SMM June 15 News:

Metal market:

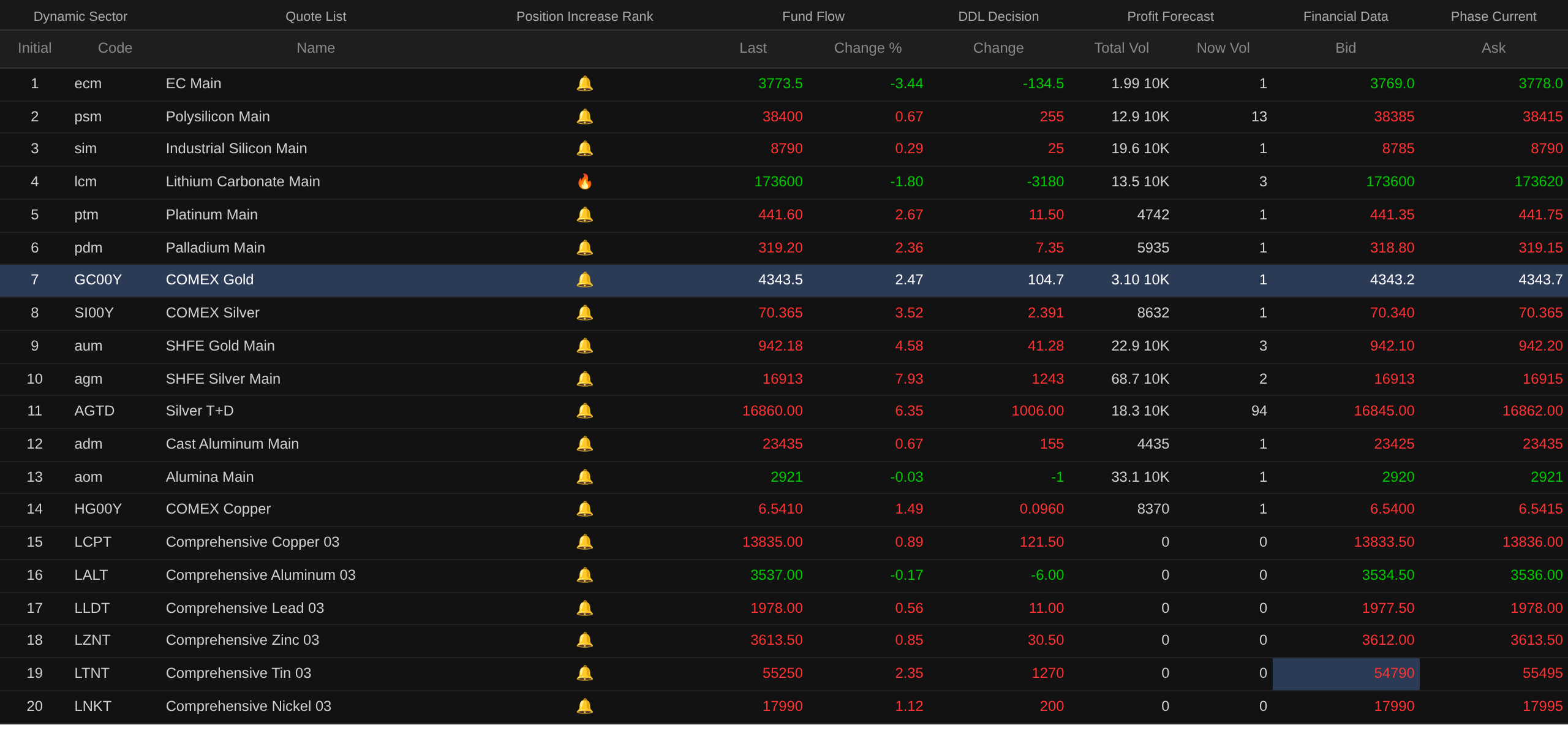

As of the midday close, domestic base metals moved higher across the board. SHFE copper rose 1.35%, SHFE tin rose 4.35%. SHFE nickel rose 1.27%, SHFE aluminum rose 0.31%, SHFE zinc rose 2.37%, SHFE lead rose 1.21%.

Additionally, the most-traded cast aluminum futures contract rose 0.67%, while the most-traded alumina contract edged lower. The most-traded lithium carbonate contract fell 1.8%, the most-traded silicon metal contract rose 0.29%, and the most-traded polysilicon futures contract rose 0.67%.

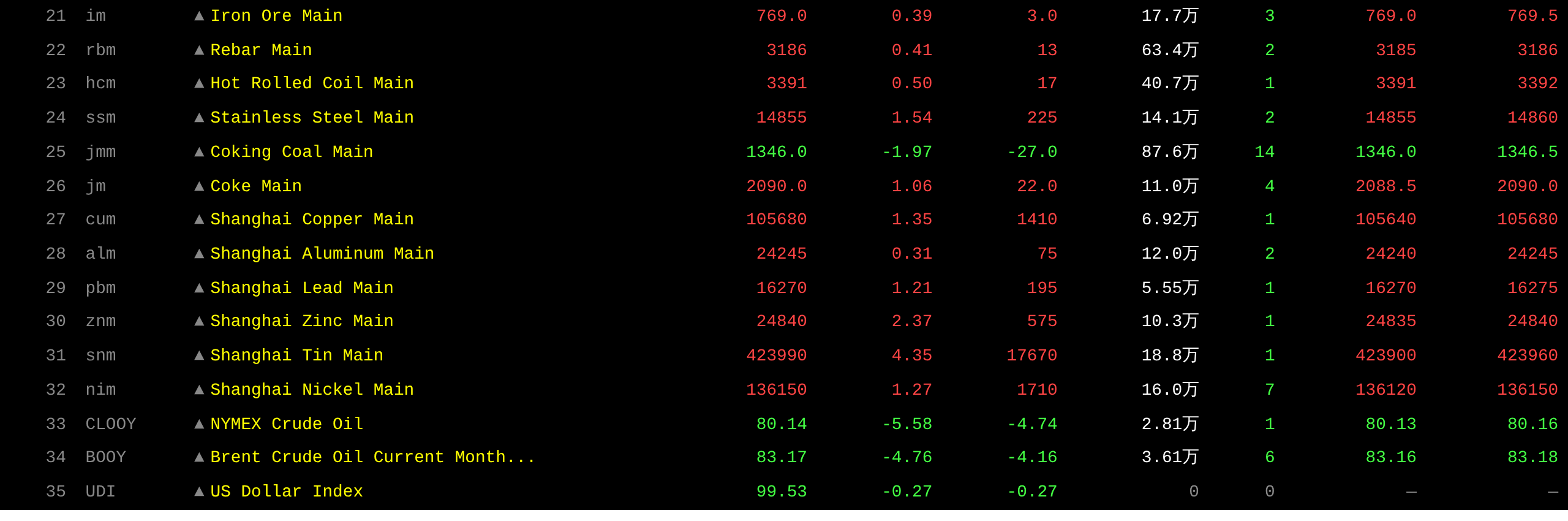

Ferrous metals rose broadly, with iron ore up 0.39%, rebar up 0.41%, hot-rolled coil up 0.5%, and stainless steel up 1.54%. Coking coal and coke: The most-traded coking coal contract fell 1.97%, and the most-traded coke contract rose 1.06%.

Overseas base metals: As of 11:38, LME metals nearly all rose. LME copper rose 0.89%, LME aluminum fell 0.17%, LME lead rose 0.56%, LME zinc rose 0.85%, LME tin rose 2.35%, LME nickel rose 1.12%.

Precious metals: As of 11:38, COMEX gold rose 2.47%, COMEX silver rose 3.52%. Domestic precious metals: The most-traded SHFE gold contract rose 4.58%, and the most-traded SHFE silver contract rose 7.93%.

Furthermore, as of the midday close, the most-traded platinum futures contract rose 2.67%, and the most-traded palladium futures contract rose 2.36%.

As of the midday close, the most-traded Europe route container shipping futures contract fell 3.44% to 3,773.5 points.

As of 11:38 on June 15, some futures midday market quotes:

Spot and Fundamentals

Zinc: Today, mainstream transaction prices for #0 zinc were concentrated at 24,650-24,885 yuan/mt, Shuangyan mainstream transactions were at 24,740-24,945 yuan/mt, and #1 zinc mainstream transactions were at 24,580-24,815 yuan/mt. In early trading, market quotes against SMM’s average price were at premiums of 10-30 yuan/mt, with no quotes against the futures price yet...

Macro Front

Domestic:

[NDRC and Other Departments: Launching a Three-Year Campaign for Key Industries’ Energy-Saving and Carbon-Reducing Transformation] The National Development and Reform Commission (NDRC) and other departments have decided to organize a three-year campaign for energy-saving and carbon-reducing transformation in key industries, including steel, aluminum, cement, flat glass, oil refining, ethylene, synthetic ammonia, methanol, and coal-fired power. It was mentioned that key industries have large-scale and high-intensity energy consumption and carbon dioxide emissions, making them the top priority for improving energy efficiency, reducing coal consumption, and lowering carbon emissions. Starting from 2026, nine key industries—steel, aluminum, cement, flat glass, oil refining, ethylene, synthetic ammonia, methanol, and coal-fired power—will be the focus of a three-year initiative to fully implement energy-saving and carbon-reduction retrofits. This aims to drive enterprises to elevate their energy and carbon efficiency levels as much as possible, leading to a marked improvement in the green and low-carbon development of these industries. Beginning in 2028, the scope of implementation will be further expanded based on practical circumstances, with additional industries advanced in a phased manner. All regions may proceed in an orderly fashion as needed, based on local conditions.

[PBOC Reverse Repo Injects Net 206.5 Billion Yuan Today] The PBOC conducted a 425 billion yuan 7-day reverse repo operation in the open market at an interest rate of 1.40%, unchanged from the previous day. Today, 218.5 billion yuan in reverse repos matured.

US Dollar:

As of 11:38, the US dollar index fell 0.27% to 99.53. Easing tensions in the Middle East led the market to scale back bets on US Fed interest rate hikes. Interest rate swaps showed traders now see a roughly 60% probability of the Fed raising rates by 25 basis points before December, down from about 80% last Friday. (Jinshi Data APP)

Additionally, according to the CME "FedWatch" tool: The probability of the Fed holding interest rates steady in June is 98.5%, with a 1.5% chance of a cumulative 25-basis-point cut. The probability of holding rates steady through July is 91.3%, with a 7.4% chance of a cumulative 25-basis-point hike and a 1.4% chance of a cumulative 25-basis-point cut. (Jinshi Data APP)

On the data front: US consumer confidence rebounded for the first time in four months in early June, as lower gasoline prices offered some relief to Americans grappling with surging inflation. A survey released Friday showed the University of Michigan's preliminary consumer sentiment index for June rose to 48.9 from May's record low of 44.8. Economists had expected a modest recovery to 46. Consumers anticipated prices would rise 4.6% YoY over the next year, down from 4.8% in May. They also projected costs would climb at an average annual rate of 3.4% over the next five to ten years, also below the prior month's expected increase. Although gasoline prices remain higher than pre-Ukraine war levels, the decline in recent weeks has lessened pessimism about personal finances among Americans. The report showed a notable improvement in sentiment among lower-income consumers, who typically allocate a larger share of their budgets to fuel costs. Nevertheless, against the backdrop of the Iran war and the resulting wave of inflation, overall economic sentiment remains at historically depressed levels. Survey Director Joanne Hsu stated, "While there has been some relief, gasoline prices still have a significant impact on consumers. As a result, current price levels remain broadly unacceptable to consumers and have dampened their view of the economy." (Jin10 Data APP)

Data:

Today will see the release of Switzerland’s May Consumer Confidence Index, the Eurozone’s April seasonally adjusted trade balance, Eurozone April industrial production MoM, Canada April wholesale sales MoM, the US June Empire State manufacturing index, US May industrial production MoM, the US June NAHB Housing Market Index, and China’s May total electricity consumption YoY (to be determined), among other data. Attention should also be paid to: ECB President Lagarde’s speech; the National Energy Administration’s release of total electricity consumption data around the 15th of each month; and the opening of the G7 summit, which runs through June 17.

Crude Oil:

As of 11:38, oil prices on both sides of the Atlantic fell sharply, with WTI down 5.58% and Brent down 4.76%. A US-Iran peace agreement is expected to be signed soon, easing market concerns over crude supply and putting oil prices under pressure.

According to Xinhua News Agency, US President Trump stated on social media on the 14th that with the signing of the US-Iran agreement on the 19th, the Strait of Hormuz will be reopened for mine-clearing operations. Iran’s Deputy Foreign Minister also indicated that an immediate and permanent halt to military operations on multiple fronts, including in Lebanon, will be announced starting tonight.

Patrick DeHaan, head of petroleum analysis at GasBuddy, said the US nationwide average gasoline price fell below $4 per gallon on Sunday for the first time since April 20. He expects that in an optimistic scenario, the nationwide average price could fall below $3.75 per gallon before July 4, but the hurricane season could be a major variable in the latter half of the summer. "The coming weeks are critical—any major misstep could significantly impact the subsequent oil price trajectory." (Wall Street CN)

Spot Market at a Glance:

►

►

►

►

►

►

►

►

►

►

►

►

![US-Iran peace agreement boosts market sentiment, SHFE zinc hovers at highs [SMM Zinc Brief]](https://imgqn.smm.cn/usercenter/Txorc20251217171755.jpg)

![SHFE Copper 2606 Contract Last Trading Day, Copper Prices Rose, Spot Premiums Were Slightly Under Pressure [SMM Shanghai Spot Copper]](https://imgqn.smm.cn/usercenter/grvgR20251217171710.jpg)