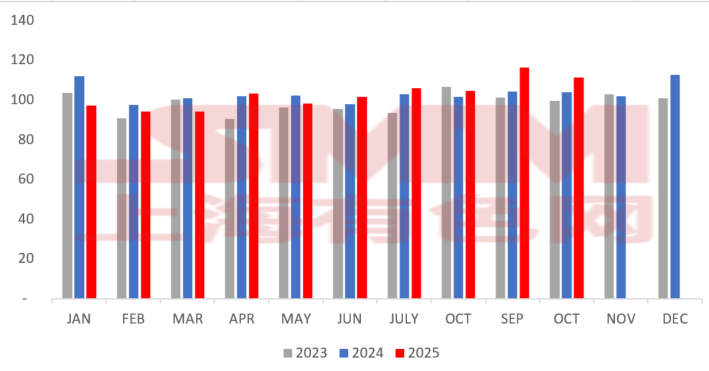

In October, China imported 111.309 million tonnes of iron ore and its concentrate, down 5.017 million tonnes from the previous month, down 4.31% month-on-month, and up 7.19% year-on-year. From January to October, the cumulative import of iron ore and its concentrate was 1028.886 million tonnes, up 0.7% year-on-year.

The import volume of iron ore in October declined slightly, mainly because some steel mills and traders declared and prepared goods in advance before the National Day holiday, and some goods had been counted in September. Meanwhile, steel mills in Hebei province were affected by environmental protection policies in late October, with more maintenance and furnace shutdown, which led to a decline in imports in October.

Looking ahead to November, as the northern region enters winter, the demand for steel in the construction industry has weakened, and the poor shipment of steel mills has led to increased inventory pressure. In addition, the northern region has entered the heating season, and environmental protection and production restrictions are frequent, which is expected to lead to consistent blast furnace production. At the same time, the further rise in coke prices has led to increased losses for steel mills, and some steel mills may have further production reduction plans. Taking into account the comprehensive consideration, it is expected that the overall demand for iron ore will further weaken in November, and the import volume may also decline accordingly.

China Iron Ore Import in October 2025:

![Forecast for Next Week: Ferrous Metals Expected to Fluctuate at Highs in the Short Term [SMM Steel Industry Chain Weekly Report]](https://imgqn.smm.cn/usercenter/VYrIs20251217171747.jpg)

![[SMM Zhangjiagang HRC Inventory] Zhangjiagang Inventory Declined WoW This Week](https://imgqn.smm.cn/usercenter/SEwWP20251217171716.jpg)