Après les vacances du Nouvel An chinois, le marché du cuivre électrolytique est entré dans sa période traditionnelle de validation de la reprise post-vacances. La région du delta du Yangtsé, en tant que cœur national de la transformation et de la consommation du cuivre, sert de baromètre pour évaluer la dynamique de l'offre et de la demande à travers les taux d'activité et le rythme d'approvisionnement en matières premières de ses principales entreprises. Notre enquête indique que la région est actuellement caractérisée par un « accumulation de stocks excessivement élevée, une divergence des taux de reprise et un sentiment d'approvisionnement se redressant prudemment », conduisant à une révision à la baisse des attentes du marché pour le début de la saison haute en mars.

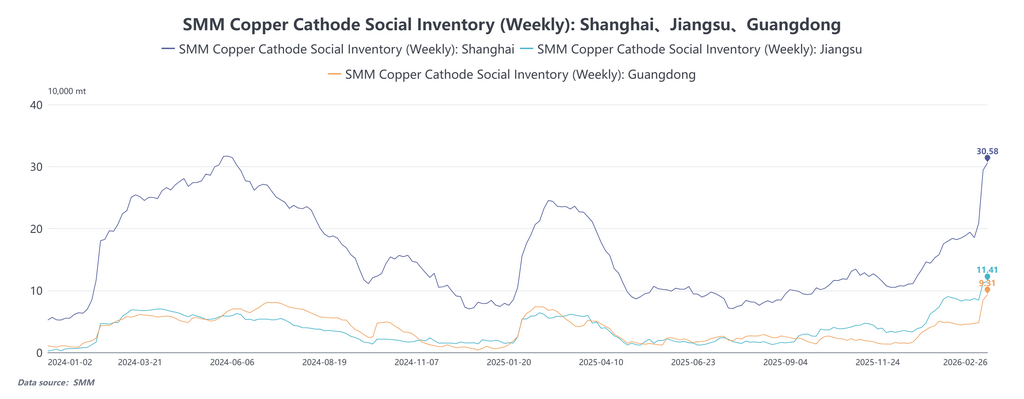

Selon une recherche de SMM, au 26 février 2026, les stocks sociaux de cuivre électrolytique s'élevaient à 531 700 tonnes métriques, soit une augmentation de 178 100 tonnes par rapport au 12 février. Ce rythme d'accumulation des stocks dépasse significativement les niveaux observés les années précédentes. La région du delta du Yangtsé a contribué à la majeure partie de cette augmentation : les stocks à Shanghai sont passés à 305 800 tonnes, tandis que la province du Jiangsu a atteint 93 100 tonnes, en hausse de 97 500 tonnes et 45 200 tonnes respectivement par rapport au 12 février. Cette accumulation de stocks est qualifiée de « livraison passive dans les entrepôts ». Le premier jour de bourse après les vacances (25 février) coïncidant avec le dernier jour de négociation du contrat SHFE 2602, les fonderies ont concentré leurs marchandises livrables dans les entrepôts désignés par la bourse juste avant les vacances. Cela a entraîné une augmentation de 80 400 tonnes des warrants cuivre du SHFE, portant le total à 277 100 tonnes, une partie étant temporairement bloquée sous forme de warrants. Parallèlement, avec le rétrécissement des pertes à l'importation et l'apparition d'une fenêtre de profit avant les vacances, les arrivages de cuivre importé en mars devraient augmenter, exerçant une double pression sur les stocks sociaux nationaux, à la fois de la production domestique et de l'offre importée.

Sur la base des retours opérationnels des entreprises, les secteurs avals de transformation du delta du Yangtsé présentent des dynamiques contrastées significatives :

Le secteur des matériaux pour batteries affiche des performances robustes. Les producteurs de feuilles de cuivre ont soit eu de courts arrêts de production, soit fonctionné en continu pendant les vacances. Les fabricants de batteries en aval fonctionnent à des taux d'utilisation élevés, certains rapportant que leurs plannings de production de mars présentent déjà des caractéristiques de saison haute. Ceci soutient une demande rigide pour l'achat de cuivre électrolytique.

En revanche, la reprise des activités dans les secteurs traditionnels du câble et de la transformation du cuivre est lente. Les performances dans les segments traditionnels de consommation de cuivre comme les fils et câbles, les barres de cuivre et les tubes de cuivre sont relativement faibles. La première semaine après les vacances, les principales entreprises de câbles ont connu une baisse des nouvelles commandes. Outre les prix élevés du cuivre qui freinent l'acceptation en aval, le fait que les projets des utilisateurs finaux n'aient pas encore pleinement démarré est une contrainte majeure. Selon les retours des entreprises, les projets de construction et d'infrastructure reprennent généralement progressivement après la Fête des Lanternes (qui a lieu après les vacances standard), et le marché connaît actuellement une accalmie pour les nouvelles commandes. Les transformateurs de barres de cuivre ont généralement un stock élevé de produits finis, et certaines commandes d'avant les vacances sont encore en attente de livraison. Par conséquent, leurs achats de cuivre électrolytique se concentrent principalement sur la consommation des stocks existants et sur des achats spot ad hoc basés sur les besoins immédiats, montrant une faible volonté de constituer des stocks de matières premières.

Dans l'ensemble, la consommation en aval dans la région présente actuellement un schéma de demande rigide du secteur des batteries contre une demande en attente du secteur des câbles. La transmission de la consommation réelle des utilisateurs finaux à l'étape des achats de cuivre électrolytique demandera encore du temps.

Selon les informations obtenues par SMM via la communication avec les entreprises :

Entreprise 1 : La reprise normale des activités a eu lieu le 6ème jour du premier mois lunaire. L'industrie des batteries en aval fonctionne à un taux d'utilisation élevé ; la production actuelle de feuilles de cuivre est passée de 20 % à environ 50 % par rapport aux niveaux précédents. Cependant, le secteur des fils et câbles a enregistré relativement peu de nouvelles commandes récemment. Les principales raisons sont la persistance de prix élevés du cuivre et, comme les années précédentes, les projets des utilisateurs finaux ne démarrent généralement pleinement qu'après la Fête des Lanternes, entraînant un décalage temporaire dans la transmission de la demande.

Entreprise 2 : L'entreprise a atteint sa pleine capacité de production immédiatement après la reprise du travail le 6ème jour du premier mois lunaire, nécessitant environ 1 000 tonnes de cuivre électrolytique par jour. Le stock de matières premières est maintenu à un niveau raisonnable, adoptant une stratégie d'achat prudente d'achats spot quotidiens. Cependant, le stock de produits finis est plus élevé qu'avant les vacances, avec certaines commandes d'avant les vacances encore en attente de livraison. En ce qui concerne les commandes en aval, les retraits pré-fêtes étaient relativement concentrés, tandis que la performance des nouvelles commandes après les fêtes est faible, car certains clients en aval n’ont pas encore repris leurs activités.

Entreprise 3 : Les ateliers de production ont fonctionné en continu pendant le Nouvel An chinois. Récemment, la production est restée stable, les commandes des clients clés se maintenant fermement. Les stocks de matières premières sont maintenus à un faible niveau, et les achats de cuivre électrolytique sont effectués en fonction du volume des commandes. Cependant, le volume des achats au comptant récents a diminué par rapport à la période précédente.

Entreprise 4 : Récemment, il y a eu une baisse des nouvelles commandes en aval, entraînant des transactions de marché languissantes. La pression des stocks de produits finis n’est pas significative, mais certaines commandes pré-fêtes sont encore en attente de livraison. Les stocks de matières premières sont maintenus dans une fourchette normale et gérable.

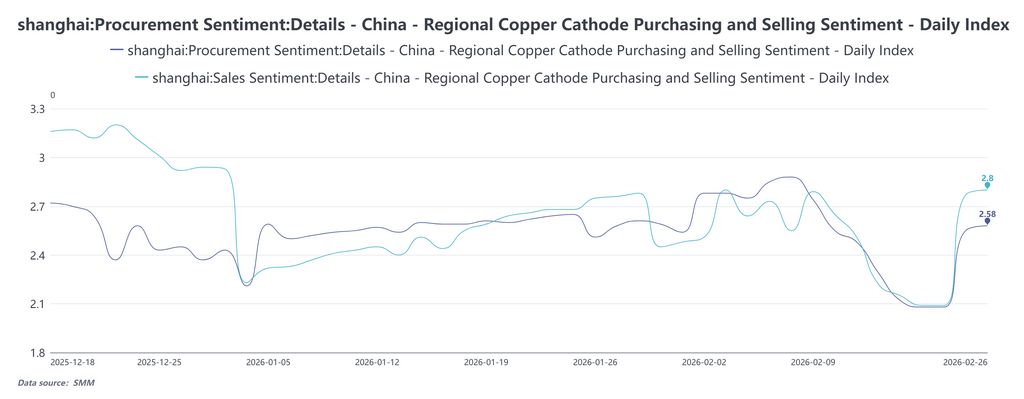

Le 24 février, l’indice de sentiment des achats a enregistré 2,08, restant dans une fourchette faible, indiquant un faible enthousiasme des entreprises en aval pour les demandes de marché lors de la première semaine après les fêtes. Par la suite, il s’est redressé jour après jour pour atteindre 2,58 le 26 février. Sur la même période, l’indice de sentiment des expéditions est passé de 2,09 le 24 février à 2,80 le 26 février, affichant une tendance à la hausse continue et se maintenant systématiquement au-dessus de l’indice de sentiment des achats.Les données historiques peuvent être consultées dans la base de données. Cela reflète qu’avec la progression de la reprise du travail, une certaine demande rigide a commencé à émerger, certaines entreprises en aval entrant sur le marché pour des demandes. Cependant, les niveaux absolus restent bas, indiquant une acceptation limitée des prix actuels du cuivre par les utilisateurs en aval. Leur stratégie de réapprovisionnement reste principalement axée sur des « achats au coup par coup ». Les détenteurs, sous la pression de stocks élevés, manifestent une forte volonté de liquidation, tandis que les transactions du marché circulent principalement dans la sphère commerciale, la véritable absorption en aval n’ayant pas encore significativement repris.

À l’avenir, l’accumulation inattendue de stocks a déjà déclenché une correction du marché par rapport aux attentes antérieures de l’offre et de la demande. À court terme, les stocks sociaux dans la région du delta du Yangts Jiang font toujours face à des pressions de deux côtés : premièrement, l’arrivée de ressources de cuivre importées, et deuxièmement, le besoin de temps pour digérer les stocks élevés de produits finis en aval. Les canaux d'écoulement des stocks sont également obstrués, les stocks du LME continuant d'augmenter et maintenant une structure de Contango, rendant difficile l'absorption du surplus domestique. Un facteur positif du côté de l'offre réside dans la fenêtre de maintenance concentrée des fonderies nationales entre mars et mai durant le premier semestre, avec des impacts substantiels attendus à partir d'avril. Si le soutien de la demande se matérialise d'ici là, un cycle de réduction des stocks pourrait potentiellement commencer entre fin mars et avril. Cependant, en raison du niveau de stocks exceptionnellement élevé après les congés, même l'entrée dans une phase de destocking est peu susceptible de reproduire la structure de BACK élevée et les primes importantes observées durant les mêmes périodes des années précédentes. Globalement, la reprise post-congés dans la région du delta du Yangtsé se caractérise par des niveaux de stocks élevés, des achats prudents et des commandes en attente. Le marché attend désormais le retour substantiel des commandes des utilisateurs finaux après la Fête des Lanternes. La logique de valorisation des prix à court terme pourrait passer de la validation du « déstockage attendu » au « déstockage réel ».

![[SMM Sulfur Flash] Les transactions au comptant de soufre chutent, les prix des raffineries du Shandong reculent](https://imgqn.smm.cn/usercenter/HhNHP20251217171708.jpg)

![Volonté de réapprovisionnement avant les vacances peu soutenue, échanges au comptant modérés [SMM cuivre au comptant de Chine du Sud]](https://imgqn.smm.cn/usercenter/KtfdC20251217171713.jpeg)

![Les livraisons contractuelles à long terme prédominent, l'activité du marché au comptant est atone [SMM North China Spot Copper]](https://imgqn.smm.cn/usercenter/XTMPt20251217171713.jpeg)