Driven by recovering risk appetite and China's peak demand season, copper prices both in China and abroad bottomed out since late March. However, as SHFE copper returned to the 100,000 level, the tug-of-war between longs and shorts increased, and futures prices shifted to range-bound consolidation. After the Labour Day holiday, copper prices quickly resumed their upward momentum. Today, prices opened higher with a gap and continued to rise, with SHFE copper just one step away from the record high set at the end of January, while LME copper hit a new closing high. What is fueling such strong confidence behind this rally?

Deepening Ore-Side Vulnerability Intensifies Supply Disruption Concerns

Since the suspension of First Quantum's Cobre Panama copper mine at the end of 2023, spot TC for copper concentrates in China has been caught in an endless downward spiral. Falling from around $80/dmt at the end of 2023, it largely dropped to single-digit levels and moved sideways in 2024. Entering 2025, it further plunged into negative territory, mainly due to successive production disruptions at world-class copper mines including Ivanhoe Mines' Kakula, Codelco's El Teniente, and Freeport's Grasberg mine in Indonesia. Entering 2026, global major copper ore supply growth remained limited, and the ore tightness showed no improvement. The latest data showed that spot TC for copper concentrates in China had fallen below -$90/dmt. With long-term contract TC at zero and spot TC declines accelerating, domestic smelters' production profits mainly relied on surging sulphuric acid prices and firm by-product prices of gold, silver, and other metals to compensate. It was reported that current sulphuric acid revenue could already cover smelters' procurement costs for copper concentrates and part of the processing costs, enabling domestic smelters to maintain relatively high operating rates, and the ore tightness had not yet notably transmitted to the smelting side.

It is worth noting that sulphuric acid is not only a by-product of pyrometallurgy but also a core production material for SX-EW copper. For every 1 mt of copper produced, 5–6 mt of sulphuric acid is consumed. Sulphuric acid costs account for 40%–50% of total SX-EW copper production costs, and SX-EW copper production accounts for approximately 20% of global mine copper production. Since the beginning of this year, sulphuric acid prices surged sharply due to multiple factors, and ex-China sulphuric acid supply was periodically disrupted, raising concerns that copper supply in some countries could be affected. Focusing on the reasons behind the sulphuric acid price surge: on one hand, since the escalation of the Middle East conflict on February 28, shipping through the Strait of Hormuz has been broadly restricted and has recently faced a dual blockade by Iran and the US. Sulphur exports from the Middle East have been impacted, with the DRC and Zambia being the most concentrated SX-EW copper producing regions that are highly dependent on sulphur imports from the Middle East. As sulphur supply has been constrained, sulphuric acid prices have naturally risen in tandem, not only raising local SX-EW copper production costs but also potentially triggering further production cuts if the Strait of Hormuz blockade continues and sulphur disruption risks escalate. On the other hand, to prioritise domestic spring ploughing phosphate fertiliser production and support new energy industry expansion, China has imposed a phased ban on sulphuric acid exports according to industry sources. Chile has a relatively high dependence on Chinese sulphuric acid, with SX-EW copper accounting for around 20% of its output, and the market is also concerned that Chile's SX-EW copper production may be affected.

In addition, against the backdrop of an already fragile copper ore supply, frequent news shocks from outside China recently have undoubtedly intensified market concerns. Last week, market rumours suggested that the full restart of Indonesia's Grasberg copper-gold mine, which declared force majeure in September last year, had been delayed by one year, driving SHFE copper sharply higher in the afternoon of 8 May. However, according to the latest update from Freeport-McMoRan, the company still expects Indonesia's Grasberg copper-gold mine to fully resume production by the end of 2027, reaffirming the plan outlined last month and refuting reports that production resumptions could be delayed to 2028. Furthermore, yesterday Peru declared an emergency energy decree due to a natural gas pipeline explosion. Peru's copper production reached 2.63 million mt in metal content last year, ranking third globally. Copper mining and smelting are relatively sensitive to power stability, and the market is concerned that Peru's energy strain may disrupt local copper supply.

Overall, China's copper cathode production remains relatively stable, but some major global miners lowered their full-year production guidance in Q1, the ore tightness persists, sulphuric acid supply — a core raw material for ex-China SX-EW copper — is constrained, and there are multiple supply disruption themes on the copper supply side, which can easily boost copper prices once the macro front stabilises.

Global Copper Visible Inventory Divergence: China Destocking Provides Support

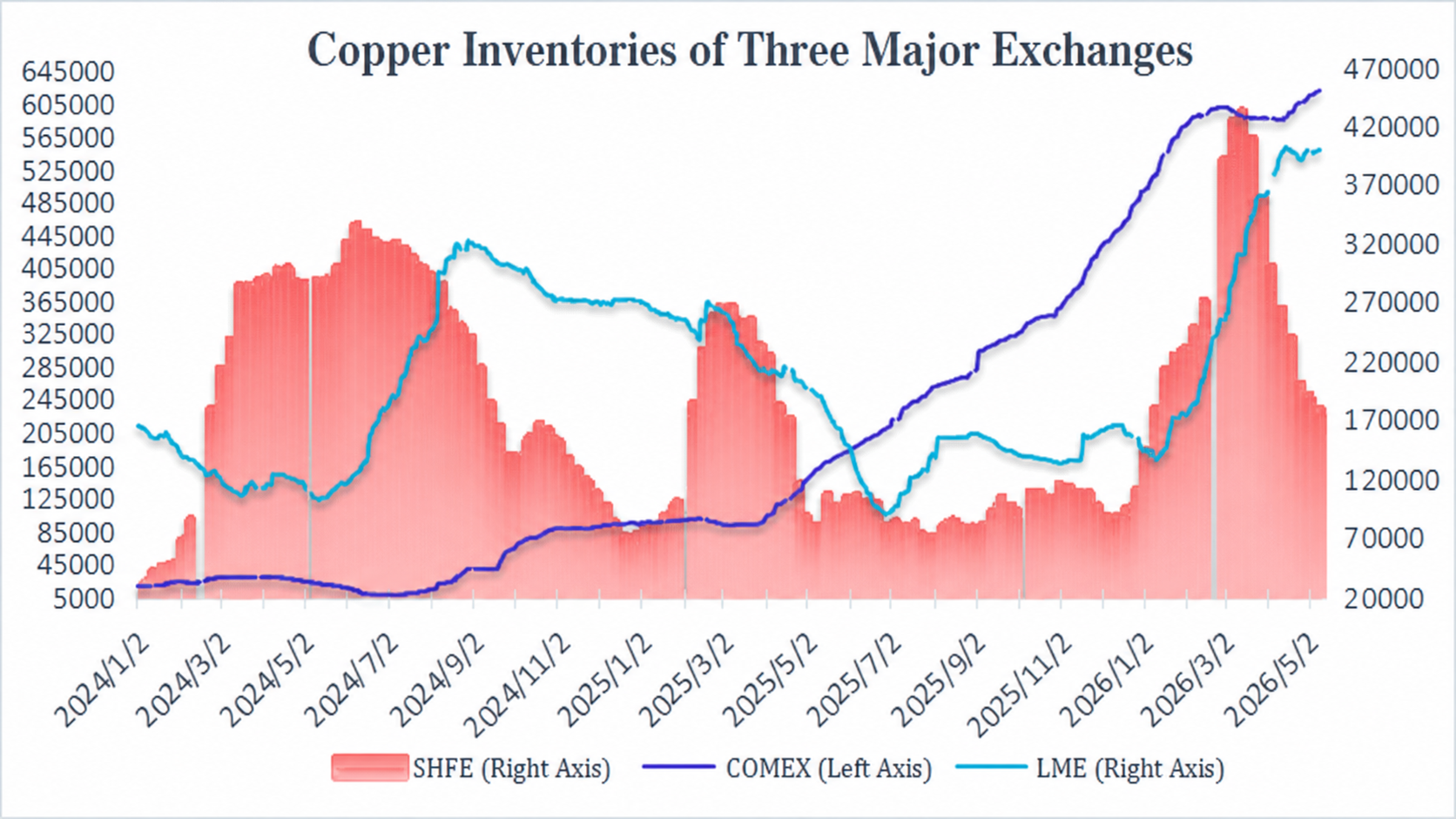

Last year, driven by the US government's threat to impose additional tariffs on imported copper, global copper continued to flow into the US, causing COMEX copper inventories to accumulate continuously while copper inventories in non-US regions remained low, providing sustained support for copper prices. In February this year, the US Supreme Court struck down most of the tariff measures introduced by the Trump administration in 2025. The Trump administration subsequently turned to Section 122 of the Trade Act of 1974 to push new global tariff policies. On 7 May, the US Court of International Trade issued a ruling stating that the legal basis for imposing a 10% global import tariff was invalid. The tug-of-war between US courts and the Trump administration over tariffs has continued recently, but the market has certain expectations that the US may subsequently impose additional tariffs on imported copper. Under such expectations, the price spread between COMEX copper and LME copper has shown a slight strengthening trend recently, meaning copper in LME warehouses still has the potential to flow to the US.

Specifically, COMEX copper inventories have continued to rebound since mid-April, rising from around 590,000 mt to the latest 620,000 mt, again hitting a multi-year high. Correspondingly, LME copper inventories pulled back from around 400,000 mt in mid-April, declining to 397,700 mt on 6 May. They have rebounded with fluctuations recently, but overall inventories have not exceeded the over-12-year high set in mid-April. SHFE copper inventories fell for the eighth consecutive week, currently dropping to 181,300 mt, the lowest since the beginning of the year.

Data source: Webstock Inc.

Overall, on the macro front, there are currently disagreements in US-Iran negotiations, but both sides continue the ceasefire with no recent signs of escalation in conflict. Energy prices pulled back from late April levels, inflation concerns eased somewhat, the US dollar index was in the doldrums, and combined with the AI boom lifting global stock markets, market risk appetite was moderate, providing a fertile ground for copper prices to strengthen. Focusing on copper's own fundamentals, inventories outside China remained elevated, but significant prior destocking of China inventories provided support. The ore tightness was difficult to reverse, and supply-side narratives were abundant, meaning copper prices may still hold up well. However, it is worth noting that the Middle East situation remains the biggest macro variable, and the policy path following the Fed Chairman's power transition also deserves close attention.

(Webstock Composite)

![Peru Mine Concerns Cause Disruptions, Copper Prices Hover at Highs [SMM BC Copper Commentary]](https://imgqn.smm.cn/usercenter/HaNSH20251217171714.jpeg)

![Copper Prices Rose Sharply While SHFE/LME Price Ratio Weakened, but Market Offers Stayed High [SMM Yangshan Spot Copper]](https://imgqn.smm.cn/usercenter/uoTGi20251217171713.jpg)