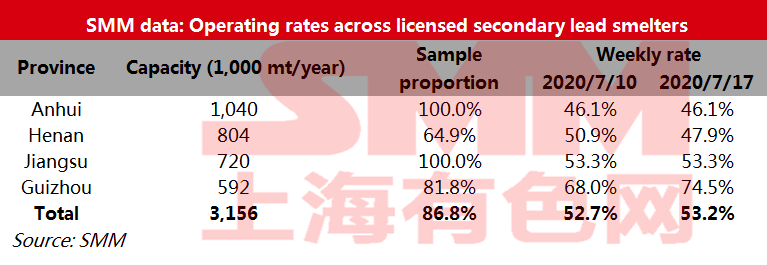

SHANGHAI, Jul 17 (SMM) – Operating rates across licensed smelters of secondary lead in Jiangsu, Anhui, Henan and Guizhou averaged 53.2% in the week ended July 17, up 0.5 percentage point from the previous week, showed an SMM survey.

A rise of 6.5 percentage points in the operating rate in Guizhou, to 74.5%, accounted for the overall increase, as Guizhou Sanhe and Cenxiang smelters returned to normal production after maintenance.

The average rates in Anhui and Jiangsu held largely unchanged from a week ago, at 46.1% and 53.3% respectively, as a continued tight supply of battery scrap and production technology constraints kept a lid on production. Smelters struggled to maintain normal operations.

The average operating rate in Henan stood at 47.9%, down 3 percentage points from a week ago, as Henan Jinli scaled back production to 80% of last week’s level amid maintenance this week.

SMM expects the operating rates across Chinese secondary lead smelters to decline next week as a slump in lead prices and high prices of battery scrap have significantly squeezed their profits. Most smelters tended to hold cargos back from the market and their production enthusiasm may be dampened next week.

![SHFE lead 2607 traded above the daily average line intraday, recording a three-day winning streak [Lead Brief Review]](https://imgqn.smm.cn/usercenter/yqTpQ20251217171721.jpeg)

![[SMM Sulfur Flash] Spot Sulfur Transactions Slide, Shandong Refinery Quotes Decline](https://imgqn.smm.cn/usercenter/HhNHP20251217171708.jpg)