SMM, 20 mai :

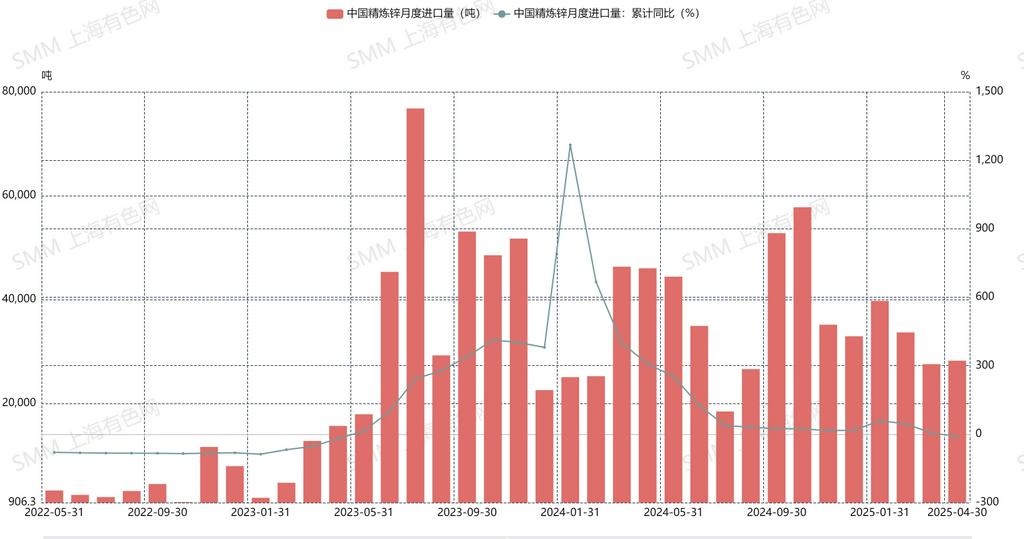

Selon les dernières données douanières, les importations chinoises de zinc raffiné ont atteint 28 200 tonnes métalliques (tm) en avril 2025, en hausse de 600 tm en glissement mensuel (gm) ou de 2,4 % gm, mais en baisse de 38,66 % en glissement annuel (ga). Les importations cumulées de zinc raffiné de janvier à avril se sont élevées à 129 200 tm, soit une baisse de 9,44 % en ga. En avril, la Chine a exporté 2 500 tm de zinc raffiné, ce qui a donné lieu à des importations nettes de 25 700 tm de zinc raffiné pour le mois.

Les trois premiers pays pour les importations de zinc raffiné en avril étaient le Kazakhstan (20 700 tm, soit 73,35 %), l'Australie (4 800 tm, soit 16,9 %) et l'Inde (1 900 tm, soit 6,78 %). Du point de vue des données par pays, les importations de lingots de zinc en provenance du Kazakhstan ont fortement augmenté. En termes de mode de commerce, le commerce ordinaire représentait environ 87 % des importations. Cela était principalement dû à l'ouverture intermittente de la fenêtre d'importation en avril, qui a fourni des opportunités pour les importations de commandes au comptant, maintenant les importations de lingots de zinc à un niveau élevé.

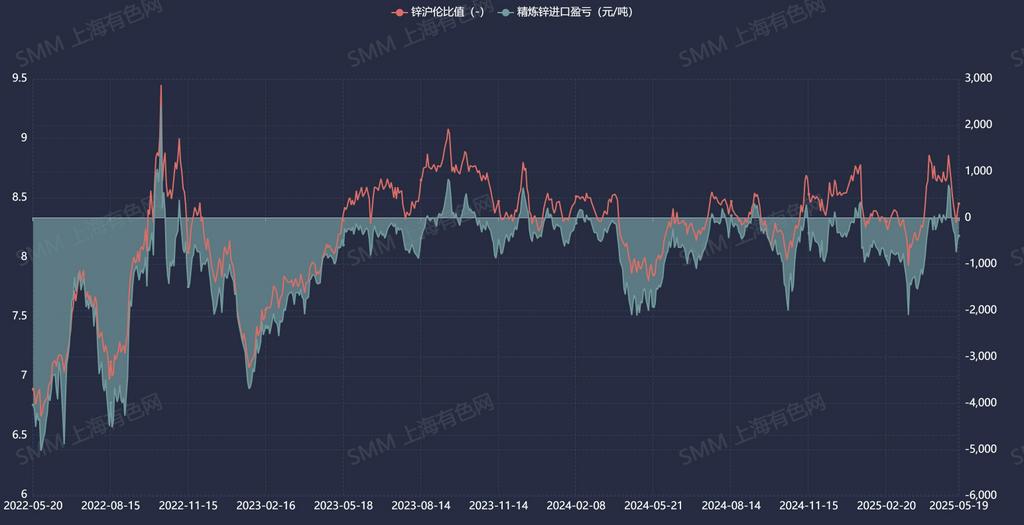

Entrant dans le mois de mai, avec l'atténuation du différend commercial sino-américain sur le plan macroéconomique, le moral du marché s'est quelque peu amélioré. Cependant, les inquiétudes concernant la faiblesse des données économiques américaines ont contrebalancé l'optimisme antérieur lié aux réductions tarifaires, augmentant les craintes d'une récession économique aux États-Unis et affaiblissant le moral à l'étranger. Du côté des fondamentaux, en raison des attentes des fonderies concernant l'augmentation de la production à l'avenir et de la demande d'achat et de stockage qui en résulte, les TCs des minerais nationaux ont eu du mal à augmenter en mai. Cependant, avec les attentes d'une augmentation des importations de minerais, les TCs d'importation ont quelque peu augmenté, maintenant un niveau globalement élevé. Dans le contexte de la maintenance des fonderies en Chine en mai, les arrivées de marchandises au comptant ont été inférieures aux attentes, maintenant les stocks sociaux à un niveau bas et fournissant un soutien de base aux prix du zinc. Couplé à l'atténuation actuelle des différends commerciaux et aux attentes d'une ruée vers les exportations de certains secteurs en aval, avec un marché intérieur surperformant le marché extérieur, le ratio des prix du zinc SHFE/LME a augmenté, ouvrant la fenêtre d'importation de zinc raffiné. Par conséquent, les lingots de zinc importés de l'étranger ont afflué et les importations devraient augmenter à environ 35 000 tm.

》Cliquez pour consulter la base de données de la chaîne industrielle des métaux SMM