Les nouveaux droits de douane de l’Indonésie sur le nickel et le MACF européen ont fortement augmenté les coûts de l’acier inoxydable à l’étranger, poussant les aciéries asiatiques à relever leurs prix. La demande en aval reste contrastée : le Japon et la Corée du Sud font preuve de résilience, tandis que la région de Taïwan, Chine, subit des pressions. Méfiants face aux hausses rapides des prix, les acheteurs limitent leurs achats aux besoins incompressibles. Le marché restera prudent jusqu’à ce que les détails tarifaires et la demande réelle soient confirmés.

I. Environnement macroéconomique et résonance des politiques

Le marché mondial de l’acier inoxydable traverse actuellement une période de forte volatilité alimentée par les politiques, dans laquelle les conflits géopolitiques et les barrières commerciales ont provoqué un déplacement marqué du centre de coûts des marchés extérieurs. Les pénuries mondiales d’approvisionnement énergétique et la hausse des prix du pétrole déclenchées par les récents conflits géopolitiques ont aggravé les pressions inflationnistes et sur la croissance économique des pays importateurs d’énergie. Afin d’alléger les pressions sur le budget intérieur et de pousser davantage la montée en gamme de la chaîne de valeur des ressources, le président indonésien Prabowo a officiellement approuvé l’imposition de taxes à l’exportation sur le nickel et le charbon. Cet ajustement macroéconomique a fondamentalement ravivé le sentiment haussier au sein de la chaîne d’approvisionnement en matières premières. Parallèlement, le marché européen ressent fortement l’impact des barrières commerciales vertes. Le mécanisme d’ajustement carbone aux frontières (MACF) de l’Union européenne, officiellement entré en vigueur au début de cette année, combiné à des prix locaux de l’énergie exorbitants et à l’envolée des coûts d’approvisionnement en ferrochrome, a entraîné en avril une hausse maximale de 5,4 % en un seul mois de la surcharge d’alliage de l’acier inoxydable au chrome en Europe. Cela signifie que le commerce mondial de l’acier inoxydable passe en profondeur d’une simple concurrence sur les coûts de production à une compétition fondée sur la capacité à franchir des barrières complexes telles que les émissions de carbone.

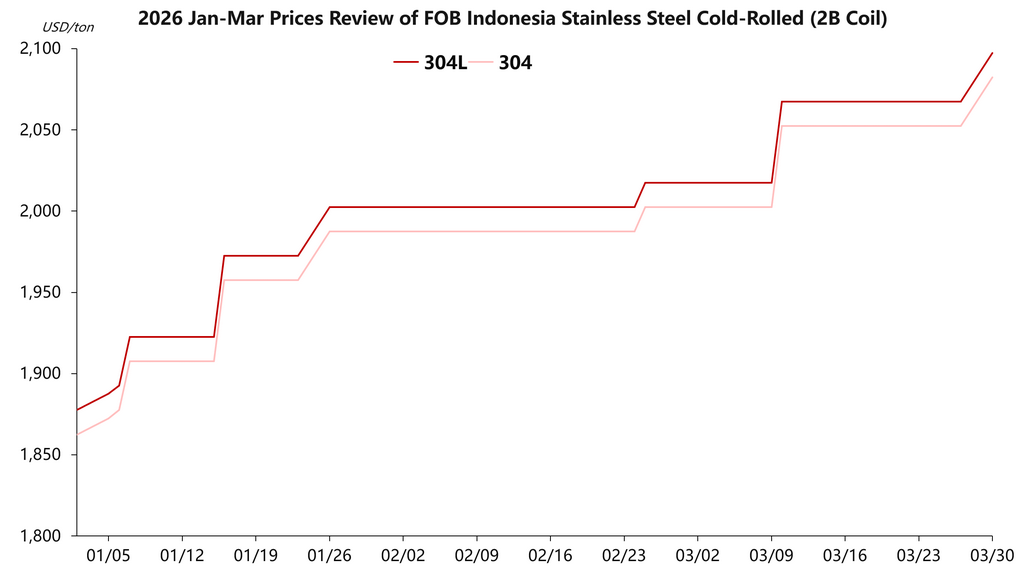

Figure 1 : Évolution des prix FOB de l’acier inoxydable laminé à froid en Indonésie

II. Dynamique de l’offre et de la demande à l’étranger et jeu de marché

Soutenue par de solides facteurs de coûts, l’offre à l’étranger a montré une nette volonté de soutenir les prix. Les cotations FOB à l’exportation de l’acier inoxydable indonésien sont restées fermement à des niveaux élevés, le laminé à froid 304 et le laminé à froid 316L se stabilisant respectivement autour de 2 052,50 $/tonne et 3 852,50 $/tonne. Sous l’effet combiné des perturbations de l’approvisionnement en minerai de nickel à haute teneur en Indonésie et de la hausse des coûts domestiques de l’électricité, les aciéries de plusieurs régions d’Asie ont relevé de manière rapprochée leurs prix de référence. Plusieurs aciéries de la région de Taïwan ont sensiblement augmenté les prix des séries 316 et 304 de 4 000 NTD/tonne et 2 000 NTD/tonne respectivement, tandis que les aciéries du Japon et de la Corée du Sud ont rapidement emboîté le pas avec des ajustements défensifs de prix. Toutefois, derrière cette forte poussée haussière du côté de l’offre, la demande en aval à l’étranger présente une bifurcation structurelle marquée. Le marché japonais a montré une forte résilience, soutenu de manière stable par les industries des semi-conducteurs et de l’automobile, tandis que l’essor de la construction navale en Corée du Sud a directement stimulé l’activité transactionnelle des produits de la série 316. À l’inverse, la région de Taïwan, fortement dépendante des exportations, continue de subir une pression importante sur la prise de commandes. En raison de la rapidité excessive des précédentes hausses des prix de référence, la large base d’acheteurs en aval à l’étranger nourrit actuellement une forte crainte des prix élevés. Le rythme global des achats reste strictement limité aux besoins incompressibles, laissant les échanges de marché profondément enlisé dans un rapport de force bloqué.

III. Perspectives du marché et variables clés

À l’avenir, la logique centrale de fixation des prix sur le marché extérieur de l’acier inoxydable continuera de s’articuler autour du rapport de force entre de puissants facteurs de hausse des coûts et la validation de la demande. À court terme, la mise en œuvre des taux spécifiques des taxes à l’exportation du nickel en Indonésie constituera la principale variable macroéconomique influençant le sentiment du marché, tandis que l’effet de recomposition du MACF européen sur les flux mondiaux de produits semi-finis continuera de se renforcer. Il est attendu qu’il subsiste encore une marge de hausse des prix de référence des aciéries étrangères en avril, mais la capacité de répercuter avec succès ces coûts exorbitants sur l’aval dépendra de manière décisive des actions réelles de reconstitution des stocks des négociants internationaux et des utilisateurs finaux. Tant qu’une demande substantielle n’aura pas été pleinement confirmée et que les ressources actuellement proposées à des prix élevés n’auront pas été effectivement absorbées, le marché extérieur de l’acier inoxydable devrait très probablement conserver une tendance d’oscillation à haut niveau et d’observation prudente.

![[SMM Flash Marché du Nickel] La Banque mondiale estime que les nouvelles capacités nickel de l'Indonésie pourraient être freinées par un approvisionnement en minerai tendu](https://imgqn.smm.cn/usercenter/OjGlE20251217171734.jpg)

![[SMM Flash Marché du Nickel] La Banque mondiale prévoit une hausse de 12 % des prix du nickel en 2026 en raison d'une offre tendue](https://imgqn.smm.cn/usercenter/PFIti20251217171734.jpg)

![[SMM Flash du marché de l'acier inoxydable] Aperam étend sa capacité au Brésil et renforce son intégration en aval avec l'accord Magnetec](https://imgqn.smm.cn/usercenter/fzwTi20251217171733.jpg)