At the hosted by SMM, Ouyang Yichang, SMM secondary copper industry research analyst, shared insights on the topic of "Analysis of Japan's Secondary Copper Market." He noted that, according to SMM, Japan's copper scrap market is gradually transitioning toward a fiercely competitive "seller ecosystem." Trade models that rely solely on spot cargo procurement are increasingly exposed to the risk of supply disruptions. To secure long-term resource supply, ex-China purchasing enterprises need to move beyond the traditional spot trading mindset and establish structural partnerships through deep-binding approaches such as signing long-term contracts and equity cooperation, in order to adapt to the persistently tight market landscape.

Global Positioning of Japan's Copper Scrap Market

Global Positioning of Japan's Copper Scrap Market

Key Drivers Behind Japan's Leading Position in Asia

1 Precision Sorting:Exceptional classification accuracy ensures high-quality scrap output.

2 Well-Established Infrastructure:A mature "urban mine" system and advanced logistics provide a highly reliable supply foundation.

3 Strategic Geographical Advantage:Proximity to China (accelerating capital turnover), while serving as a key trans-Pacific logistics hub connecting the Americas and Asia.

4 Favorable Trade and Tax Policies:Zero export tariffs and transparent regulations ensure seamless global operations.

5 Commercial Reliability:High standards of packaging and business ethics minimize quality claims.

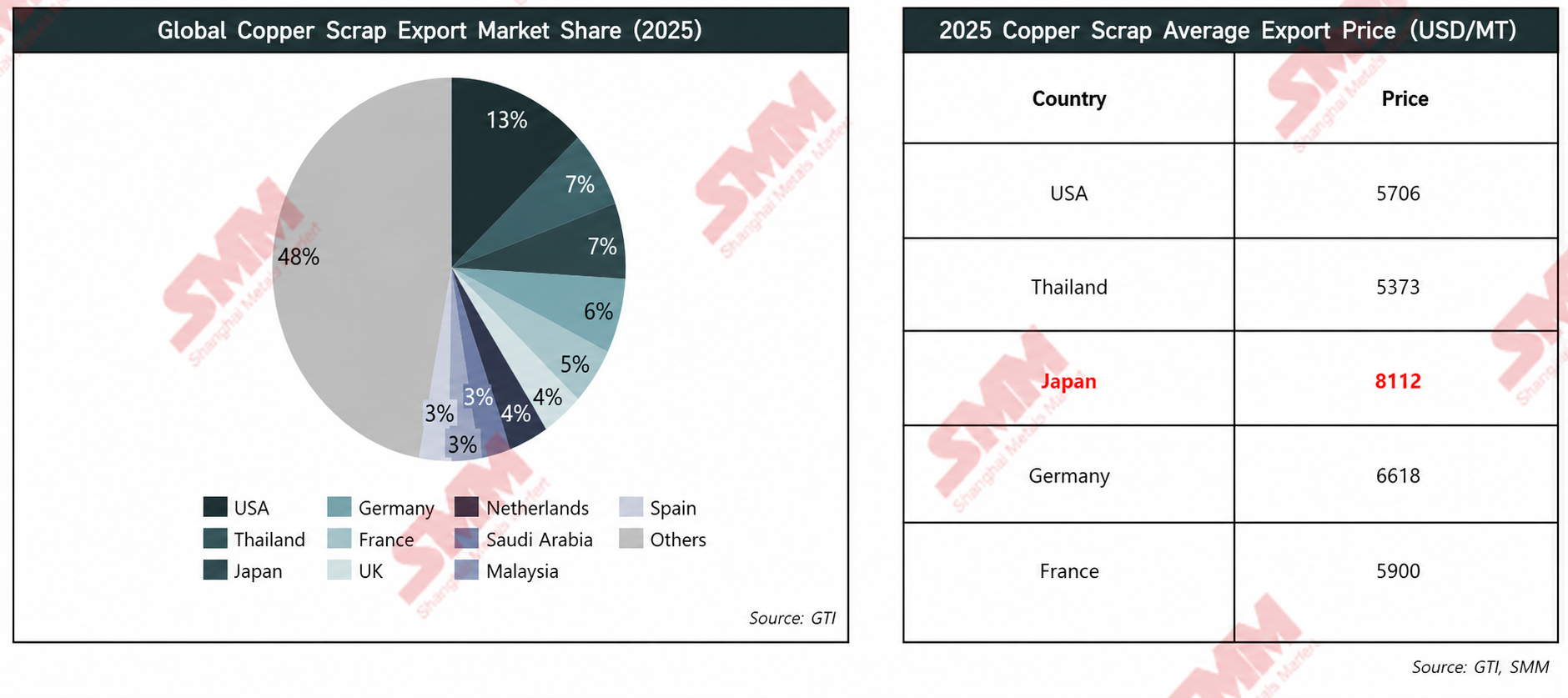

Japan's Average Unit Price of Copper Scrap Significantly Leads the Top Five Global Exporters

In 2025, Japan and Thailand each accounted for approximately 7% of global copper scrap exports. However, Japan commanded the highest average export price among major peers ($8,112/mt), thanks to a substantial quality premium.

This price spread revealed fundamental differences in product mix. Thailand primarily served as a processing hub, with limited high-grade copper scrap output domestically. In contrast, Japan was organically driven by its mature "urban mine" ecosystem, consistently producing high-purity, high-grade materials.

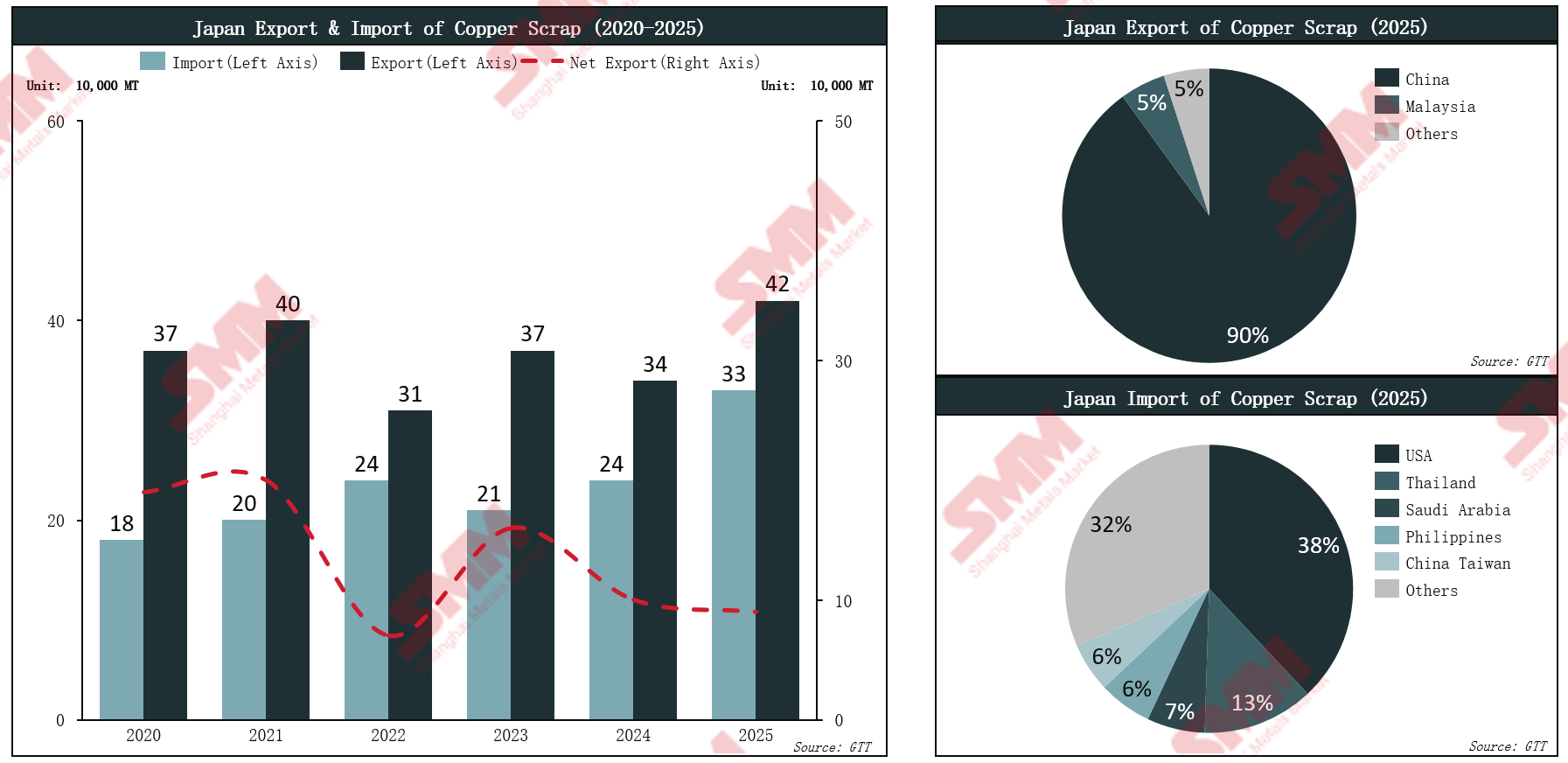

Flow of Japan's Copper Scrap

Flow of Japan's Copper Scrap

Rising Trade Volume and Shrinking Net Exports: A Shift Toward Domestic Retention

Smelters Drove Copper Scrap Consumption Growth While Downstream Processing Enterprises Saw Declining Usage

According to SMM, compared with 2021, processing enterprises' copper scrap usage declined by 8% in 2025.

Processing enterprises:Weak downstream demand (automotive, construction) and fierce global competition for high-quality copper scrap severely squeezed domestic processing enterprises, resulting in a sustained 8% decline in their absolute usage.

Smelters:Tightened environmental protection and export policies implemented since 2023 restricted the outflow of copper scrap, significantly accelerating this structural "reflux" toward smelters. Combined with the plunge in TC/RC, Japanese smelters were forced to rely on these raw materials to maintain production.

Consequently, the share of copper scrap consumed by the smelting segment has maintained an overall upward trend in recent years.

Japan's overall scrap supply is contracting; despite robust growth in domestic consumption, the structural decline in net exports is the primary driver.

Since the 2021 peak, Japan's total apparent supply of copper scrap has been on an overall downward trend. This indicates structural tightening in domestic scrap generation and social recovery rates, with increasingly scarce available resources.

Despite the overall supply contraction, domestic apparent consumption demonstrated strong resilience, as Japanese smelters actively secured local raw materials to maintain production amid plunging TC.

This robust local demand is significantly squeezing exports. Net exports have consequently declined structurally to low levels. Japan is shifting from a "resource overflow" model to an "internal absorption" model, which will severely exacerbate raw material shortages for Southeast Asian and Chinese buyers.

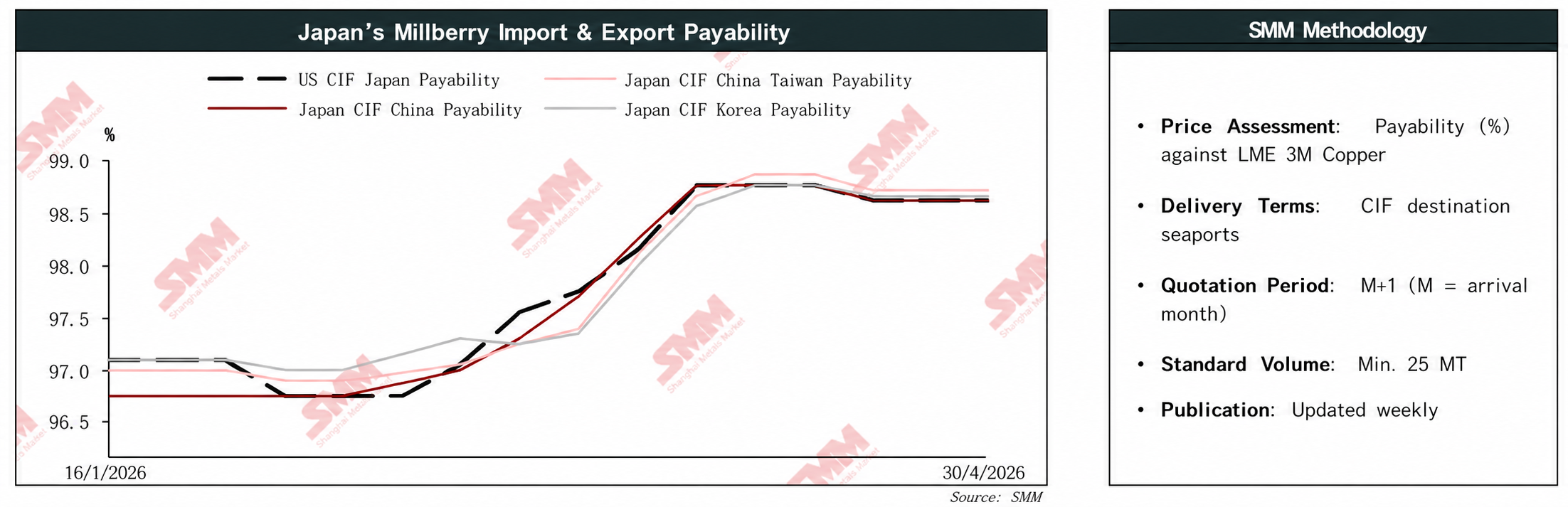

Bare bright copper payable indicator stays high: supply tightness and China's tax-driven demand outweigh the impact of recent copper price rebound

Since early 2026, market copper prices have risen steadily overall; in March, copper prices experienced a periodic pullback, and copper scrap sellers held prices firm with strong willingness to defend price floors, directly driving the bare bright copper payable indicator passively higher.

Entering April, futures copper prices rebounded and stabilized at highs, but the copper scrap payment ratio deviated from conventional pricing logic and did not pull back accordingly, remaining firmly in the 98.5%-99.0% range.

The core supporting logic lies in: continued tightening of domestic tax regulation, with China's downstream processing enterprises increasingly relying on imported copper scrap to obtain compliant input tax deductions, forming rigid procurement demand; coupled with tight spot copper scrap supply, the dual support of supply and demand underpins the copper scrap payment ratio to stay high.

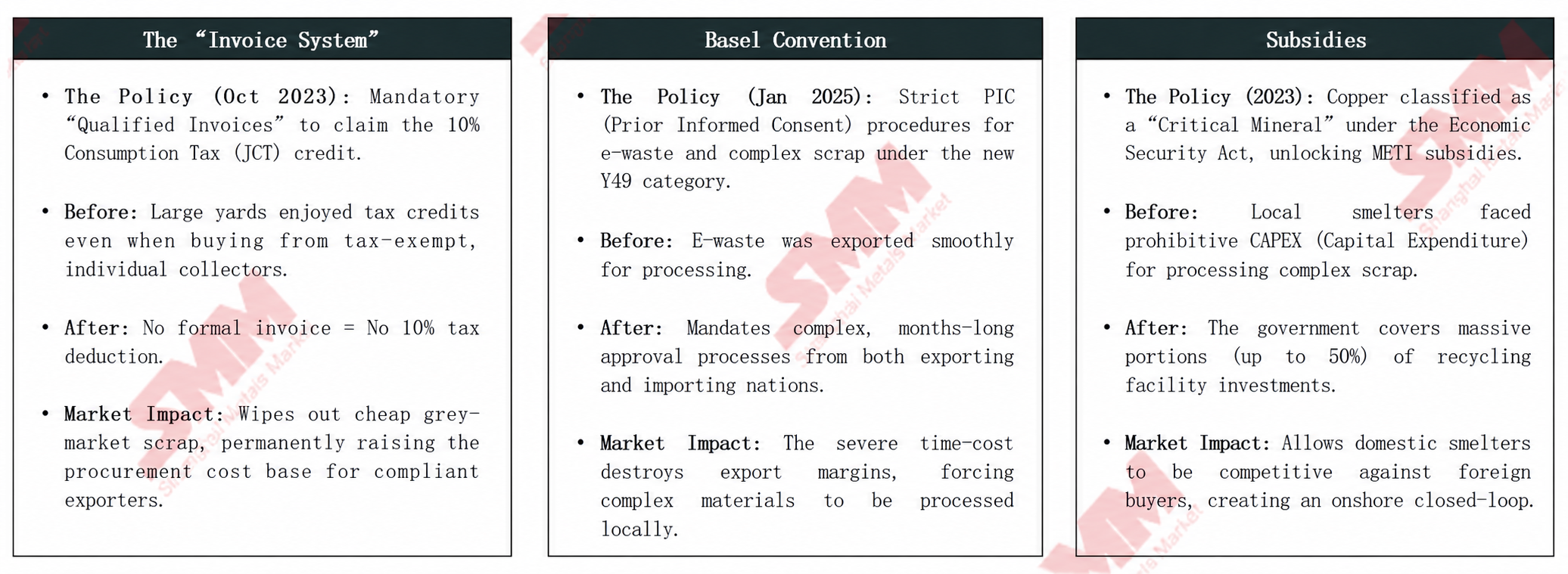

Japan's Scrap Policies

Japan's Scrap Policies

Regulatory Shift: Building an "Invisible Wall"

Although Japan has not explicitly imposed export bans, it strengthens its domestic closed-loop system through a strategic policy combination.

For global buyers, this signals a structural shift in the Japanese market going forward: intensified competition, soaring procurement costs, and increasing difficulty in accessing high-quality scrap.

Regulatory maturity and standardized transparency are the primary drivers of the "Japan premium."

Policy Lag vs. Market Reality:Although the EU Waste Shipment Regulation and potential US export restrictions have not yet been formally enacted, the market has already priced in expectations of future supply contraction, compelling downstream buyers to proactively pivot toward trade hubs with higher compliance and transparency.

"Reliability Premium" Logic Emerges:As a pioneer in industry compliance and market transparency, Japan can effectively hedge against risks prevalent in other regions, such as insufficient information transparency and origin rerouting, providing the market with an important safe-haven and pricing anchor function.

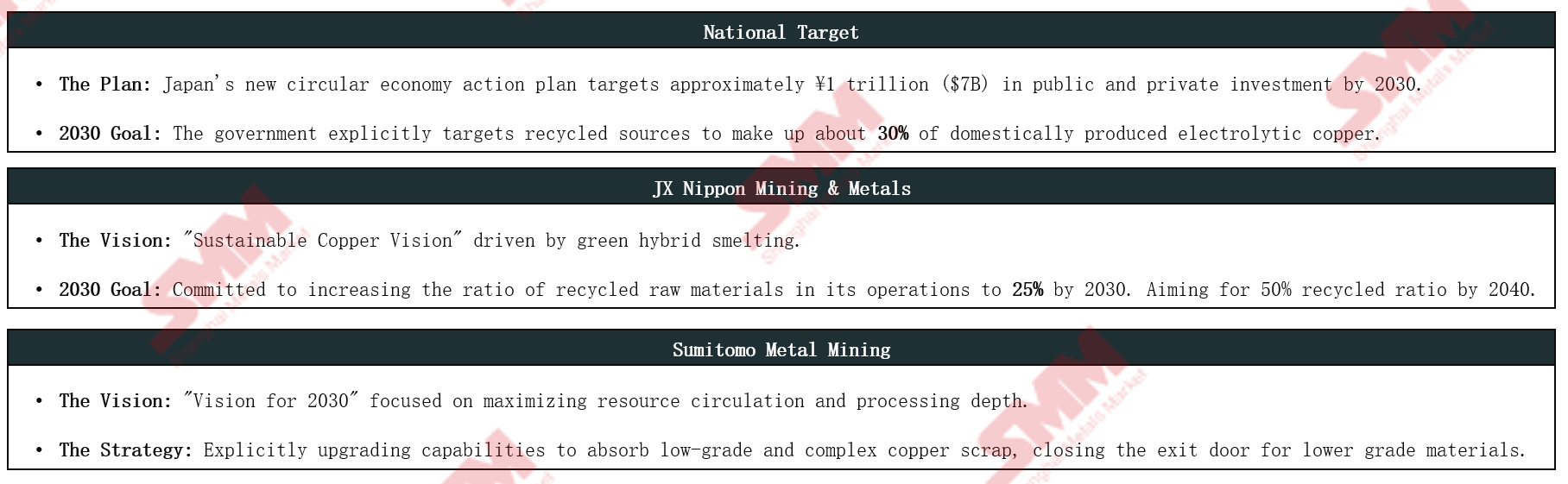

Outlook and Forecast

Strategic Outlook and Forecast

Driven by aggressive development targets at both enterprise and national levels, scrap consumption by domestic smelters in Japan is set to experience significant structural growth.

According to SMM, the climb in scrap consumption by Japanese smelters is not a short-term cyclical response triggered by declining mine TCs, but rather a fundamental structural transformation underpinned by strong capital strength and long-term commitment.

As 2030 ESG-related targets continue to materialize, the trend of retaining domestic scrap for internal use in Japan will deepen further, structurally tightening global circulating scrap supply over the long term and continuously compressing the available sourcing volume for ex-China buyers.

Response Logic for the "New Normal" in Japan's Copper Scrap Market

Volume and Flow Direction: Steady Decline

Net exports of copper scrap will not plunge to zero abruptly, but rather exhibit asustained structural declinetrend. As domestically subsidized capacity comes fully online, exports of high-grade secondary copper such as bare bright copper and No.1 copper will enter a steady contraction trajectory.

Pricing Logic:

The traditional medium and long-term linkage of "rising copper prices, declining scrap payment ratios" has been structurally reshaped.

Under the dual effects of persistently tight copper concentrates supply and China's rigid tax-driven procurement demand providing a floor, the payment ratio for Japan's high-quality copper scrap is expected to establish a long-term upward baseline.

Strategic Pivot:

Constrained by the upper limit of domestic secondary copper output and tight labor supply, Japanese recycling industry alliances will accelerate their expansion into markets outside China.

Japanese enterprises will invest in overseas joint venture projects to solidify downstream processing capacity deployment while maintaining Japanese-led control over raw material supply chains.

According to SMM analysis, the current Japanese copper scrap market is gradually transitioning toward a fiercely competitive "seller ecosystem." Trade models that rely solely on spot purchases are increasingly exposed to the risk of supply disruptions. To secure long-term resource supply, ex-China purchasing enterprises need to move beyond the traditional spot trading mindset and establish structural partnerships through deep-binding approaches such as signing long-term contracts and equity cooperation, thereby adapting to the persistently tight market landscape.

![Downstream Buyers Took a Wait-and-See Approach Amid Surging Copper Prices, Spot Cargo Trading Activity Remained Weak [SMM North China Spot Copper]](https://imgqn.smm.cn/usercenter/oeWiG20251217171714.jpeg)

![Copper Prices Hit New Highs as Downstream Buyers Reluctant to Restock, Overall Trading Remains Poor [SMM South China Spot Copper]](https://imgqn.smm.cn/usercenter/ULCXN20251217171714.jpeg)