Recientemente, los datos mensuales de producción y ventas de vehículos de pila de combustible publicados por la CAAM (Asociación China de Fabricantes de Automóviles) han revelado una tendencia notable. A finales de 2025, el mercado experimentó un aumento significativo, con producción y ventas alcanzando máximos históricos. Sin embargo, tras entrar en 2026, los datos cayeron rápidamente, borrando prácticamente las ganancias anteriores. Este patrón de "pico a fin de año, enfriamiento a principios de año" no es casual, sino un reflejo típico de la interacción entre los ciclos políticos y la transformación industrial.

I. Señales de los datos: auge a fin de año, caída a principios de año

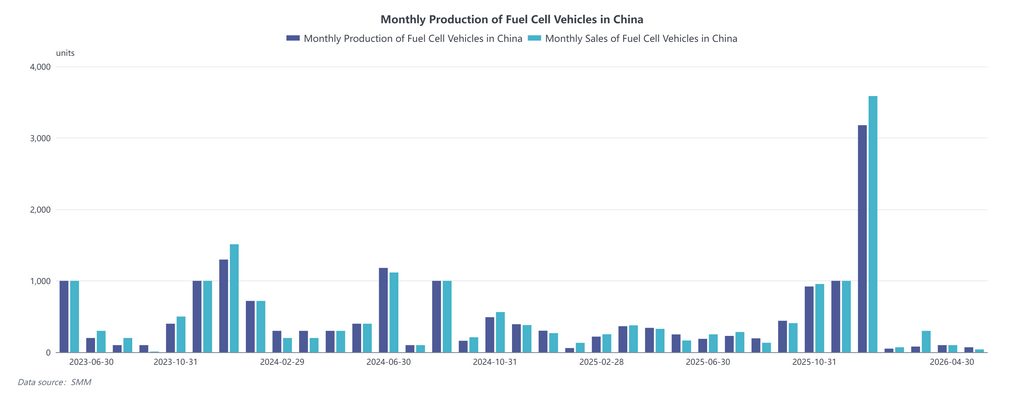

Observando el gráfico de tendencias, durante la mayor parte del período de 2023 a 2025, la producción y ventas mensuales de vehículos de pila de combustible fluctuaron por debajo de las 1.000 unidades, con solo pequeños picos ocasionales. Pero en los dos últimos meses de 2025, la curva se empinó bruscamente: solo en diciembre la producción superó las 3.200 unidades y las ventas las 3.500, estableciendo un nuevo récord histórico.

El problema es que este "máximo histórico" no se mantuvo. De enero a abril de 2026, la producción y las ventas cayeron por debajo de las 100 unidades mensuales, y el impulso del mercado se desvaneció rápidamente. Este patrón pulsátil "impulsado por políticas" pone de manifiesto una vez más la sensibilidad de la industria a los ciclos políticos.

II. Análisis de atribución: entregas concentradas antes del cierre de la ventana de subsidios

El auge de ventas a finales de 2025 puede atribuirse en gran medida a la conclusión de las tareas de los clústeres de ciudades de demostración y a la liquidación centralizada de las políticas de subsidios. A medida que el "XIV Plan Quinquenal" y el primer lote de clústeres de ciudades de demostración de vehículos de pila de combustible entraban en su fase final, todas las partes necesitaban completar la entrega de vehículos, el registro y la activación del sistema antes de los plazos de evaluación para asegurar los subsidios completos. Este efecto de "carrera por instalar" infló artificialmente las cifras mensuales.

Sin embargo, la "puesta en marcha" de estos vehículos no equivale a una operación comercial genuina. En cierta medida, fue un esfuerzo concentrado para cumplir las condiciones de los subsidios, lo que sigue estando algo desconectado de la demanda real del mercado.

III. Transición política: el "XV Plan Quinquenal" se orienta hacia las operaciones

Los bajos datos de principios de 2026 pueden entenderse como un fenómeno de "vacío político" durante el período de transición: el antiguo modelo de subsidios a la compra se está eliminando gradualmente, mientras que el nuevo mecanismo aún no ha entrado plenamente en vigor. Esto también indica que la industria del hidrógeno no se ha liberado fundamentalmente de la dependencia del apoyo político.

De cara al "XV Plan Quinquenal", la orientación política está experimentando un cambio claro: ya no se centra únicamente en el número de vehículos promovidos, sino que presta más atención a la producción, almacenamiento, transporte y repostaje de hidrógeno verde, así como a la viabilidad económica de toda la cadena de valor. El modelo de subsidios también está pasando de "comprar un vehículo te da dinero" a "usar hidrógeno te da subsidios", es decir, los incentivos se basarán en el kilometraje operativo real y el uso de hidrógeno verde.

Esto implica que la lógica de competencia futura del mercado pasará de "quién puede asegurar cuotas" a "quién puede hacer funcionar el modelo de costes".

IV. Perspectivas: de "impulsado por políticas" a "crecimiento endógeno"

El auge a finales de 2025 y la caída a principios de 2026 no son simples fluctuaciones del mercado, sino un microcosmos de la transición de la industria desde una fase de apoyo político hacia una fase de transformación orientada al mercado. Para la industria, la cuestión clave en los próximos años será si puede realmente reducir los costes totales del ciclo de vida, ampliar los escenarios de aplicación y mejorar la infraestructura, lo que determinará en última instancia quién permanece en la mesa.