Strong Cost Support Meets Weak Demand as Overseas Secondary Aluminum Market Divergence Widens【SMM Analysis】

The overseas secondary aluminum market continues to show structural divergence. Scrap aluminum prices remain elevated, providing strong cost support; however, downstream procurement remains cautious with weak transaction follow-through. As a result, demand-side support for prices has marginally weakened, and the market is characterized by firm quotations but subdued trading activity.

1. Price Trends: Marginal Raw Material Pullback, Divergence in Alloy Prices

Last week, overseas secondary aluminum prices remained in a high-level consolidation range. Scrap prices saw a slight pullback, while alloy prices showed regional divergence.

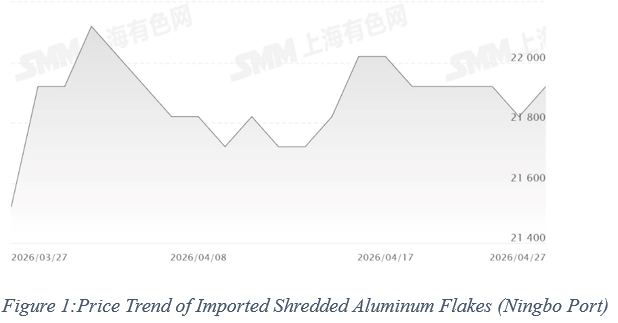

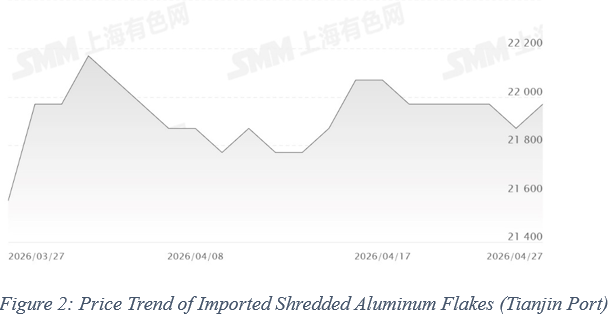

On the scrap side, imported shredded aluminum prices edged lower. Ningbo port prices declined from RMB 21,920/mt to RMB 21,820/mt, while Tianjin port prices dropped from RMB 21,970/mt to RMB 21,870/mt, representing a decrease of around RMB 100/mt. Despite the marginal weakening, prices remain at relatively high levels, continuing to provide effective cost support for ADC12.

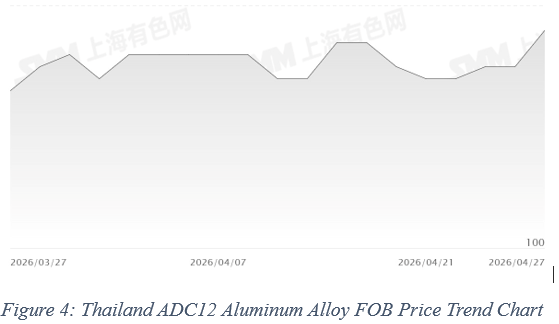

For ADC12 secondary aluminum alloy ingots, the Thai market remained stable last week. Domestic prices were concentrated in the range of THB 106–108/kg, with a weekly average of around THB 107.50/kg. FOB prices were stable within USD 3,310–3,350/mt, averaging approximately USD 3,340/mt.

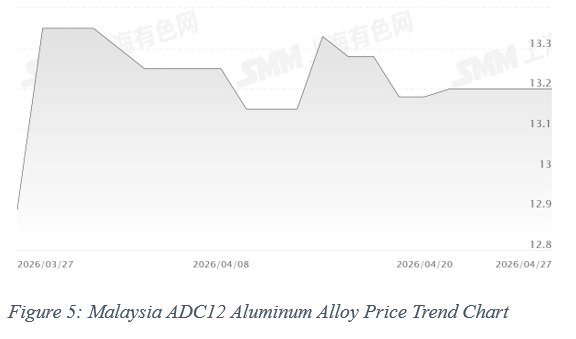

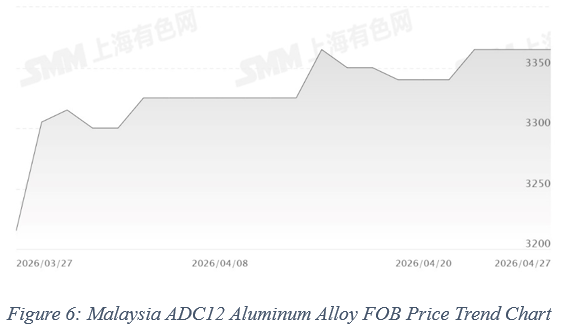

In comparison, the Malaysian market showed relatively stronger performance. Domestic prices edged up from MYR 13.175/kg to MYR 13.20/kg, while FOB prices increased from USD 3,340/mt to USD 3,365/mt, indicating slightly stronger export performance than Thailand.

2. Costs and Demand: Cautious Downstream Procurement, Transactions Under Pressure

From a transaction perspective, the market remained generally weak last week. Downstream buyers showed limited willingness to accept higher prices, with “buying resistance” widely observed.

Although some producers attempted to raise quotations due to elevated costs, actual transactions failed to keep pace. Discounts were observed in some deals, and the gap between bid and offer prices widened. Procurement remained largely demand-driven, with weak restocking momentum, and demand-side support for prices remained limited.

3. Raw Material Side: Tight Supply Persists, Cost Support Remains Strong

On the raw material side, scrap aluminum supply remains tight, particularly for high-grade materials.

According to SMM research, the delivery cycle for imported scrap is currently around three weeks, constraining supply availability. Meanwhile, prices for mainstream scrap categories such as motor casings and UBC remain elevated, keeping cost pressures high for producers.

Some companies have adjusted their raw material mix to offset cost pressures. Overall, the high-cost environment remains unchanged and continues to provide underlying support for alloy prices.

4. Overall Assessment: Persistent Gap Between Quotations and Transactions

Overall, in the Thai market, although elevated scrap costs provided strong bottom support and strengthened sellers’ pricing stance, sluggish demand recovery and cautious procurement behavior from downstream buyers continued to cap price increases.

In contrast, the Malaysian market saw relatively stronger buying interest, which provided some support for prices.

5. Outlook: Range-Bound Market with Limited Upside Momentum

In the short term, the overseas secondary aluminum market is expected to remain range-bound.

ADC12 prices are likely to fluctuate within the range of USD 3,300–3,400/mt. Without a clear improvement in downstream demand, the conversion of higher quotations into actual transactions remains uncertain.

Overall, while strong cost support limits downside risks, slow demand recovery continues to cap upward momentum. Export markets, particularly India, are providing partial support, and the market is expected to remain in a range-bound tug-of-war.