The 2026 SMM London H1 Seminar concluded on April 29 with great success, bringing together global metals and commodities leaders for a day of high-level dialogue and actionable insights.

The seminar drew over 160 valid pre-registrations and more than 100 on-site attendees, gathering core practitioners, senior experts, research scholars and institutional representatives across the global non-ferrous metals industrial chain.

Centered on copper, aluminum, lead and zinc, the event delivered in-depth insights into current industry performance, supply-demand shifts and future market outlooks. It also featured two high-level panel sessions with distinguished guests, who exchanged views on key industry highlights such as geopolitical impacts, global trade restructuring, cross-market arbitrage and divergent commodity fundamentals.

The event comprehensively reviewed the macro backdrop of commodities as well as opportunities and risks in base metals, offering professional references and forward-looking insights for global non-ferrous market participants.

SMM Industry Analysis: Copper, Aluminum, Nickel, Lead & Zinc

- Geopolitics and Metals: Pricing the New Global Risk Premium

- How rising geopolitical tensions are reshaping global supply chains, macro risk, and base metal price formation.

Dr. Yanchen Wang, Managing Director of SMM Global UK Ltd., provided analysis on macro trends and the aluminum and nickel markets. From a macro perspective, he noted that global economic uncertainty has intensified, with the IMF cutting global GDP growth forecast. China's exports may serve as a key economic pillar in 2026. Power sector investment increased significantly from January to February 2026. The State Grid Corporation of China will ramp up investment during the "15th Five-Year Plan" period.

In terms of the aluminum market, Chinese smelters saw improved profitability and higher operating rates. Weak demand in Q1 combined with rising aluminum prices drove inventory to rise. Outside China, new aluminum capacity additions in Indonesia in 2026 are expected to be substantial, with SMM estimating approximately 950,000 mt of new aluminum smelting capacity potentially coming online in Indonesia in 2026. Angola is attracting Chinese investment thanks to its hydropower advantages.

In the nickel market, given the Indonesian government's tightening of quotas, SMM estimates Indonesia's RKAB supplementary quotas this year at approximately 15%-20%. In terms of supply outside China, constrained by a lack of new projects, imports from the Philippines are expected to remain at around 19 million mt. Considering the impact of the rainy season on production, the market is expected to maintain a tight balance.

Shairaz Ahmed, Principal Market Analyst & Client Advisor at SMM, shared insights on the global copper market. He noted that global copper cathode demand will continue to grow from 2025 to 2030, with demand potentially reaching around 32 million mt by 2030 in an optimistic scenario. China's copper concentrates still rely on imports, and global copper concentrates supply will remain tight from 2026 to 2028, with the downward trend in spot TC not yet over. Meanwhile, global copper cathode production growth will slow down in the future, and the market will most likely fall into a supply deficit from 2027 to 2030, providing long-term support for copper prices.

Yueang He, Senior Lead & Zinc Analyst at SMM, interpreted the lead-zinc market trends for 2026. Looking at the global zinc concentrates market in 2026, he stated that although production in China, Africa, and some projects continues to ramp up, production cuts at large mines are suppressing overall supply, with China's zinc concentrates production estimated to be up 4.8% YoY to 3.95 million mt in 2026; European smelting, affected by electricity prices fluctuations, may see selective minor production cuts of 60,000-100,000 mt. Overall, the zinc concentrates market in and outside China will maintain a tight balance in 2026, with refined zinc showing a surplus in China and a deficit ex-China.

In terms of lead market, he stated that global lead mine supply is gradually recovering, but the concentrates market remains tight, and TC is unlikely to rebound significantly in the short term. He estimates that the loose supply situation in the global refined lead market will persist until 2028, with high visible inventory on both exchanges combined with slightly soft battery demand in China limiting the upside room for lead prices.

Panel Session — Positioning and Price Signals: What Are Commodity Markets Telling Us?

Understanding market positioning, inventory signals, and cross-market arbitrage.

Moderator:

Shairaz Ahmed, Principal Analyst & Client Advisor at SMM

Panelists:

David Lilley, Director and Co-CIO at Drakewood Capital Management Limited

Maruis Van Straaten, Metals Research Analyst at Squarepoint

Gregory Shearer, Head of Base Metals and Precious Metals Strategy at J.P. Morgan

Loic Jonchery, Base Metals Trader at Gunvor

The panelists focused on current mainstream cross-market arbitrage strategies, emphasizing the need to closely track premiums and futures price spreads across various commodities, while comparing price spread performance across upstream and downstream categories such as cathode materials, scrap, and intermediate products, leveraging signals to identify arbitrage opportunities. The current market is subject to multiple influences including policy constraints, supply adjustments, and changes in industry rules, with the overall landscape becoming increasingly fragmented. China's policies have imposed a supply ceiling, compounded by industry framework adjustments and lengthy implementation cycles, keeping small and medium-sized enterprise operations and the supply side persistently tight, increasing market friction, and creating significant uncertainty in arbitrage trading.

In this complex environment, price spread fluctuations have amplified and ranges continued to widen, with enhanced trend continuity in underlying markets; combined with cross-regional approval processes and circulation restrictions, traditional arbitrage logic has broken down and trade execution difficulty has increased. At the sub-sector level, the copper market attracted high attention, while structural distortions in nickel and other categories became prominent, making conventional arbitrage and sales models difficult to execute consistently; quality arbitrage opportunities concentrated among entities with balance sheet advantages, while ordinary participants became more cautious in decision-making, with overall trading behavior turning more conservative.

Overall, the guests believed that there is no universally applicable, low-risk cross-market arbitrage strategy in the current market. Logic across different sub-markets has diverged significantly, and conducting related trades requires thorough assessment of policy, circulation, and fundamental risks.

Panel Session: Superpowers and the Battle for Base Metals

Moderator:

Dr. Yanchen Wang, Managing Director of SMM Global UK Ltd.

Panelists:

Natalie Scott-Gray, Senior Metals Analyst, Middle East, North Africa and Asia, StoneX

Max Layton, Global Head of Commodities Strategy, Citi

Helen Amos, Managing Director and Commodities Analyst, BMO Capital Markets

Amy Gower, Executive Director, Head of Metals and Mining Commodities Strategy, Morgan Stanley

Amy Gower stated that since H2 last year, they have held a structurally bullish view on aluminum fundamentals: China's aluminum capacity is approaching its ceiling, and combined with expectations of incremental supply from Indonesia, the bullish logic for the aluminum industry is concentrated in H2. Currently, supply-side tightening in the aluminum market has gradually materialized, but the tightness has not been fully reflected in futures prices, and is instead more evident in strengthening spot premiums. Year-to-date, three-month aluminum has risen 18%, with European spot premiums at 27%.

In addition, the guests noted that due to geopolitical factors, countries are increasingly prioritizing self-sufficiency and controllability of critical material supply chains, rather than relying on globalized supply allocation. Combined with various policy interventions, the previously freely flowing global commodities market is gradually moving toward regionalization and localized fragmentation. On the trade front, markets have become more unpredictable, and understanding the market is crucial. Some guests mentioned that interest rate trajectory is a key variable, and they expect that after interest rates decline from 2027 to 2028, supply-demand and inventory dynamics will further materialize. Meanwhile, upgraded supply chain governance and the normalization of strategic reserves across countries will provide long-term support for commodities price resilience.

Session 4: How Do SMM Data and Information Products Empower Commodities Decision-Makers?

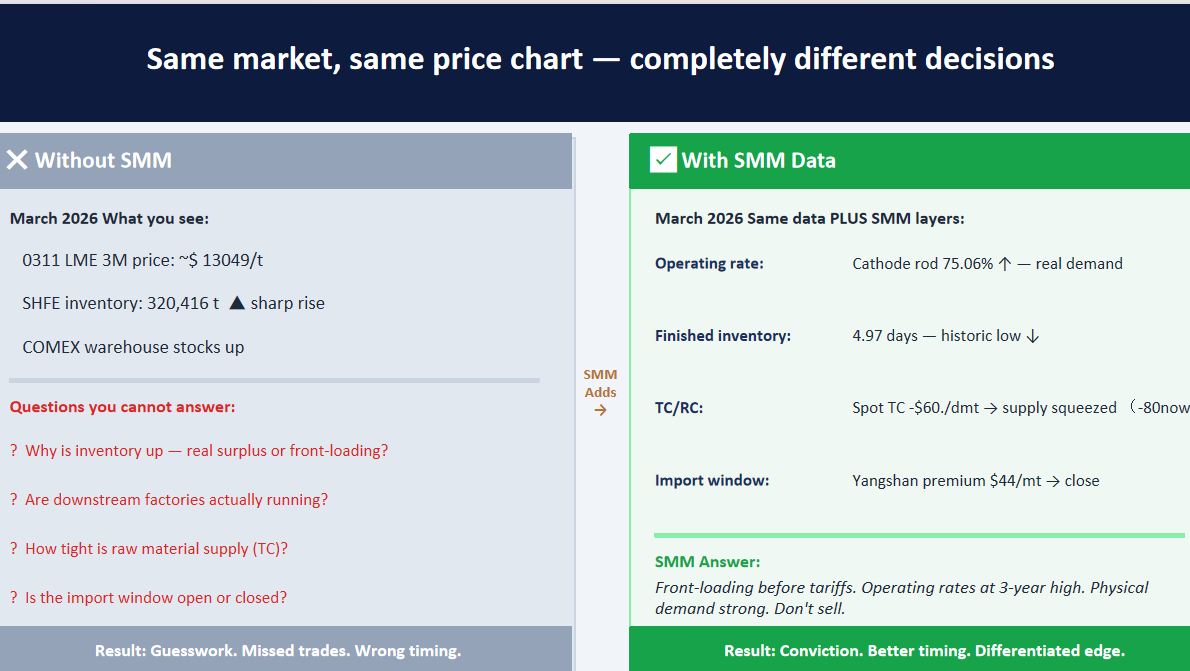

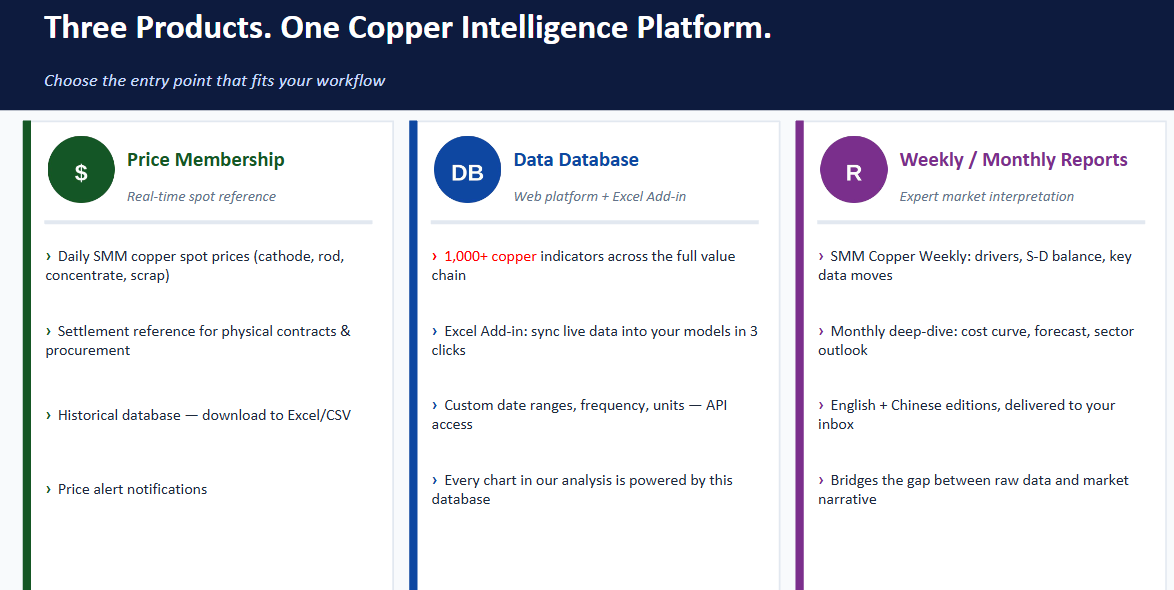

As a globally renowned non-ferrous metals price assessment platform, Shanghai Metals Market (SMM) is committed to providing superior data to clients worldwide, empowering them to make more precise decisions. SMM understands that in a complex and ever-changing market environment, accurate and timely data is the key to success. To this end, SMM has built a comprehensive data platform covering multiple metals including copper, aluminum, lead, zinc, and nickel.

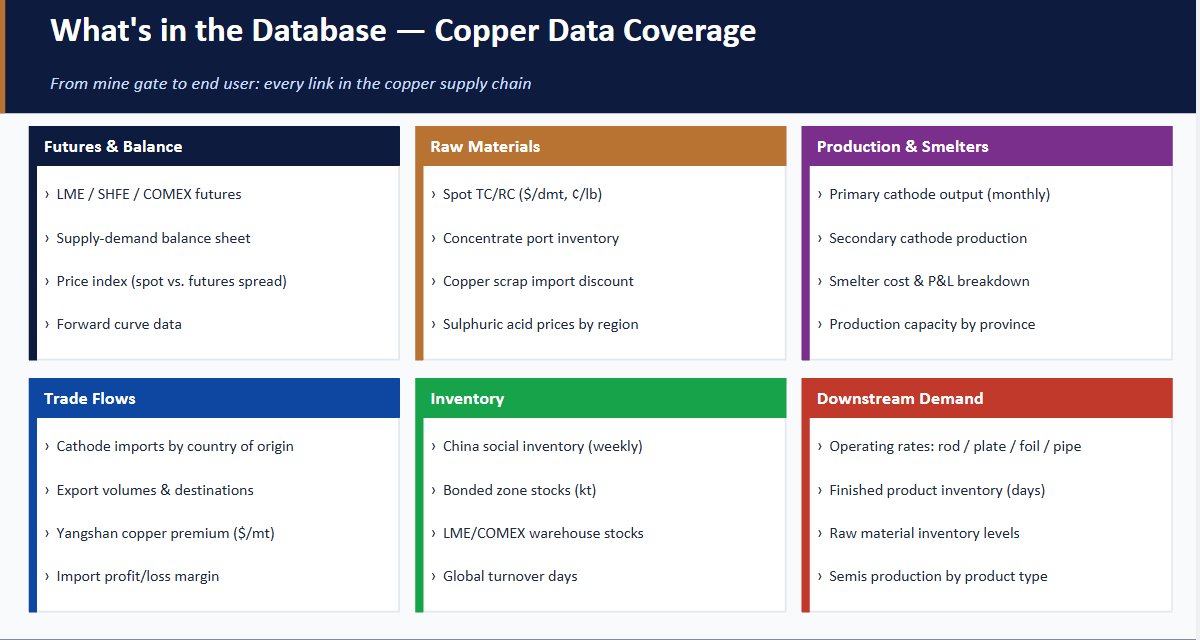

Taking the copper market as an example, the SMM database covers the entire industry chain from mines, smelting, trading, and inventory to downstream demand, offering over 10,000 key indicators across sub-categories such as copper cathode, copper scrap, copper concentrates, copper anode, and sulphuric acid, including real-time spot prices, futures data, supply-demand balance tables, operating rates, and social inventory, comprehensively meeting clients' analytical needs.

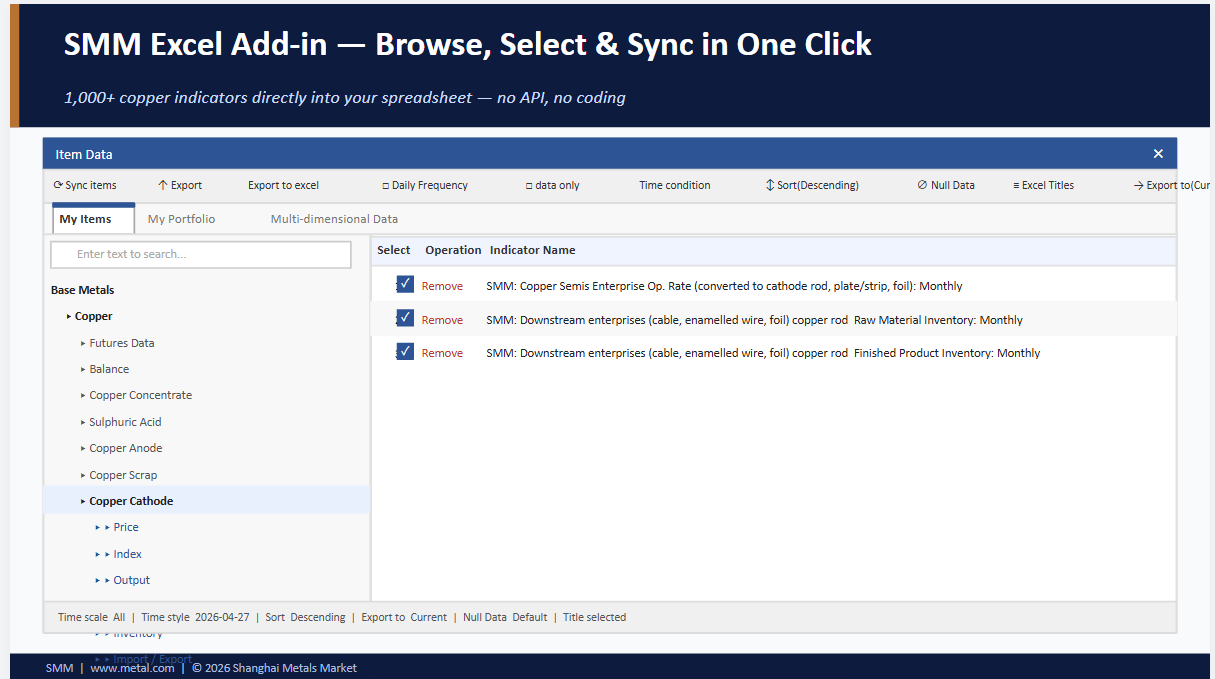

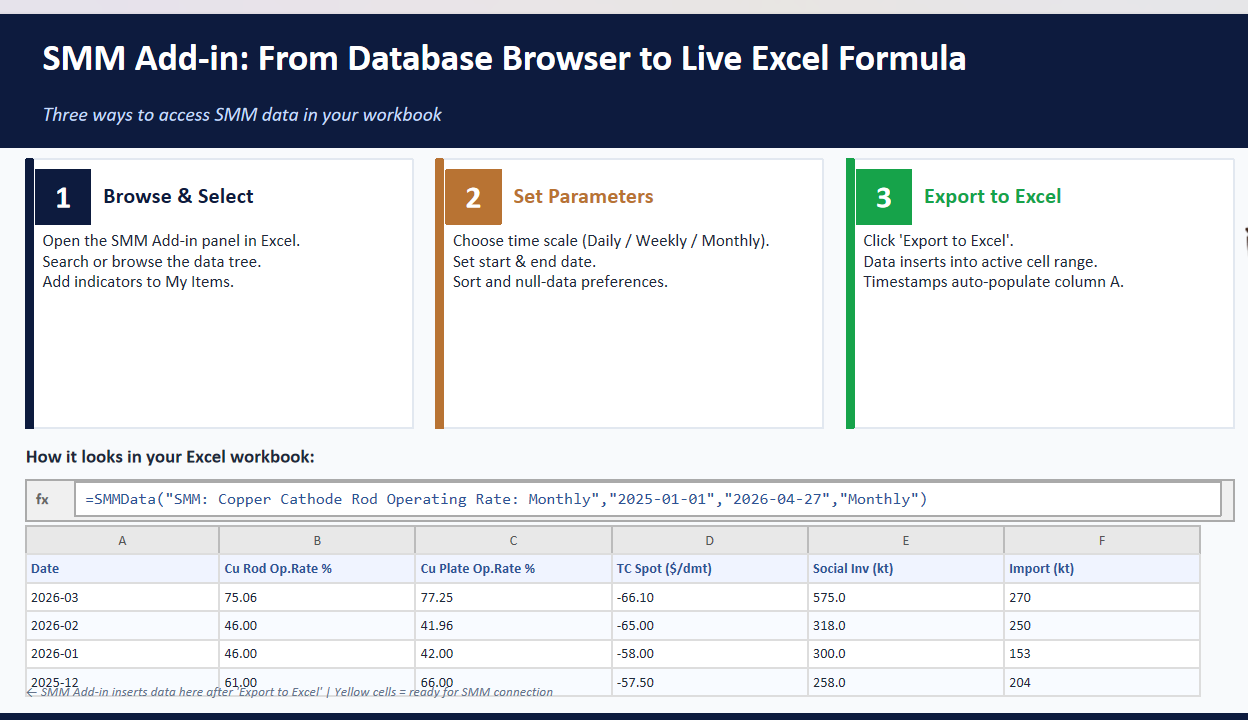

To make data access simpler and more convenient, SMM launched the SMM Excel Add-in. Users need no programming or API knowledge to browse, select, and sync massive amounts of data with a single click within the familiar Excel environment.

In addition to easy-to-use data tools, SMM also offers professional price membership services and in-depth market analysis reports. Whether you are a trader who needs real-time price references, an analyst who relies on granular data to build models, or an enterprise manager seeking market insights, you can find the right solution at SMM.

Coffee Break and Networking

With this, the 2026 SMM H1 London Seminar has come to a successful conclusion. SMM sincerely appreciates the strong support from all industry peers and partners.

![Copper Prices Fluctuate at Highs, Shanghai Spot Copper Premiums Pull Back Under Pressure [SMM Shanghai Spot Copper]](https://imgqn.smm.cn/usercenter/KTLHT20251217171714.jpeg)

![Copper Prices Center Shifted Upward, Downstream Buyers Mainly Made Just-in-Time Procurement [SMM North China Spot Copper]](https://imgqn.smm.cn/usercenter/eFYDl20251217171712.jpg)