDC continuant de se distinguer comme le premier contributeur. En avril, les importations chinoises de cathodes de cuivre en provenance de la RDC ont atteint 133 700 tonnes, une augmentation significative de plus de 40 000 tonnes par rapport aux 93 100 tonnes de mars, représentant une hausse notable en glissement mensuel et consolidant sa position de premier fournisseur de cuivre EQ à la Chine. En comparaison, les importations de cathodes de cuivre en provenance de Russie en avril se sont établies à 24 000 tonnes, en recul par rapport aux 49 700 tonnes de mars ; l'approvisionnement en provenance du Kazakhstan a progressé régulièrement à 18 600 tonnes ; d'autres pays comme la Zambie ont enregistré 4 600 tonnes et l'Ouzbékistan 4 500 tonnes, maintenant un flux entrant globalement stable.

Guidées par cette dynamique de flux, les importations totales en provenance des principaux pays sources EQ ont atteint 190 000 tonnes en avril, affichant une tendance continuellement haussière par rapport aux 138 900 tonnes en janvier, 108 300 tonnes en février et 172 500 tonnes en mars. En termes de tendance des parts, les importations de cathodes de cuivre EQ ont représenté 70,24 % en avril. Bien que ce chiffre ait légèrement reculé de 3,29 points de pourcentage par rapport au sommet historique de 73,53 % en mars, une comparaison sur une période plus longue avec les données historiques de 2022 à 2026 montre que ce ratio dépasse largement la fourchette de fluctuation typique de 45 % à 65 % observée durant la même période entre 2022 et 2024, étant globalement au niveau des sommets de 2025 avec une légère percée. Cela indique que les sources EQ sont devenues de facto l'offre dominante absolue dans les importations actuelles de cathodes de cuivre en Chine.

À l'avenir, la part des importations de cathodes de cuivre EQ s'est maintenue à un niveau élevé supérieur à 70 % pendant trois mois consécutifs, indiquant que la pénétration des déplacements de flux géopolitiques et des nouvelles capacités de fusion hors Chine sur le marché chinois s'approfondit davantage. Le rebond mensuel des importations en avril a été principalement alimenté par une demande de reconstitution rigide des stocks durant la traditionnelle haute saison du deuxième trimestre en Chine et une amélioration ponctuelle de la fenêtre d'importation. Le cuivre EQ, bénéficiant d'un certain avantage de prix, a été absorbé sans difficulté dans le système actuel des cathodes de cuivre. À l'avenir, il convient de surveiller attentivement le rythme des arrivées de cargaisons EQ hors Chine dans les ports de mai à juin, ainsi que l'évolution des taux d'utilisation des entreprises en aval en Chine vers la fin de la haute saison. Si la consommation ne parvient pas à absorber continuellement l'afflux élevé de cuivre EQ, les stocks visibles en Chine pourraient être confrontés à une pression localisée d'accumulation des stocks.

Il convient de noter qu'en Afrique, en prenant l'exemple de la RDC, le cuivre est essentiellement produit par procédé SX-EW. Des problèmes antérieurs tels que les pénuries d'acide sulfurique et de soufre ont pu entraîner des réductions de production, et le volume affluant vers la Chine devrait connaître une augmentation significative limitée à l'avenir. De plus, il a récemment été observé sur le marché spot que certaines cargaisons EQ proviennent de pays tels que le Chili, qui produisent principalement du cuivre enregistré, ce qui signifie que la proportion réelle de cathodes de cuivre EQ entrant en Chine est estimée supérieure à ce que suggèrent les statistiques ci-dessus.

![Les stocks sociaux de cuivre en Chine continuent de se déstocker, les tendances régionales divergent fortement [Données hebdomadaires SMM]](https://imgqn.smm.cn/usercenter/YIaMU20251217171711.jpg)