In May, key materials for sodium-ion batteries sustained their strong momentum, with both cathode and hard carbon anode recording sharp YoY and MoM growth. Top-tier players’ order books were full and capacity utilization rates approached their limits. On the supply side, the pattern of rising volumes and stable prices was pronounced, yet pressure to pass on rising raw material costs was also building. Meanwhile, capacity expansion expectations for Q3 became progressively clearer, setting the stage for the sodium-ion battery industry chain to scale up in H2.

Cathode Material: Surge in Demand Boosts Capacity Utilization, Cost Pressures Force Price Increases

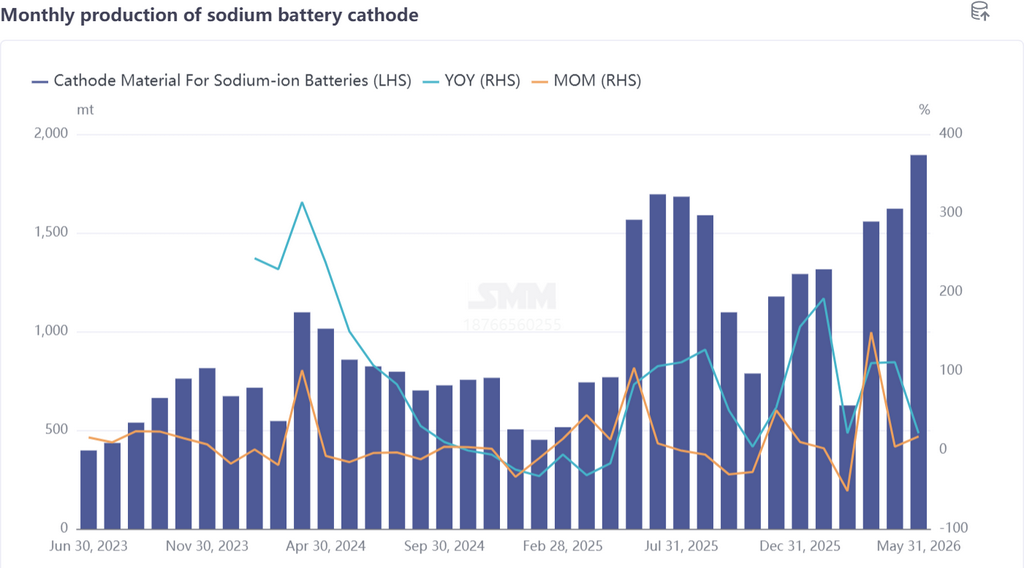

In May, production of sodium-ion battery cathode material rose 17% MoM and 21% YoY. The polyanion route accounted for as much as roughly 87% of output, with NFPP’s share up 5 percentage points MoM, further cementing its dominance. Top cathode enterprises progressively delivered orders, but available capacity had become a bottleneck, creating an undersupply situation. Simultaneously, leading players intensively launched next-generation products in May, offering comprehensive performance upgrades that continuously enhanced the competitiveness of sodium-ion batteries in application scenarios. On the supply side, leading cathode plants had begun preparing for capacity expansion, and a significant release of sodium-ion battery cathode capacity is expected in Q3.

However, the current order boom was heavily concentrated among top-tier players. Midstream cathode producers, constrained by capacity scale, continued to produce based on demand, send samples for validation, and develop clients at a gradual pace, and had yet to fully benefit from the demand surge.

Cost side, NFPP raw material costs continued to climb in May: iron phosphate prices rose, and sodium salts such as monosodium phosphate and sodium pyrophosphate also surged. Although mass production scale had improved from earlier and production line processes had been upgraded, the broad-based rise in raw material prices still drove a significant cost increase. Consequently, NFPP prices are expected to increase going forward, to ease cost pressure. In terms of product structure, the share of layered oxide cathodes narrowed further, market concentration continued to rise, and demand was concentrated in niche applications such as two-wheelers and start-stop power supplies.

The layered oxide segment faces the challenge of accelerating contraction. Looking ahead to June, demand for sodium-ion battery cathodes remains on an upward trajectory, production schedules are expected to continue growing, and June output is projected to increase 1% MoM and 24% YoY.

Hard Carbon Anode: Full Capacity Utilization, Toll Processing to Fill Gaps, Sustained Premium for Quality Products

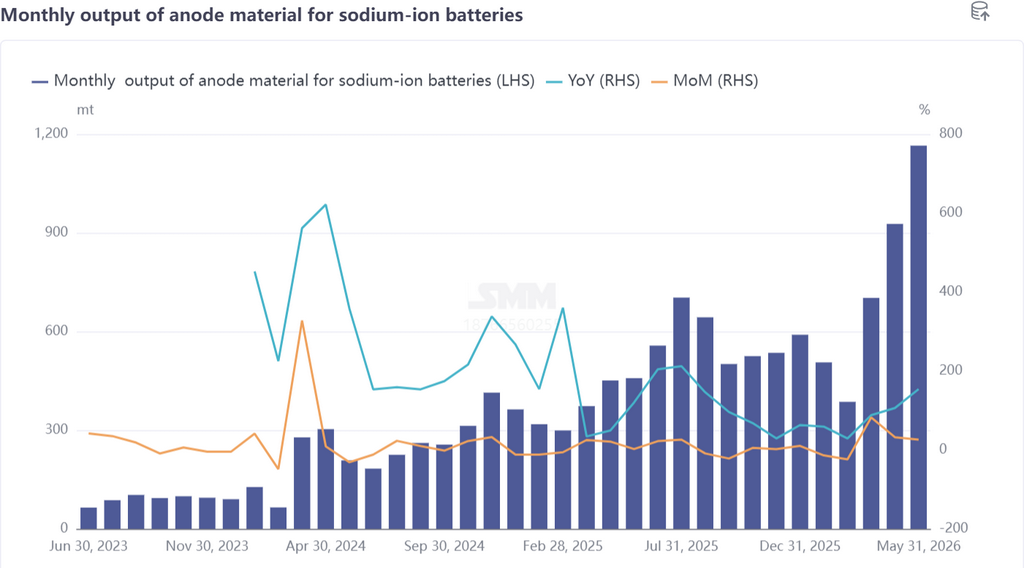

In May, production of sodium-ion battery anode materials rose 26% MoM and surged 154% YoY, moving in tandem with the cathode side. Leading hard carbon enterprises are in the capacity ramp-up stage, with ample orders on hand and new orders continuing to improve.Shortfalls from insufficient existing capacity are being covered through external toll processing. Recently, some hard carbon producers have brought new capacity on stream, and as this capacity is gradually ramped up and released, the supply side of sodium-ion battery anodes is expected to see a notable boost in Q3.

On the price front, premiums for high-performance hard carbon products remain firm. Hard carbon grades with outstanding cycle life, low-temperature performance, and C-rate capabilities are primarily used in energy storage, start-stop, and other applications, with prices generally above 30,000–40,000 yuan/mt and high-end products reaching 50,000–60,000 yuan/mt.

The price spread between premium hard carbon and ordinary products reflects the market’s differentiated pricing logic based on material performance. Looking ahead to June, demand for hard carbon anodes remains favorable, with production expected to increase 9% MoM and 128% YoY.

Summary

Overall, the sodium-ion battery cathode and anode material market in May exhibited three core characteristics: First, a pronounced top-tier effect, with orders and capacity expansion concentrated among a few leading enterprises, while mid- and tail-end producers have yet to enter the volume ramp-up stage.Second, cost-side pressure, as rising upstream raw material prices are forcing cathode product prices higher, putting profitability to the test. Third, the pace of capacity expansion is accelerating, and capacity release in Q3 will be a key variable for the scale leap of the sodium-ion battery industry chain in H2. Structurally, the dominance of the polyanion route has been further reinforced, while the space for layered oxide cathodes continues to narrow, making the landscape of technological divergence increasingly clear. Looking ahead to June and Q3, as capacity is gradually brought on stream and demand continues to flow in, the sodium-ion battery material market is expected to enter a new phase of rising volumes and prices.

![[CATL's Wu Kai: Sodium-ion mass production this year, lithium-air next]](https://imgqn.smm.cn/usercenter/MaxcL20251217171730.jpg)

![[Sodium Battery: Fujian Nate Energy Sodium Battery Project Receives Environmental Assessment Acceptance]](https://imgqn.smm.cn/usercenter/tKgKv20251217171725.png)