Since the start of June, the tug-of-war between sellers and buyers over magnesium prices has been intensifying. The EXW price of 99.90% magnesium ingot (Fugu, Shenmu) moved sideways around 16,300–16,400 yuan/mt, with the trading range narrowing significantly. The magnesium market was mired in a supply-demand stalemate, as end-users' acceptance of high magnesium prices declined markedly, while primary magnesium smelters held their bottom line supported by costs. As a result, magnesium prices were stuck in a pattern where they could neither rise nor fall easily.

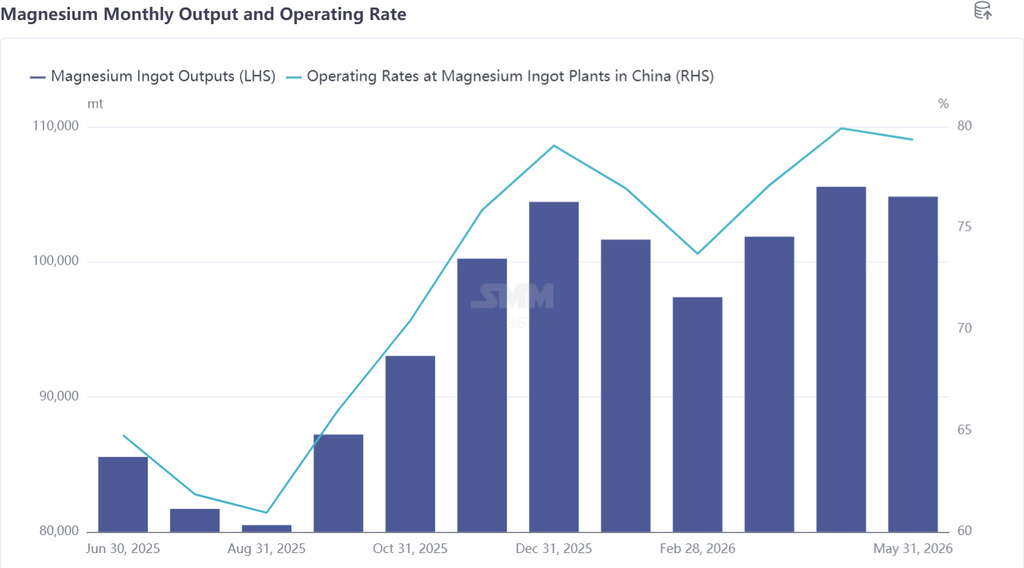

A closer look at the primary magnesium market's performance in early June reveals notable divergence between supply and demand. On the supply side, smelters in major producing regions raised output simultaneously. The drivers of the increase fell into two categories: first, enterprises operated at full capacity to dilute fixed production costs, thereby reducing the comprehensive cost per tonne of magnesium ingot; second, integrated enterprises across the entire industry chain maintained production scale to ensure internal supply of raw materials for captive use. Driven by this, the industry's overall operating rate edged up, and China's total primary magnesium production in June is expected to rise to 108,600 mt. On the demand side, off-season characteristics were pronounced. Combined with a wait-and-see sentiment toward purchases amid high spot prices, the market saw only just-in-time procurement, with overall trading sentiment mediocre. By segment, magnesium alloy plants maintained a moderate raw material procurement pace, while magnesium powder processing and overseas export orders weakened simultaneously. The market thus exhibited a structure of strong supply and weak demand. Downstream buyers' fear of high prices continued to intensify, and in the absence of concentrated restocking support, upward momentum for magnesium prices was severely lacking.

Furthermore, after the coal mine explosion in Shanxi in late May, prices of raw coal and semi-coke strengthened in tandem. Although price increases in by-products such as coal tar partially offset coal gas expenses, the price hike in semi-coke led to sales resistance, and on a comprehensive basis, coal gas costs for smelting still edged up slightly. Pressure from the raw material side continued to accumulate. Since H2 2025, the price of dolomite from Wutai, Shanxi has risen in a stepwise manner, significantly increasing smelters' procurement costs for high-quality dolomite. With multiple raw material costs rising simultaneously, many primary magnesium smelters are now approaching their break-even point. Supported by solid cost floors, producers hold firm intentions to hold prices firm.

Outlook

At present, multiple bearish factors are emerging in the magnesium market. Producers' willingness to hold prices firm and downstream buyers' fear of high prices are locked in intense standoff at the 16,300–16,400 yuan/mt level, making the direction of market prices difficult to predict.

Supply-demand pressures continue to intensify, and against the backdrop of persistently weakening end-use demand, inventories at primary magnesium smelters are accumulating overall, with the market pricing center gradually tilting toward the demand side. However, inventory structure shows clear divergence. Current producer inventories are mostly concentrated at top-tier players with strong financial strength, and available supplies in the market account for only about half of total producer inventory. The core pressure now lies in absorbing the daily surplus output generated by high operating rates.

As the hot summer season sets in, maintenance plans at primary magnesium smelters are successively implemented, and market attention gradually shifts to expectations of supply contraction due to production cuts. The market is currently in a delicate balance of ample supply and weak demand. The core focus of magnesium price dynamics going forward will revolve around a race against time between the supply contraction window created by summer maintenance-related production cuts and the period of weakening external demand brought by the summer break outside China.

Conflicting supply-demand forces persist amid buyer-seller standoff. What’s next for magnesium prices?

Since the start of June, the tug-of-war between sellers and buyers over magnesium prices has been intensifying. The EXW price of 99.90% magnesium ingot (Fugu, Shenmu) moved sideways around 16,300–16,400 yuan/mt, with the trading range narrowing significantly. The magnesium market was mired in a supply-demand stalemate, as end-users' acceptance of high magnesium prices declined markedly, while primary magnesium smelters held their bottom line supported by costs.

Data Source Statement: Except for publicly available information, all other data are processed by SMM based on publicly available information, market communication, and relying on SMM's internal database model. They are for reference only and do not constitute decision-making recommendations.

For any inquiries or for more information, please contact: lemonzhao@smm.cn

For more information on how to access our research reports, please contact:service.en@smm.cn

Related News

3 hours ago

Rising Fuel Costs and Shipping Congestion Drive Up International Magnesium Freight Rates

Read More

Rising Fuel Costs and Shipping Congestion Drive Up International Magnesium Freight Rates

[SMM Magnesium Express]Recently, due to a combination of factors including rising fuel costs driven by geopolitical conflicts and reduced turnover efficiency caused by congestion in major European ports, shipping companies have tightened capacity and raised freight rates, leading to a significant surge in international shipping costs. According to SMM research, since late June, the freight cost for magnesium ingots shipped from Tianjin Port to Rotterdam, Netherlands, has reached approximately $130 per ton, up $20 from the beginning of the month, while the average freight cost for the India route has reached $110 per ton, up $10. SMM will continue to closely monitor freight trends and make timely adjustments.

3 hours ago

Jun 17, 2026 13:45

Xinyuan Manufacturing to Accelerate Large-Tonnage Die-Casting for Magnesium Alloy Components in EVs and Robots

Read More

Xinyuan Manufacturing to Accelerate Large-Tonnage Die-Casting for Magnesium Alloy Components in EVs and Robots

[SMM Magnesium Express]On June 17, according to industry media reports, Xinyuan Manufacturing explicitly stated in its 2026 annual board report that it will accelerate the commissioning of large-tonnage die-casting and semi-solid injection molding production lines, focusing on core magnesium alloy components such as CCB brackets for new energy vehicles, rear shells for central control screens, and seat skeletons. It will also expand the application of magnesium alloy structural components in emerging fields like intelligent robots, computing cabinets, smart lawn mowing robots, and general-purpose power units. As application scenarios continue to broaden, the market potential for magnesium alloy lightweight components is expected to further expand.

Jun 17, 2026 13:45

Jun 16, 2026 18:37

China Upgrades Marine Resource Utilization: From Seawater to Mineral Extraction, Focusing on Magnesium

Read More

China Upgrades Marine Resource Utilization: From Seawater to Mineral Extraction, Focusing on Magnesium

[SMM Magnesium Express]According to Xinhua News Agency, the Ministry of Natural Resources released the "National Seawater Utilization Report 2025," indicating that China's utilization of marine resources is upgrading from "extracting water from the sea" to "extracting minerals from the sea." The report noted that Tianjin has initiated an international cooperation project titled "Key Technologies for Magnesium Extraction from Seawater/Concentrated Brine," forming a multidimensional industrial landscape for efficient resource development. Currently, there are 167 seawater desalination projects nationwide, with an annual capacity of 3.077 million tons. During the 14th Five-Year Plan period, efforts will continue to strengthen the technological reserves for strategic element extraction from seawater, contributing a "Chinese solution" to addressing global freshwater and strategic resource shortages. The industrialization process for seawater magnesium extraction is expected to accelerate.

Jun 16, 2026 18:37

Related News

Rising Fuel Costs and Shipping Congestion Drive Up International Magnesium Freight Rates

Jun 18, 2026 11:52

Xinyuan Manufacturing to Accelerate Large-Tonnage Die-Casting for Magnesium Alloy Components in EVs and Robots

Jun 17, 2026 13:45

China Upgrades Marine Resource Utilization: From Seawater to Mineral Extraction, Focusing on Magnesium

Jun 16, 2026 18:37

Magrathea Completes $100M Financing, Boosts U.S. Magnesium Smelting with Green Tech

Jun 15, 2026 17:59