Abstract: In May 2026, the global overseas stainless steel market navigated a series of sharp sentiment reversals at different stages of the month. The opening weeks saw Indonesia's mill closures and price hikes push the cost narrative to its highest point of the year, before a combination of easing geopolitical tensions and stubborn downstream resistance triggered the first price reduction since December 2025. This was swiftly followed by a flood of supply-side headlines, Indonesia's ferroalloy export nationalisation framework and NPI output cuts at the IWIP industrial park, that reignited bullish sentiment almost overnight. The month's defining characteristic was the same as April's: cost-side policy expectations repeatedly drove pricing while end-user demand consistently failed to provide meaningful confirmation. What differentiated May was the sharply higher amplitude of both the policy signals and the emotional swings that accompanied them.

I. Regulatory Tightening and Trade Policy Shifts: Indonesia Fires a Fourth Salvo, Global Barriers Keep Rising

The central policy theme in May extended the supply-side regulatory squeeze into the trade dimension, with a fresh layer of structural significance. On one front, Indonesia released a dense sequence of policy signals covering mining licence management, restrictions on new investment in nickel intermediate products, and — most consequentially — the framework for nationalising ferroalloy export rights. On the other, the European Union's upcoming TRQ safeguard measures and CBAM green-access requirements continued their measured advance, accelerating the narrowing of global stainless trade channels.

Indonesia's policy moves began at the mining level. In mid-May, the Ministry of Energy and Mineral Resources (ESDM) confirmed that it had suspended the IUP mining licences of more than 50 mining companies, including 34 nickel projects, for failing to submit their 2026 RKAB work plans on time. Those companies were given a 90-day remediation window, after which permanent revocation remains on the table. The tightening of mining approvals directly amplified market concerns about nickel ore supply stability and transmitted further pressure to the NPI production chain. Concurrently, the Weda Bay facility within the IWIP industrial park announced that high-grade NPI output would be cut by 10–15% over the coming months, with some production lines already cycling through maintenance downtime since March due to ore shortages and elevated operating costs.

Against this backdrop of simultaneous ore and smelting constraints, the directional shift in Indonesia's industrial policy became unmistakable. The government announced restrictions on new investment in nickel intermediate processing — covering NPI, ferronickel, nickel matte and MHP — signalling a deliberate move away from low-value intermediate capacity expansion and towards battery materials and higher-value downstream products. Indonesia is no longer simply seeking to maximise intermediate output; it is using mining rights, investment approvals and export channel management to progressively reshape how nickel resources are allocated and priced for export.

If Indonesia's policy changes primarily altered expectations around global stainless raw material supply, European policy continued to raise the bar for finished stainless steel entering premium consumption markets. The EU's new TRQ safeguard measures are set to take effect on 1 July, cutting import quotas by approximately 47% and raising out-of-quota tariffs to 50%. By May, the European market had already entered a "July countdown" mode, with traders rushing to lock in pre-July shipments and several major mills closing their June order books early. The tightening of quotas is not only compressing the window for Asian material to enter Europe — it is also intensifying competition for available spot material and compliant import allocations within the region itself.

Taken together, May's global stainless policy environment was characterised by simultaneous tightening across the resource, trade and carbon-cost dimensions. Indonesia is consolidating control over upstream resources through mining rights, smelting investment restrictions and export channel management; Europe is raising the entry bar through TRQ and CBAM. The two policy trajectories operate at different points in the supply chain, but they converge on the same outcome: a repricing and redistribution of global stainless steel trade flows. As Indonesia's export control framework and the EU's new safeguard measures formally take hold in the months ahead, regional price differentials and resource routing patterns face further reassessment.

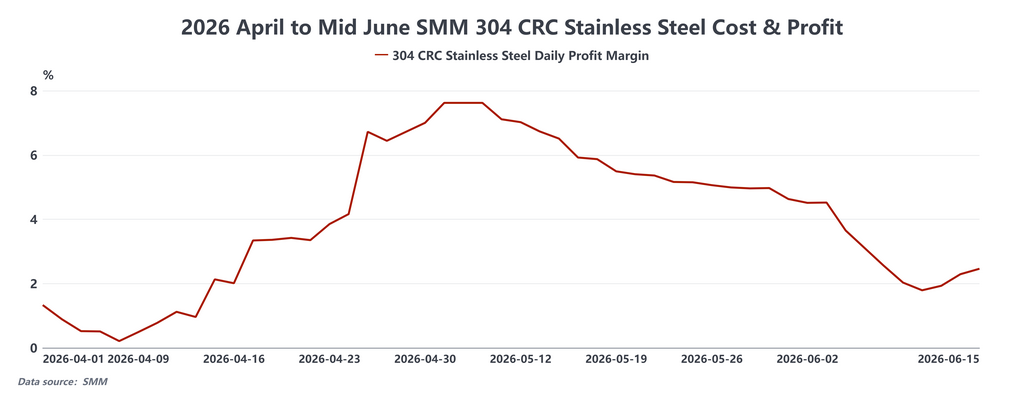

II. Prices: Cost-Driven Momentum Meets Demand Resistance

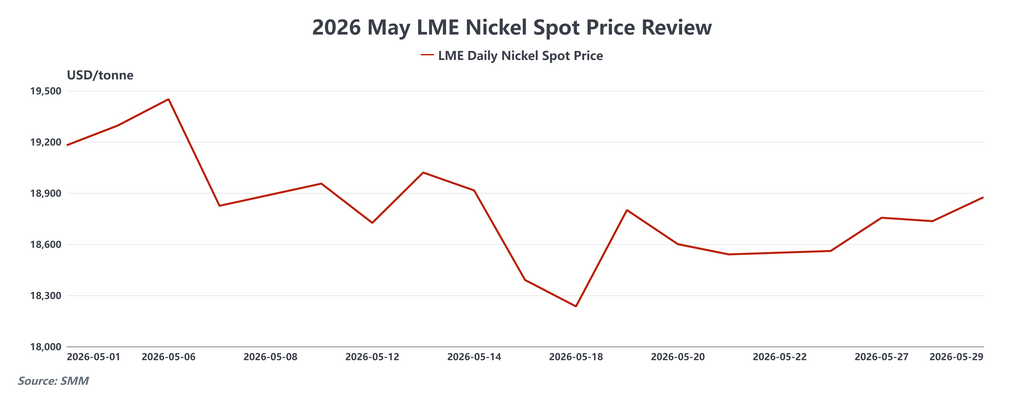

May's overseas stainless price trajectory was unusually volatile. Each turning point was accompanied by a clear trigger, Indonesian policy signals, LME nickel movements or shifts in the trade environment, yet the overarching pattern was consistent: cost-side and policy-side forces provided repeated support, while insufficient downstream absorption meant that each leg higher lacked transactional confirmation.

At the start of the month, overseas stainless prices surged on the back of Indonesian policy expectations. Following a brief mill closure, Indonesian producers raised their 304 cold-rolled export quotes by approximately USD 30/tonne, setting a new year-to-date high. On 7 May, the Indonesian government reiterated its intention to impose a floating export levy and windfall tax on lightly processed nickel products, reinforcing the market's expectation of further nickel cost inflation. LME nickel touched an intraday high of approximately USD 19,450/tonne, while the SHFE front-month nickel contract surged by more than 3% in a single session. Southeast Asian stainless quotes rose sharply in the short term, but buyer acceptance of the higher prices was already showing clear signs of deterioration.

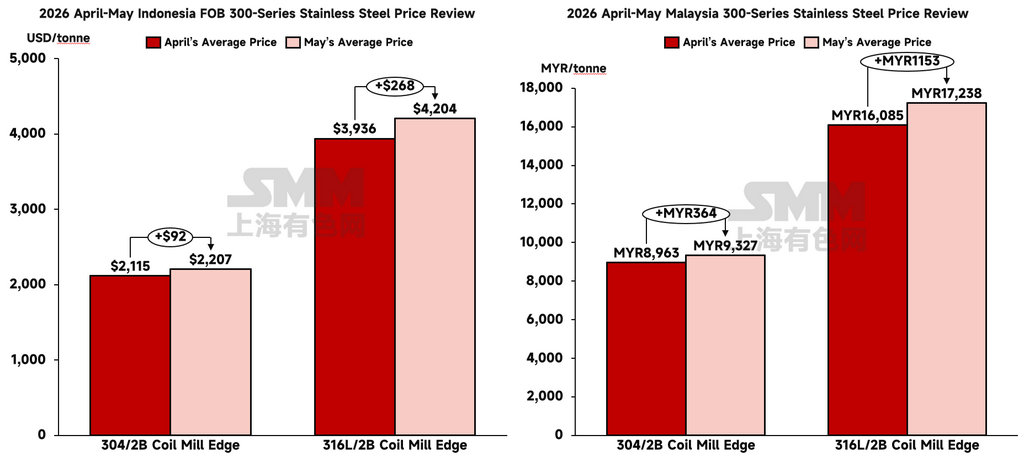

Moving into mid-month, the disconnect between asking prices and actual transaction volumes became acute. On 19 May, Indonesian mills reversed course and reduced their 304 cold-rolled export quotes by USD 30/tonne to approximately USD 2197.50/tonne, ending a run of consecutive monthly increases stretching back to December 2025. Malaysia's local stainless market followed suit, with prices declining to around MYR 9305/tonne. Rather than stimulating restocking, the price reduction reinforced a "buy the rally, not the dip" mentality among buyers, further suppressing transaction activity. The Southeast Asian market quickly entered a holding pattern — offers were firm, but actual deals were scarce, with procurement limited to immediate operational needs.

Outside Southeast Asia, price performance across Asia diverged. Taiwan's 304 cold-rolled ex-works price held at the three-year high of NT$70,500/mt, but export-side pressure mounted noticeably. Taiwan's stainless export volume fell 10.4% month-on-month to approximately 63,000 mt in May, while imports remained elevated at around 103,000 mt, squeezing local mills between weakening external demand and a continuous inflow of lower-priced import material. Indonesia's sole upward price adjustment during the month — a mid-month increase of USD 30/mt — placed additional cost pressure on buyers in Taiwan, South Korea, Vietnam and Thailand.

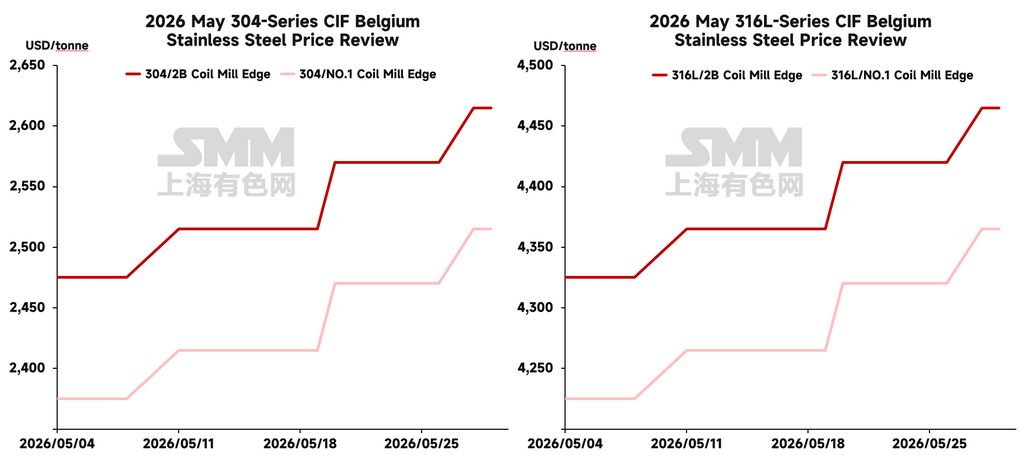

European prices continued their upward trend, though the momentum was driven more by structural supply tightness from reduced imports than by any meaningful improvement in end-user consumption. Cold-rolled stainless for July delivery rose to €2,700–2,740/mt delivered, with some mills targeting a delivered price of €2,900/mt by the end of Q3. The impending TRQ restrictions and narrowing import window are tightening European spot availability and shifting the price centre of gravity higher. Distributors, however, remain caught between elevated restocking costs and limited ability to pass those increases through to end customers, with margin compression continuing across the channel.

III. Supply and Demand: Mining Tightness and NPI Output Cuts Define the Raw Material Narrative

The overseas stainless raw material picture in May was characterised by a notable dislocation: spot prices softened while forward cost expectations continued to build. On the near-term side, a pullback in finished stainless prices, compressed mill margins and sluggish physical demand led to modest declines in NPI and ferrochrome spot quotes. Yet simultaneously, tightening Indonesian mine approvals, rising NPI curtailment expectations and the advancing export control framework were consistently pushing market participants to mark up their estimates of future raw material costs. This divergence between near-term price softness and medium-term cost anxiety was a key driver of May's price volatility.

Ore supply tightness remained the foundational support for the elevated cost floor. Indonesia's 2026 RKAB quota of approximately 200 million wet metric tonnes is approaching its approved ceiling, and the suspension of over 50 mining companies' IUP licences further compressed near-term extractable supply. High-grade nickel ore premiums stayed elevated, and spot supply anxiety showed few signs of easing. The Philippines provided some offset through seasonally higher pre-wet-season ore shipments, but this incremental supply was insufficient to materially alter the underlying tightness in nickel ore availability.

On the NPI side, supply constraints compounded. IWIP's high-grade NPI output is expected to be reduced by 10–15% over the coming months, with some lines already in curtailed or rotational maintenance mode since March and April due to insufficient ore and elevated operating costs. Additional pressure came from electricity competition with new electrolytic aluminium capacity sharing the same grid infrastructure. Given Indonesia's central role in global NPI and stainless feedstock supply, any sustained production curtailment exerts a persistent drag on the region's stainless cost structure.

On the demand side, the picture was one of widening regional divergence. India stood out as the strongest-performing single market in May. Infrastructure and automotive sector demand remained robust, and the extension of India's BIS certification exemption to 26 October kept import channels open and improved the availability of raw material in the domestic market. Demand resilience, combined with accessible import channels, reinforced India's position as an important incremental destination in Asian stainless trade flows.

Europe presented a sharply contrasting picture. Local end-user demand has not recovered in any meaningful way — Aperam noted that European consumption remains approximately 20% below historical averages. The restocking activity observed in May was primarily a function of traders pre-positioning ahead of the July TRQ implementation rather than an expression of genuine downstream pull. As the 1 July deadline approached, traders accelerated their efforts to secure pre-July shipments, pushing European prices higher — but this price appreciation reflected structural supply compression from the narrowing import window, not an expansion of underlying consumption.

IV. Outlook: The Verification Phase Begins

Taking May's policy cadence and price trajectory together, the global overseas stainless market enters June at a pivotal juncture. Market attention will shift from policy expectations themselves to whether those policies are actually capable of changing raw material supply patterns, export timing and regional cost structures. In this sense, June will serve as a crucial test of whether accumulated cost expectations can translate into sustained price gains — and its outcome will set the tone for the second half of 2026.

From a global trade flow perspective, the structural rerouting of stainless steel resources is likely to continue accelerating. As the EU's new TRQ measures take effect in July, CBAM enforcement deepens, and protective trade measures in markets such as the UK are upgraded, the channels through which Asian stainless producers can access European end markets will narrow further. The natural consequence is intensifying resource competition in ASEAN, India and the Middle East — markets that are already absorbing redirected flows from both Chinese and Indonesian producers.

Regulatory compliance is also emerging as a meaningful new layer of market stratification. Producers with low-carbon manufacturing routes, robust carbon traceability systems and environmental product declaration certifications — such as Taiwan's Yieh United Steel, which received EPD certification in May, and Japan's JFE, whose new electric arc furnace in Chiba commenced commercial production in the same month — are positioning themselves to capture what may prove to be a structural compliance premium in trade flows to Europe and other regulated markets. The cost gap between high-carbon and low-carbon routes is likely to widen as CBAM enforcement matures.

On balance, June does not lack for cost and policy support. But the critical variable determining whether price gains prove durable remains the degree to which transactions actually materialise. If Indonesia's export control framework is implemented smoothly, Europe's pre-July restocking window extends as expected, and Indian demand maintains its resilience, the overseas stainless price centre of gravity retains meaningful upside. If, on the other hand, policy execution falls short of market expectations and end-user resistance to elevated prices persists, the market could revert to the pattern that has characterised much of 2026 so far: strong cost support, firm offered prices, and consistently insufficient follow-through in actual deal flow.

![[NPI Daily Review] Supply Tightness Strengthens Willingness to Hold Prices Firm, NPI Price Center Rises](https://imgqn.smm.cn/usercenter/qLeLR20251217171733.jpg)