On May 28, 2025, the US Court of International Trade in New York ruled that the executive order issued by the US government to impose tariff hikes on multiple countries under the International Emergency Economic Powers Act was an ultra vires act and illegal, prohibiting the implementation of the relevant executive order. The reason was that the President did not have the authority to impose comprehensive tariffs on nearly all trading partners, and that Congress's delegation of "unrestricted tariff authority" to the President violated the Constitution. Additionally, Congress had set limits in the International Emergency Economic Powers Act to restrict the President's power to impose tariffs. However, Trump indicated that he would still appeal the ruling, so there remains significant uncertainty regarding changes to US tariffs on China.

Nevertheless, according to the ESS tariff measures currently being implemented, there are three periods: May 14, 2025, August 13, 2025, and January 1, 2026, with tariffs of 40.9%, 64.9%, and 82.4%, respectively.

This article is the first in the series, aiming to analyze the impact of price changes on ESS battery cells produced in China through direct exports, re-exports via Malaysia, and the potential local production of LFP ESS battery cells in the US between May 14 and August 13. Some data values are more theoretical, so the results may appear high. The author will explain in detail the reasons for each data value to enable readers to replace the relevant data themselves and obtain more targeted conclusions. Subsequent articles (II) and (III) will analyze the price impacts caused by different tariffs in the subsequent two periods.

Taking domestically produced 280Ah LFP ESS battery cells as an example:

(1) Direct exports from China to the US: The data sources and changes for each link are shown in the table below.

(2) Re-exports from China to the US via Malaysia: The data sources and changes for each link are shown in the table below.

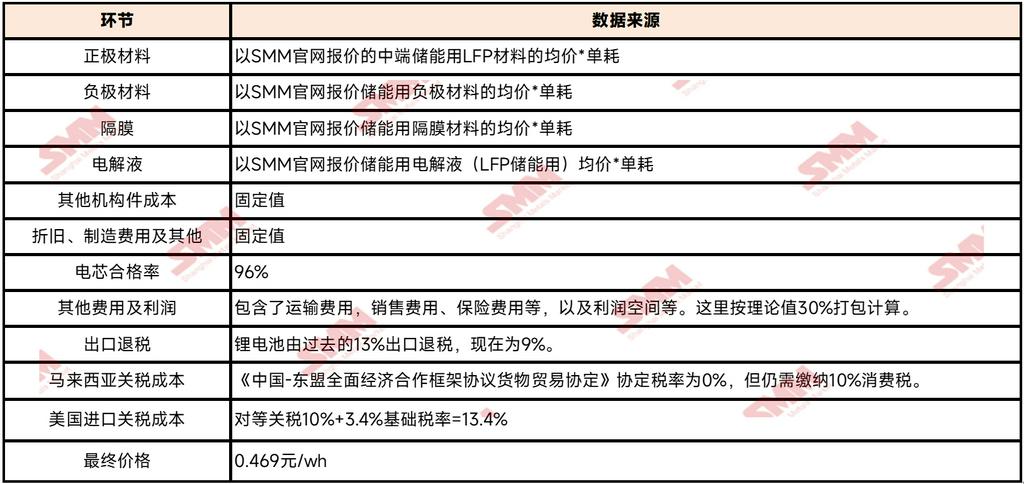

(3) US imports of raw materials for local production of battery cells: The data sources and changes for each link are shown in the table below.

(3) US imports of raw materials for local production of battery cells: The data sources and changes for each link are shown in the table below.

Note: Given China's extremely high global market share in the LFP and artificial graphite anode sectors, it is considered unlikely that the US could bypass China to directly import relevant raw materials. Therefore, corresponding tariff changes will also apply to the materials mentioned below.

Based on the above calculations, at the current stage, with the price of battery cells directly exported from China at 0.52 yuan/Wh, re-exporting via Malaysia offers a 9.8% price advantage, while the cost of directly producing ESS battery cells in the US remains 8.6% higher than in China.

The above content is summarized as follows:

Note: Some of the calculated data were obtained by the author through discussions and processing in the market, while more data were sourced from the average prices at various price points on the SMM official website. In addition, in the current actual operation, the increased costs resulting from the US tariffs on China are mainly borne by overseas customers. Therefore, the calculation results in this article may be higher than the actual transaction prices. Any inappropriate content is open to criticism and correction.

SMM New Energy Industry Research Department

Wang Cong 021-51666838

Ma Rui 021-51595780

Feng Disheng 021-51666714

Lv Yanlin 021-20707875

Zhou Zhicheng 021-51666711

Zhang Haohan 021-51666752

Wang Zihan 021-51666914

Wang Jie 021-51595902

Xu Yang 021-51666760

Chen Bolin 021-51666836

![[SMM Analysis] Korea’s Automotive Industry: 2030 Competitiveness Depends on EV Transition Execution](https://imgqn.smm.cn/usercenter/JKfXw20251217171731.jpg)

![[MinRes Announces Restart of Bald Hill Lithium Mine]](https://imgqn.smm.cn/usercenter/wZUBk20251217171729.jpg)