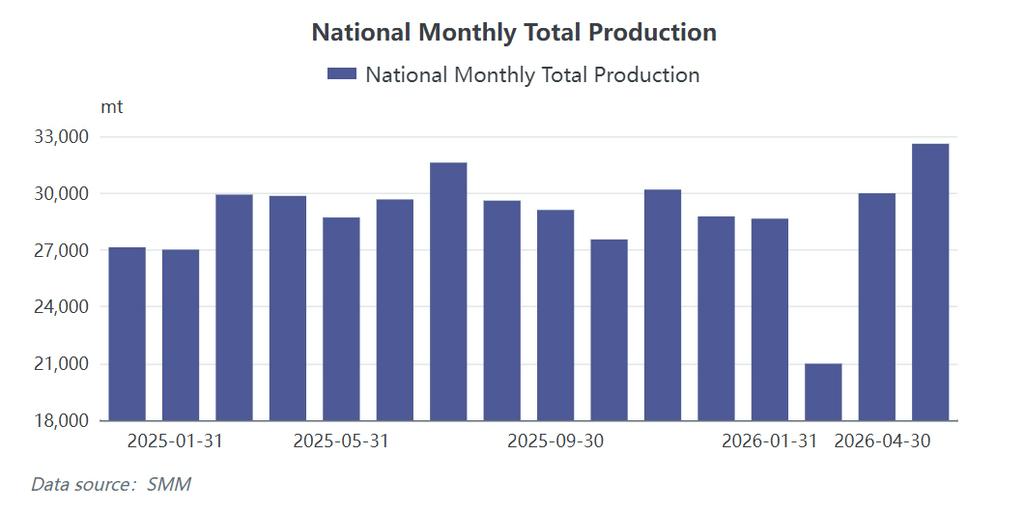

In April 2026, the output of NdFeB blanks reached 32,603 metric tons, representing a significant month-on-month increase of 8.73% and a year-on-year rise of 9%. The industry-wide average operating rate climbed to 76.37%, indicating an accelerated expansion. According to SMM's frontline research, production is expected to further increase to 34,097 tons in May, a month-on-month growth of approximately 5%. If this forecast materializes, it will mark the highest production level since January 2025.

However, beneath the surface of rising output and operating rates, the industry is broadly facing a dilemma of "increasing revenue but not profit." Magnetic material companies report that high raw material costs, coupled with limited acceptance of high prices by downstream end-users, are leading to a cost inversion that is unlikely to improve in the short term, thus hindering profit recovery.

Rising Production: Resonance of Seasonal Demand and Export Pull

This round of production growth is primarily driven by the traditional manufacturing peak season and geopolitical factors.

On one hand, the second quarter is the traditional stocking season for sectors like air conditioners and industrial motors. With the upgrade of domestic energy efficiency standards, the demand for high-performance NdFeB from variable-frequency air conditioners and high-efficiency energy-saving motors has grown steadily, providing stable domestic demand support.

On the other hand, the surge in global energy prices triggered by the Israel-Hamas war has accelerated the substitution of new energy vehicles in Europe and the Middle East. Leveraging supply chain advantages, Chinese magnetic material companies have seen a notable increase in export orders. From January to March 2026, the export volume of rare earth permanent magnets reached 16,000 tons, a 4.8% year-on-year increase, with demand from the new energy vehicle sector being the main driver.

Furthermore, the general export licensing policy, which began in the fourth quarter of 2025, has gradually taken effect in 2026, simplifying export procedures for companies and further facilitating the release of overseas orders.

Profit Pressure: Impeded Price Transmission

Despite strong demand, the profitability of magnetic material companies has not improved in tandem. The core contradiction lies in the difficulty of cost transmission.

On the upstream side, rare earth raw material prices have remained at high levels. In the first quarter of 2026, the average price of PrNd oxide saw a substantial year-on-year increase, and major rare earth groups have consecutively raised concentrate prices, exerting immense cost pressure on magnetic material companies.

On the downstream side, competition is fierce across new energy vehicles, home appliances, and industrial motors, with end-manufacturers universally demanding price reductions from upstream suppliers to share cost pressures. This "double squeeze" of rising upstream prices and downstream price suppression has led many magnetic material companies into a cost inversion dilemma, where product selling prices fail to cover raw material costs, resulting in a phenomenon of "increasing orders but declining profits." Even for companies with rising production, financial expenses (mainly affected by capital tied up in raw material procurement) have also increased significantly year-on-year, further eroding profit margins.

Demand Divergence: Structural Concerns Amidst High Prosperity

From the perspective of downstream demand structure, different application sectors show clear signs of divergence.

New Energy Vehicles (NEVs): As the largest consumption sector for NdFeB, demand exhibits a pattern of "calm domestically, booming for exports." The domestic market penetration rate is already at a high level, and growth is slowing; the export market has become the main engine driving demand.

Energy-Efficient Home Appliances: Driven by energy efficiency policies, demand for NdFeB from variable-frequency air conditioners and washing machines has maintained steady growth. However, this sector is highly price-sensitive, and magnetic material companies have weak pricing power.

Industrial Motors: Benefiting from industrial energy-saving retrofits, the penetration rate of permanent magnet motors continues to rise. However, the market has numerous players and intense price competition, severely compressing profit margins.

Industry Outlook: Technological Cost Reduction as the Key to Breakthrough

In the short term, supported by seasonal demand and export orders, NdFeB production is expected to remain at high levels. However, the cost inversion dilemma is likely to persist, and the industry will generally exhibit the characteristic of "increasing volume but stable profits."

In the long run, the focus of industry competition is shifting from scale expansion to technology and cost control. To cope with cost pressures, advanced technologies capable of reducing heavy rare earth usage, such as Grain Boundary Diffusion (GBD), are being rapidly adopted. Leading companies with technological advantages, high-end capacity deployment, and upstream resource synergy are expected to take the initiative in this round of industry reshuffle, while small and medium-sized enterprises lacking core competitiveness face the risk of elimination.