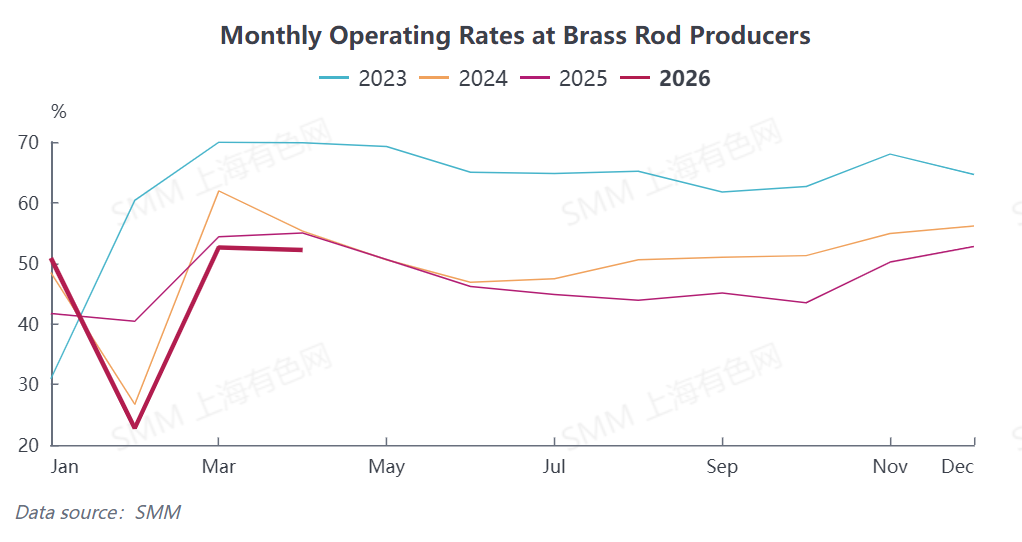

According to SMM data, the comprehensive operating rate of copper billet producers in China was 52.18% in April, down 0.41 percentage points MoM and down 2.79 percentage points YoY. Overall operating levels continued their weak trend, with divergence among enterprises becoming more pronounced.

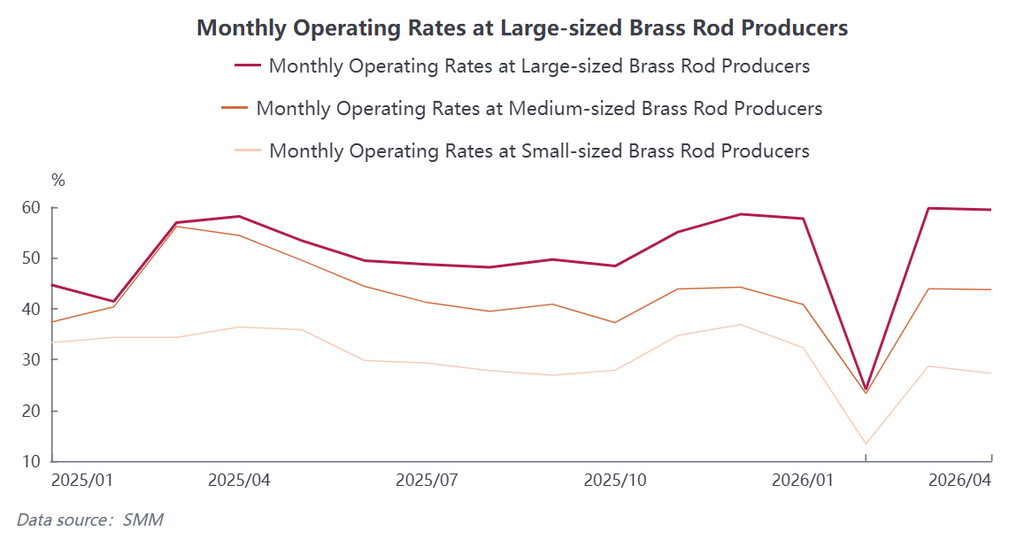

By enterprise scale, large enterprises, leveraging stable raw material channels, order resources, and capital advantages, maintained operating rates at a relatively high level of 59.48%. Medium-sized enterprises recorded an operating rate of 43.74%, with production pace slowing down under dual pressures of order instability and raw material costs. Small enterprises, constrained by difficulties in raw material procurement, insufficient orders, and cost pressures, posted an operating rate of only 27.28%.

In early April, orders for copper billet producers were moderate, with orders from home appliance heat dissipation and power supporting sectors underpinning production. However, entering late April, end-use demand weakened notably, compounded by multiple factors that sapped production momentum. Raw material side, recycled brass raw materials remained in tight supply, imported secondary brass supply was tight, and raw material prices fluctuated at highs, pushing up production costs. Some small and medium-sized enterprises were forced to cut production due to insufficient raw materials or loss pressures, directly dragging down operating rates. Demand side, end-users showed insufficient enthusiasm for cargo pick-up, and enterprises continued to destock finished product inventories to mitigate price fluctuation risks, further contracting production pace.

By downstream sector, orders in the refrigeration sector pulled back after a phased release in April as the off-season approached. Orders in traditional application fields such as bathroom hardware and mechanical components were overall mediocre, with the market lacking new growth drivers. Only structural sectors such as new energy supporting and power maintained relatively stable orders, offering limited boost to the industry's overall operating rate.

Looking ahead to May, China's copper billet industry is expected to gradually enter the traditional consumption off-season, with end-use demand from downstream sectors such as refrigeration and home appliances expected to weaken further, while orders from traditional markets such as bathroom hardware are unlikely to see significant improvement. Raw material side, tight supply of imported secondary brass is unlikely to ease significantly, and prices fluctuating at highs are expected to continue squeezing enterprise profit margins. Additionally, some enterprises, concerned about insufficient raw materials affecting delivery, are becoming more cautious in taking orders, with limited incremental new orders. SMM expects the operating rate of copper billet producers in China to pull back 3.96 percentage points MoM to 48.22% in May, down 2.39 percentage points YoY, with the industry's overall operating level expected to come under further pressure.

![Copper Prices Rise, Consumption Suppressed, Spot Premiums Decline [SMM North China Spot Copper]](https://imgqn.smm.cn/usercenter/XBbTq20251217171709.jpg)

![Copper Prices Surged with Weak Consumption, Suppliers Actively Adjusted Prices for Shipments [SMM South China Spot Copper]](https://imgqn.smm.cn/usercenter/arNnt20251217171714.jpeg)