SMM June 3 News:

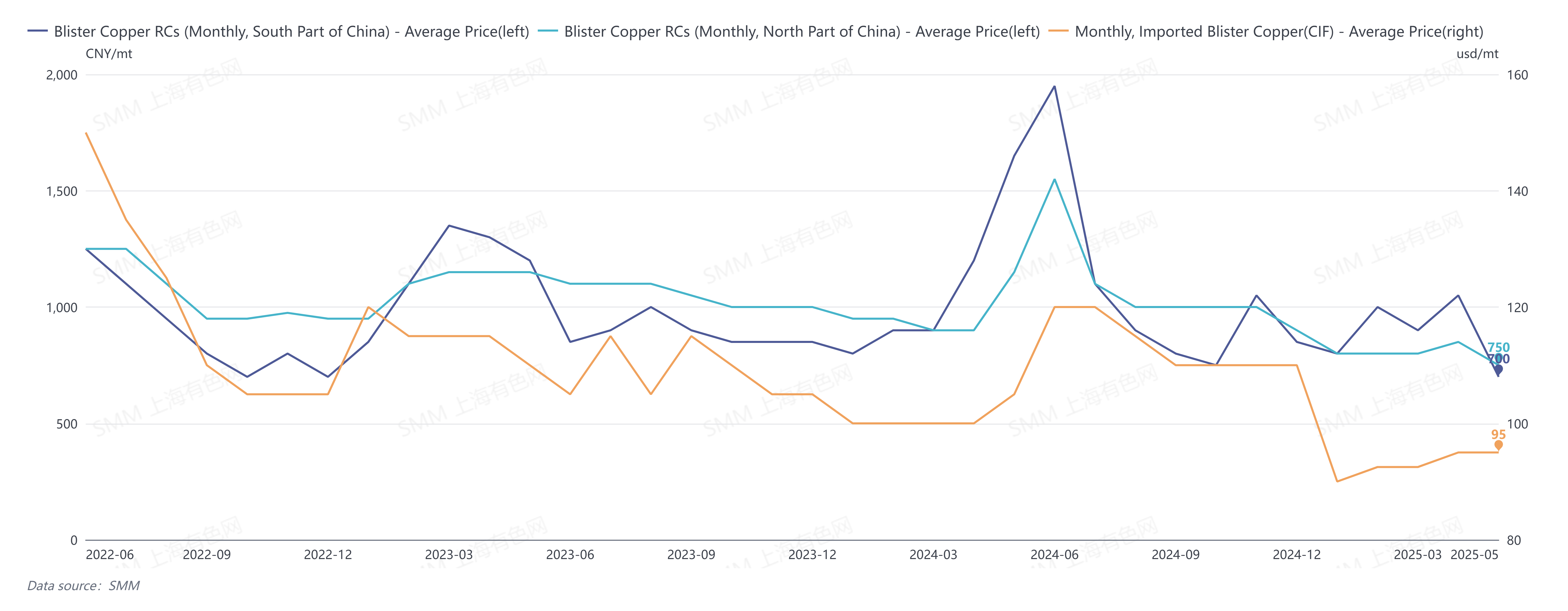

In May 2025, blister copper RCs in south China were quoted at 600-800 yuan/mt, with an average of 700 yuan/mt, down 350 yuan/mt MoM. Blister copper RCs in north China were quoted at 650-850 yuan/mt, with an average of 750 yuan/mt, down 100 yuan/mt MoM. CIF import blister copper RCs were quoted at 90-100 US dollars/mt, with an average of 95 US dollars/mt, unchanged MoM.

In May, due to reduced copper scrap imports and tight domestic copper scrap supply, the production of copper anode made from scrap was constrained. Meanwhile, anode copper suppliers in the northern market faced rising costs as copper concentrate TC continued to deteriorate, leading to a decline in overall domestic anode copper supply. However, despite a significant MoM rebound in anode copper imports in April, which provided some supply relief, the increase was relatively limited. On the demand side, after a sharp drop in copper prices in April, market supply tightened, reducing smelters' anode copper inventories. As a result, restocking demand rose in May, causing a sharp decline in domestic blister copper RCs that month.

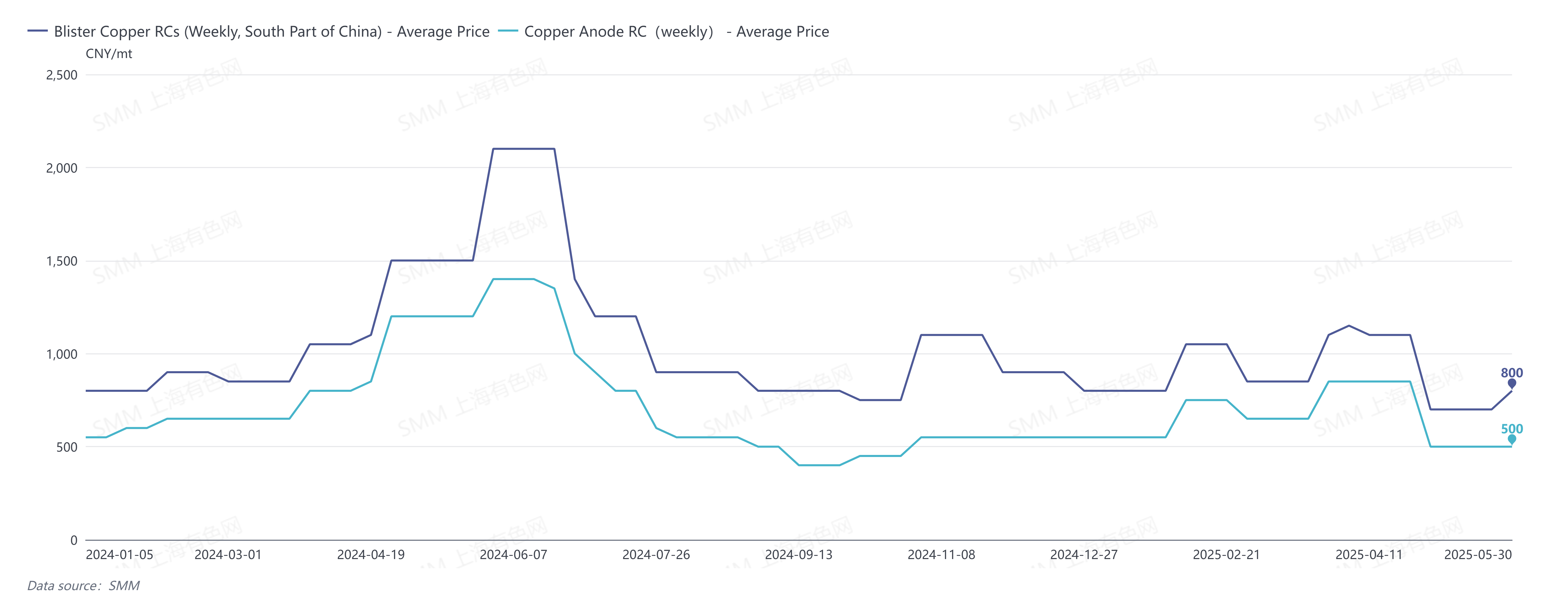

On May 30, SMM's weekly blister copper RCs in south China were quoted at 700-900 yuan/mt, with an average of 800 yuan/mt, up 100 yuan/mt MoM. Weekly blister copper RCs in north China were quoted at 650-850 yuan/mt, with an average of 750 yuan/mt, unchanged MoM. Weekly CIF import blister copper RCs were quoted at 90-100 US dollars/mt, with an average of 95 US dollars/mt, unchanged MoM. Copper anode RCs were quoted at 450-550 yuan/mt, with an average of 500 yuan/mt, unchanged MoM.

Looking ahead to June, copper scrap imports are expected to remain limited, and the supply of secondary copper raw materials is unlikely to increase significantly. However, influenced by consumption and profitability, some secondary copper rod capacity may shift to anode copper production, potentially leading to a slight increase in domestic anode copper supply. In terms of imports, according to enterprise feedback, port arrivals of imported anode copper are expected to be concentrated in Q2. On the demand side, as the mid-year period approaches, some smelters need to clear inventory. Overall, market supply is expected to increase slightly while demand declines slightly, but the overall tight market dynamics are unlikely to reverse, with limited upside potential for RCs.