Starting from October 2025, export schedule data from steel mills has been added. The planned production of rebar and wire rod includes exports but excludes steel billet exports.

According to SMM survey data from 56 key steel producers:

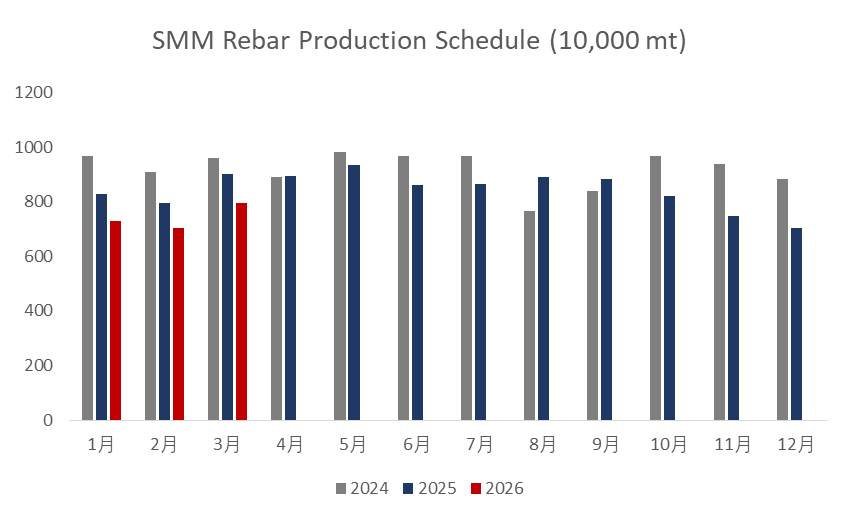

- Planned rebar production in March was 7.9565 million mt, an increase of 923,500 mt from February’s actual production, up 13.13%.

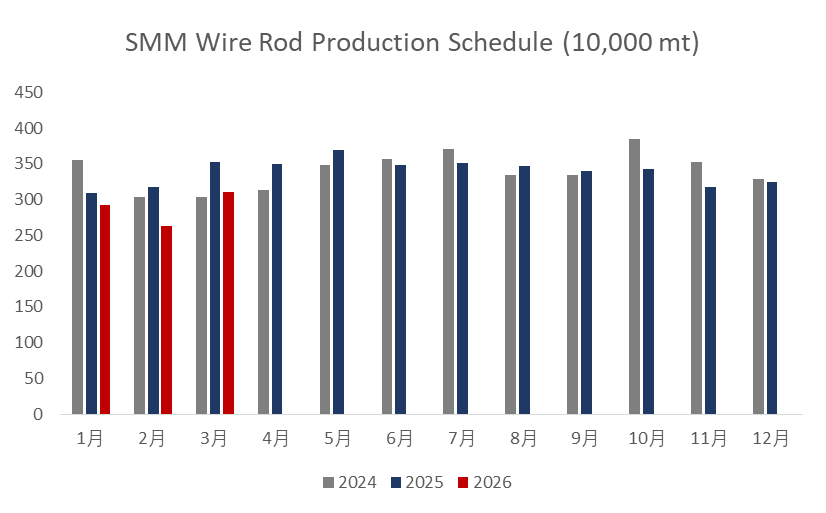

- Planned wire rod production in March was 3.1036 million mt, an increase of 466,300 mt from February’s actual production, up 17.68%.

Chart-1-2: Planned Production of Rebar & Wire Rod at Main Construction Steel Mills (56 mills)

Data source: SMM

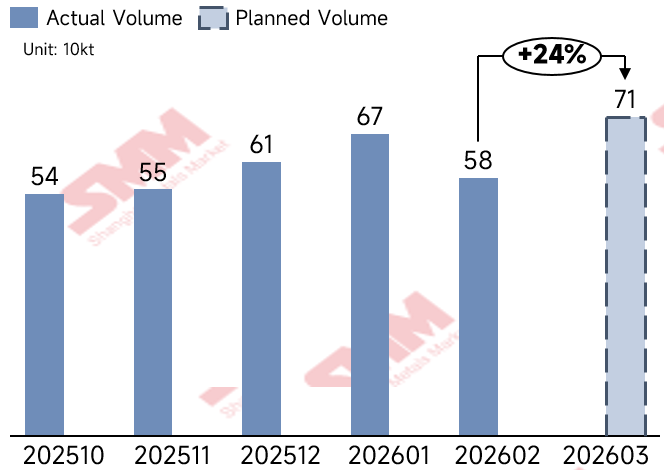

- Export schedule of long products from sample steel mills in March was 712,000 mt, an increase of 137,000 mt MoM; of which the steel billet export schedule was 270,000 mt, down 23,000 mt MoM.

Chart-3: Export Schedule of Long Products from Sample Steel Mills

Data source: SMM

Overall:

In February, national construction steel prices ran in a weak consolidation trend. In early February, amid a macro vacuum period, raw material support weakened; coupled with a deterioration in finished steel fundamentals, prices fluctuated downward. Mid-February coincided with the Chinese New Year, during which market trading stalled. In late February, merchants gradually resumed work, but trading had not fully restarted and was largely sentiment-driven. During this period, adjustments to Shanghai’s home purchase policies slightly lifted prices within a narrow range; however, no other positive news emerged ahead of the Two Sessions, market sentiment fluctuated mildly, and prices continued to consolidate.

Cost side, overall raw material prices in February were relatively firm, but finished steel prices were somewhat weak, further squeezing steel mill profitability. At present, the steel mill profitability rate stands at 35.3%, continuing to decline MoM, and profitability is generally in the (-200-100) range. In March, coke has room for concessions, and steel mill profitability may improve in the short term.

Steel mills that previously underwent maintenance had resumed normal production in March. Although steel mill profitability has not improved, the advantage of product mix has weakened, with some hot metal flowing back to construction materials, leading to a continued increase in daily construction materials output in March. Specifically, in North China, some steel mills adjusted their product mix, with some hot metal flowing back to construction materials, and planned production in March increased more noticeably. In Northwest China, to ensure the marginal benefits of hot metal and the normal release of winter stockpiling volumes, there is no maintenance plan for March, and overall production is expected to increase.

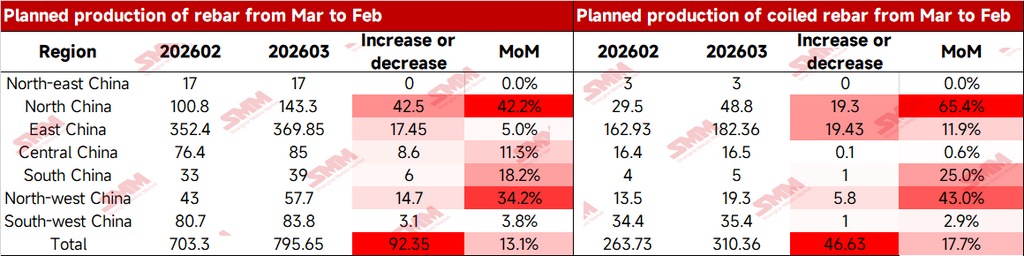

Table 1: Actual Values of Rebar and Coiled Rebar Production Schedule Last Month and Planned Volume This Month

Data Source: SMM

Looking ahead, With the short-term advantage of producing coils and strips not yet significantly greater than that of construction steel, some steel mills adjusted production among product categories. Part of the hot metal flowed back to the construction steel segment; however, considering that some steel mills in east China scheduled rebar and wire rod maintenance in March, the MoM increase in daily average production of construction steel was limited. Multiple EAF steel mills are expected to resume production after the Lantern Festival, and the overall operating rate in March will rebound to normal levels, with production gradually recovering.

Overall, steel mills will have more producible days in March than in February, so an increase in total construction steel production is normal. In addition, after multiple steel mills complete shipments of winter stockpiling resources before March month-end, they will still need to meet regular market demand, and the market will be in the traditional peak-demand season of “Golden March and Silver April.” Construction steel planned total production in April is expected to still have room to increase.

![[SMM Iron & Steel] Raipur Billet Prices Edge Higher](https://imgqn.smm.cn/usercenter/gmcdk20251217171720.jpg)

![In the short term, ferrous metals will remain under pressure [SMM Steel Industry Chain Weekly Report]](https://imgqn.smm.cn/usercenter/YxksS20251217171748.jpg)

![Silicon Metal Futures Fluctuate within a Narrow Range, Spot Market Largely Stable [SMM Silicon Industry Weekly Review]](https://imgqn.smm.cn/usercenter/bkAyC20251217171720.jpg)