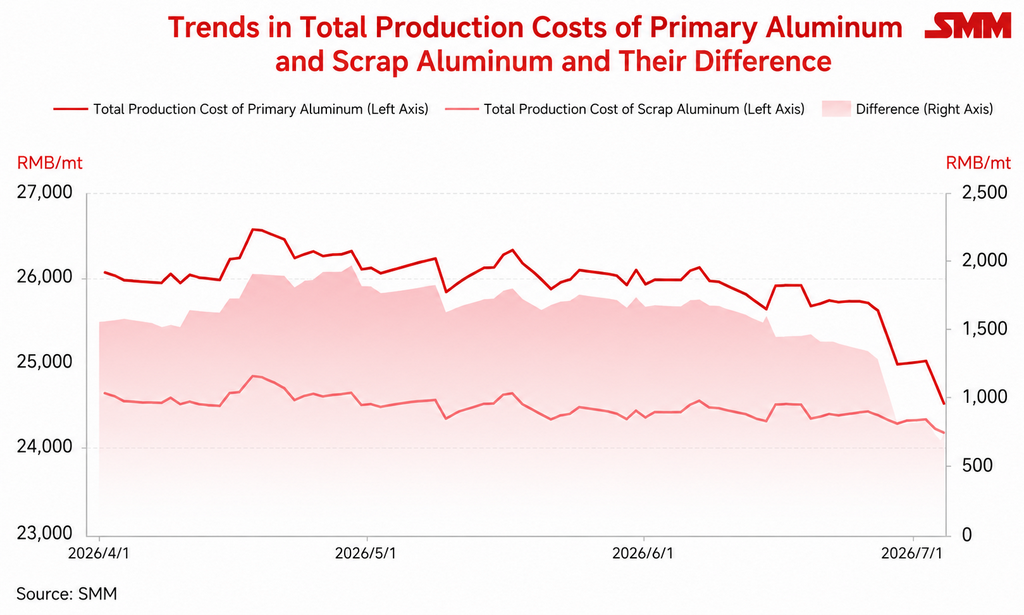

Since June, aluminum prices have remained under downward pressure, with the decline accelerating in the second half of the month. As of July 2, the SMM A00 aluminum price had fallen by RMB 1,650/mt from the beginning of June.

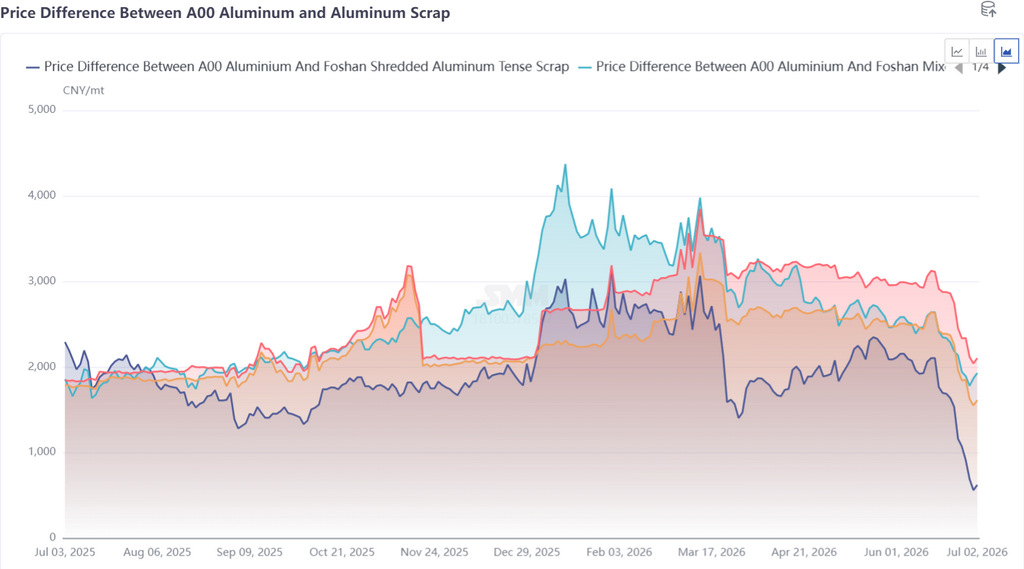

Scrap aluminum prices, however, have shown much stronger resilience. Tightened tax compliance, reduced import inflows caused by unfavorable domestic-overseas price spreads, limited availability of compliant scrap, and widespread seller reluctance have all constrained scrap supply. As a result, the primary-to-scrap aluminum spread has narrowed rapidly to one of its lowest levels in recent years.

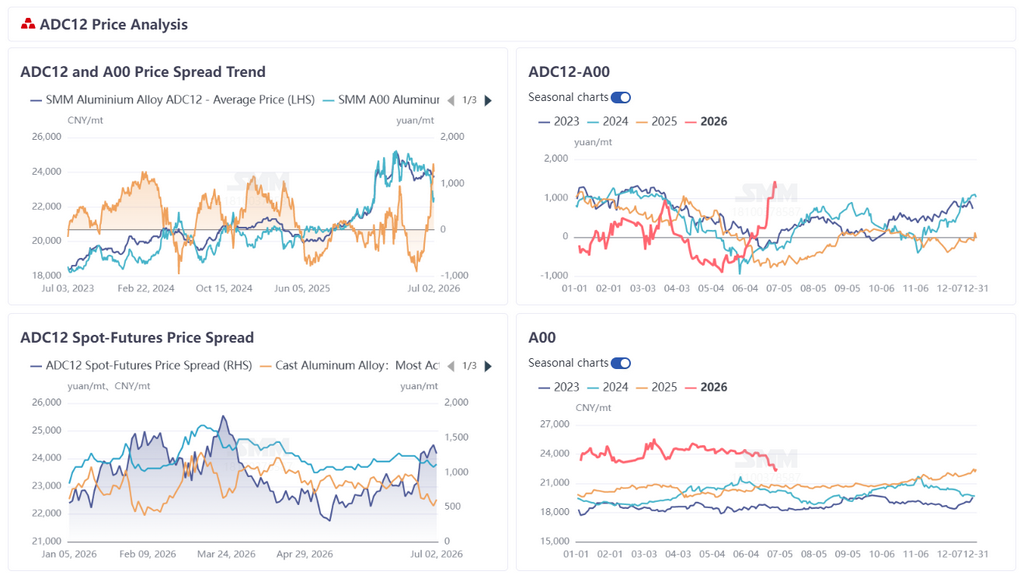

Supported by elevated scrap costs and tightening supply, ADC12 prices have declined far less than primary aluminum prices, pushing the ADC12-A00 price premium above RMB 1,000/mt, the highest level for the same period on record.

Against this backdrop, market discussions over whether A00 primary aluminum could replace scrap aluminum in ADC12 production have intensified. To better understand current market practices, SMM recently conducted a survey among a number of secondary aluminum producers.

Some Producers Have Begun Evaluating Substitution, but Mainly for Supply Security

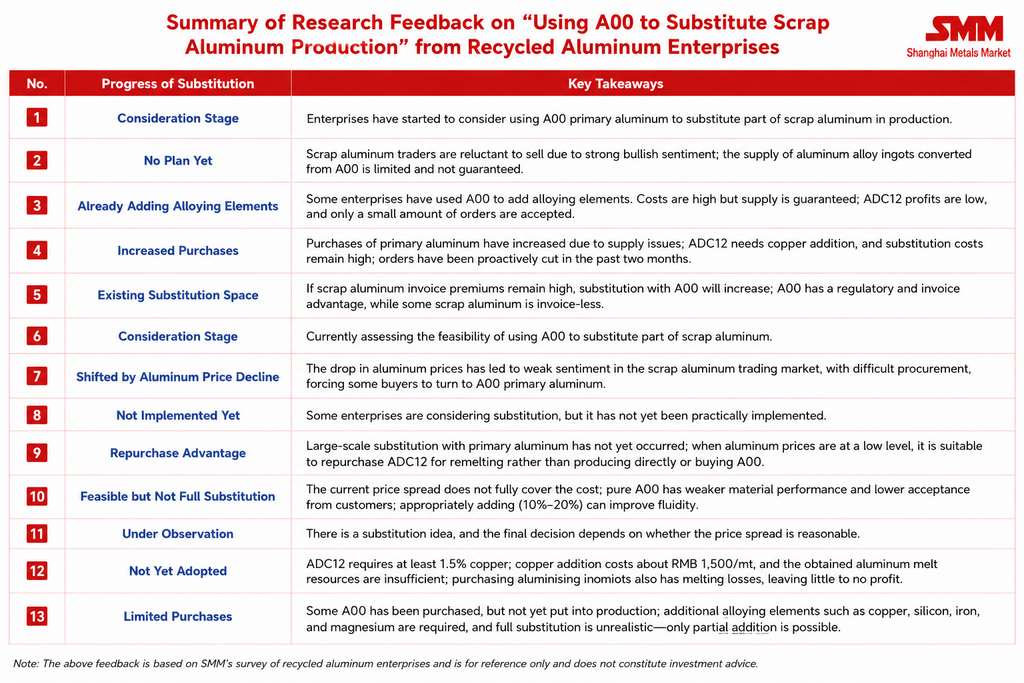

The survey indicates that several producers have started reassessing the feasibility of using primary aluminum in place of scrap. Many companies are recalculating production costs or considering increasing the proportion of A00 in their charge mix, while a few have already purchased small quantities of primary aluminum for potential future use.

Companies that have already increased primary aluminum purchases emphasized that the decision is driven primarily by supply security rather than cost considerations. With scrap traders increasingly withholding material amid falling aluminum prices, spot scrap availability has tightened significantly, forcing some producers to purchase A00 simply to maintain production and fulfill customer orders.

Although the recent decline in primary aluminum prices has partially eased cost pressure, overall production costs remain relatively high. In other words, current substitution is largely a "supply-driven substitution" rather than a cost-driven one.

Several producers also noted that A00 offers a significant compliance advantage, as purchases come with fully compliant invoices, making tax considerations another important driver behind the recent increase in primary aluminum procurement.

Many Producers Remain on the Sidelines

Despite growing interest, many producers remain cautious and have yet to put substitution plans into practice.

Some respondents pointed out that with ADC12 prices currently at relatively low levels, purchasing spot ADC12 ingots is more economical than buying A00 and producing the alloy in-house. This has also accelerated inventory drawdowns in the domestic secondary aluminum alloy market.

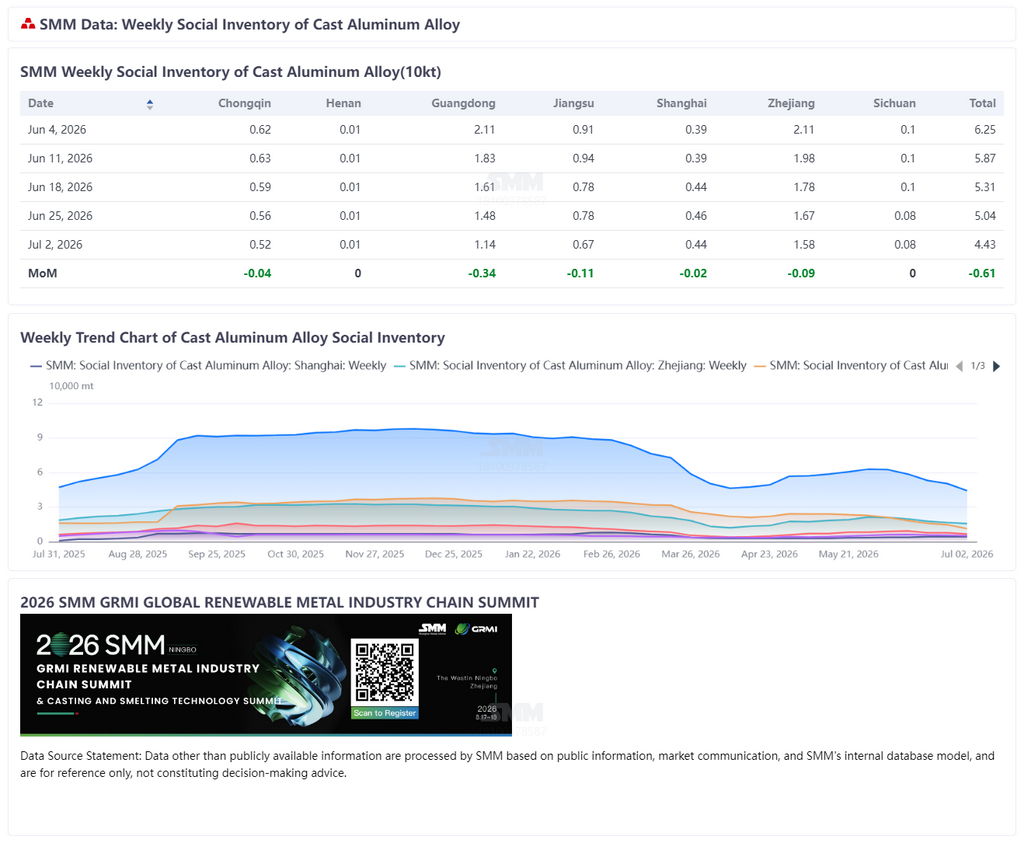

According to SMM data, social inventories of recycled aluminum alloy ingots declined by 6,100 mt week on week to 44,300 mt, marking the fifth consecutive week of inventory reductions.

Cost Advantage Remains Insufficient

Although market discussion has intensified, most producers believe that fully replacing scrap with primary aluminum in ADC12 production remains economically challenging.

ADC12 is a high-silicon, high-copper die-casting alloy. When produced from A00, additional alloying elements—including copper, silicon, iron and magnesium—must be added to achieve the required specification.

Among these, copper represents the largest cost burden, with copper additions alone costing close to RMB 1,500/mt under current market prices. Although silicon prices have softened recently and the widening aluminum-silicon price spread has partially offset alloying costs, the overall production cost remains elevated after incorporating all alloy additions and processing expenses, leaving little room for attractive margins.

According to SMM's cost model, although the continued decline in A00 prices since late June has significantly reduced the production cost of the primary aluminum route and narrowed the cost gap with the scrap-based route, the total production cost of producing ADC12 entirely from primary aluminum remains higher than that of producing it from scrap.

Product Performance Also Limits Substitution

Beyond economics, material performance presents another obstacle.

Primary aluminum and scrap-based charge mixes produce different metallurgical characteristics. ADC12 produced entirely from primary aluminum generally exhibits inferior mechanical strength and toughness compared with conventional scrap-based production, making full substitution difficult to gain acceptance among downstream die-casting customers.

As a result, primary aluminum is currently used mainly as a supplementary feedstock to alleviate raw material shortages rather than as a complete replacement for scrap.

Outlook

Overall, although discussion surrounding primary aluminum substitution has increased significantly and some producers have begun purchasing A00, the market has yet to develop into a broad industry-wide substitution trend.

The current substitution logic is driven primarily by tight availability of compliant scrap, invoice constraints, and the rapid decline in primary aluminum prices, rather than by any clear cost advantage for primary aluminum.

For most producers, purchasing A00 remains a practical measure to secure raw material supply and maintain production continuity, rather than an optimization of production economics.

Substitution opportunities also vary by alloy type. Conventional Al-Si alloys offer relatively greater substitution potential, whereas ADC12, with its high copper content, more complex alloying requirements and stringent downstream performance specifications, is considerably more difficult to replace.

Even if A00 prices continue to decline, producers are expected to increase the proportion of primary aluminum only gradually, rather than completely replacing scrap in their production process.

Looking ahead, the scale of substitution will depend largely on the ADC12-A00 price spread, the primary-to-scrap aluminum spread, the availability of compliant scrap, and the implementation of China's reverse invoicing policy. If compliant scrap remains tight, invoice-related costs stay elevated, and A00 prices continue to decline, some producers may further increase the proportion of primary aluminum in their charge mix.

Nevertheless, primary aluminum is likely to serve as only a marginal and temporary supplement to scrap, and the current production model for ADC12—centered on aluminum scrap—is unlikely to change materially in the near term.

![Coinciding with the Pre-Weekend Stockpiling Cycle, Downstream Processing Enterprises Still Mainly Make Just-in-time Procurement [SMM Spot Aluminum Midday Review]](https://imgqn.smm.cn/usercenter/tkWbz20251217171654.jpg)