En 2024, le stock d'IDE chinois en RDC atteignait 4,27 milliards USD, le secteur minier agissant comme moteur principal avec une contribution de 4,36 milliards USD aux caisses publiques — soit près de 47 % des recettes fiscales totales en 2024. L'écosystème industriel est ancré par la GÉCAMINES, avec une participation substantielle de consortiums chinois — menés par CMOC, Sicomines, Zijin Mining et CNMC. Ces organisations, aux côtés de majors occidentales comme Glencore et ERG, constituent le noyau d'investisseurs en concurrence pour les ressources premium de Tier-1 de la région.

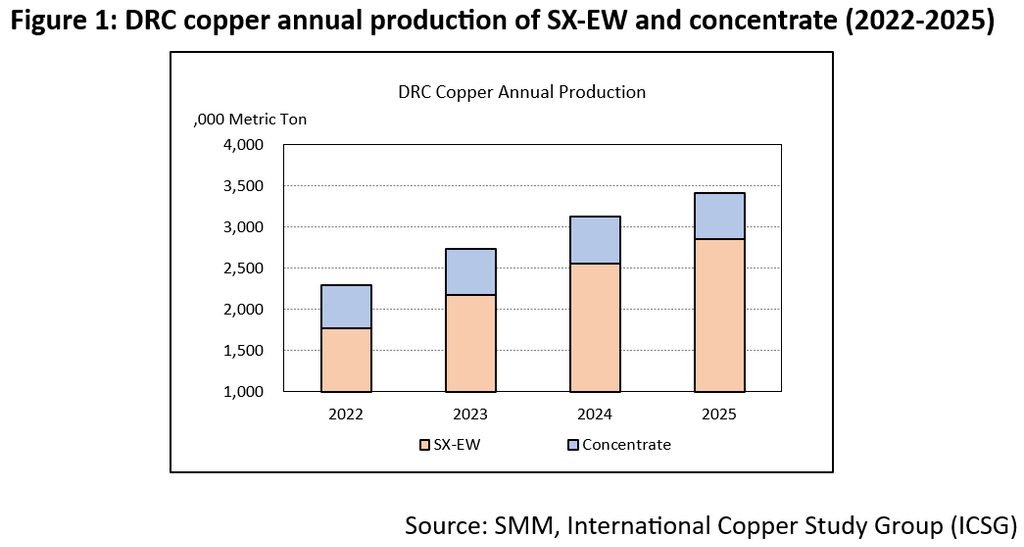

La production totale de cuivre en RDC est passée de 2,4 Mt en 2022 à 3,4 Mt en 2025, la part de la production SX-EW augmentant de 77 % à 83 % sur la même période. Cette croissance de la production SX-EW par lixiviation devrait entraîner une hausse de la demande en acide sulfurique, mettant sous tension l'approvisionnement régional à mesure que les producteurs augmentent leur production. La production SX-EW de la RDC a atteint jusqu'à 2,8 Mt en 2025, mais cette capacité repose sur une base logistique fragile tant pour les chaînes d'approvisionnement en acide qu'en énergie.

Actuellement, la RDC dépend de trois sources principales d'acide : les importations d'acide en provenance de Zambie, les importations de soufre du Moyen-Orient et l'acide coproduit des usines de concentrés domestiques.

Pour maintenir sa production de cuivre, la RDC a importé environ 2,7 Mt de soufre en 2023, dont environ 80 % provenaient du Moyen-Orient. Cette dépendance est encore aggravée par la diminution de l'offre régionale : même avant l'interdiction d'exportation de la Zambie en 2025, les flux d'acide sulfurique en provenance de Zambie avaient déjà chuté de 750 kt en 2022 à 480 kt en 2024. Parallèlement, la production d'acide des usines de concentrés domestiques a plafonné à environ 550 kt depuis 2022. Ce déficit croissant entre l'offre et la demande suggère que la croissance continue de la production SX-EW en 2025 et 2026 a été alimentée par une consommation accrue d'acide, alourdissant davantage la pression sur la fragile route commerciale du soufre moyen-oriental. La production d'acide de Kamoa-Kakula au T1 2026, avec 118 kt, constitue un tampon régional servant de compensation partielle. Selon notre visite, les stocks portuaires actuels de soufre sont estimés à environ 200 000 t, fournissant un tampon critique à court terme capable de soutenir les opérations en cas de perturbations immédiates de l'approvisionnement.

L'investigation sur site montre en outre que la consommation d'acide sulfurique varie parmi les fonderies de cuivre en RDC d'environ 3,0 t/t de cuivre à 6,0 t/t de cuivre. L'augmentation de la consommation d'acide est principalement due à la détérioration de la teneur du minerai et à la transition minéralogique des minerais oxydés vers des minerais mixtes et sulfurés. Cela a incité les usines SX-EW à moderniser leur technologie pour surmonter les défis liés au minerai.

La pénurie d'énergie est devenue le principal facteur limitant le fonctionnement stable des fonderies de cuivre en RDC. Malgré une capacité installée d'environ 2 800 MW en 2025, la fiabilité réelle du réseau de la RDC reste fragile, ne répondant qu'à 40 % des besoins du district minier du Katanga.

La transition vers le diesel s'avère financièrement insoutenable. Une série de mesures fiscales agressives a fait grimper la taxe d'accise spéciale sur le diesel de 0,65 USD/L en 2025 à 1,48 USD/L en mars 2026. Combiné à la volatilité des prix mondiaux, le coût total taxé a bondi à 3,38 USD/L. Par conséquent, les coûts de l'électricité produite au diesel ont doublé pour dépasser 0,8 USD/kWh depuis fin 2025. Cela a créé un écart croissant : les grands acteurs de premier rang disposant de sources d'énergie renouvelable maintiennent un plancher compétitif, tandis que les petits opérateurs, piégés dans une production d'électricité au diesel à coût élevé, font face à un effondrement des marges. Comme le diesel alimente l'ensemble de la chaîne de valeur — des flottes mobiles 100 % diesel dans les mines à ciel ouvert aux générateurs diesel massifs pour la fusion et le raffinage — toute augmentation du coût du carburant déclenche un effet cumulatif sur les marges.

De plus, en tant que pays enclavé, les infrastructures en RDC demeurent un goulot d'étranglement majeur. Sur 58 000 km de routes nationales, seulement 23 % sont bien entretenues. Ces infrastructures défaillantes, combinées à la congestion à Dar es Salaam et dans d'autres ports clés, ont fait passer le temps de transit pour 2 millions de tonnes d'exportations de métaux chaque année de 12 jours à plus de 25 jours. Le réseau ferroviaire de 5 000 km reste largement délabré en raison de normes incohérentes et de sa conception à voie unique. Les frais de fret ont augmenté de plus de 10 % par rapport au niveau de 2025, principalement en raison de la flambée des prix du diesel. Couplés à un doublement du cycle de transport, ces goulots d'étranglement pèsent directement sur la liquidité en allongeant les cycles de fonds de roulement tant pour les intrants de matières premières que pour les exportations minérales.

Les coûts d'exploitation de certaines fonderies de cuivre ont augmenté d'environ 3 000 USD/t par rapport aux niveaux de 2024. Cette escalade des coûts est principalement due à deux facteurs : des dépenses d'acide plus élevées et des coûts énergétiques en forte hausse. Ce changement redessine la courbe mondiale des coûts, faisant passer certains producteurs de la RDC de la tranche à faible coût vers la tranche à coût élevé. Un « seuil de survie » est désormais visible. Les entreprises disposant de leur propre énergie renouvelable et de leurs propres usines d'acide sulfurique peuvent encore absorber ces coûts. Cependant, les usines SX-EW autonomes — confrontées à une compression des marges — évoluent vers des marges nulles ou négatives et pourraient entamer des arrêts de maintenance anticipés dans le mois à venir.

SMM prévoit que la flambée des prix du soufre et du diesel sera de courte durée, avec une normalisation des prix à la fin du conflit en Iran. Toutefois, les mines font face à un défi à long terme à mesure que les opérations s'approfondissent, faisant de la transition minéralogique une certitude pour l'industrie. À l'avenir, l'expansion des usines de concentré en RDC augmentera l'offre locale d'acide sulfurique, réduisant progressivement les prix de l'acide. De plus, les coûts d'électricité devraient baisser avec la mise en service de projets hydroélectriques, photovoltaïques et de stockage d'énergie, résolvant enfin les pénuries d'électricité dans la Copperbelt. La technologie d'économie d'acide n'est plus un choix mais une nécessité. À mesure que les teneurs en minerai diminuent et que la minéralogie évolue, les usines incapables de réduire leur intensité en acide deviendront économiquement non viables, quel que soit le prix du cuivre.

Les groupes électrogènes diesel sont le seul choix pratique pour les besoins immédiats en raison de leur installation rapide, même s'ils sont le principal facteur de la crise actuelle des coûts. De nombreux projets d'énergie renouvelable devant être mis en service après 2027, certaines fonderies de cuivre en RDC pourraient devenir moins dépendantes de l'énergie diesel à l'avenir. Pour réduire la dépendance aux consommables importés coûteux, la région doit moderniser ses infrastructures ferroviaires et routières afin de raccourcir le cycle logistique à coût élevé.

Coordonnées : Chundi Feng

Téléphone : 447410506839

Email : chundi.feng@smm.cn

![Les tarifs douaniers et les facteurs géopolitiques ont fait monter le cuivre BC, l'écart de prix inversé entre Shanghai et le cuivre BC s'est légèrement réduit [Commentaire SMM sur le cuivre BC]](https://imgqn.smm.cn/usercenter/arNnt20251217171714.jpeg)