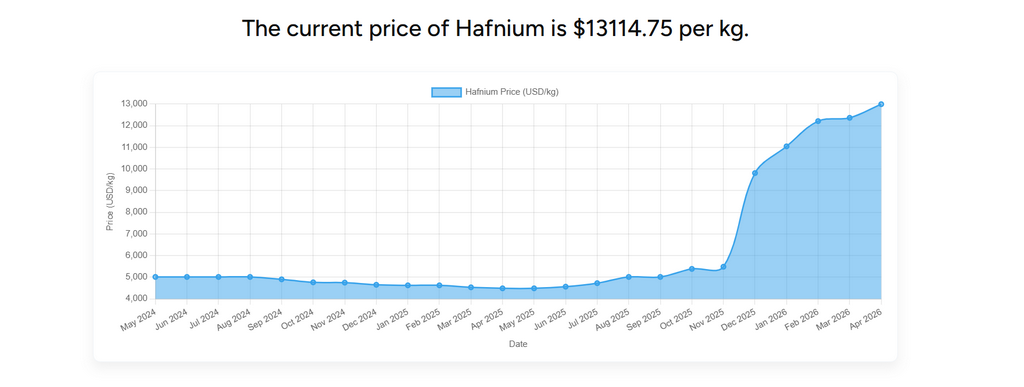

Based on recent market data, overseas hafnium prices surged in Q4 2025 after a prolonged period of stability. From May 2024 to October 2025, prices hovered around $5,000/kg. Starting November 2025, they rose sharply, reaching $13,114.75/kg by April 2026—a gain of over 140%. This was driven by both demand and supply factors.

On the demand side, hafnium is critical for advanced semiconductor manufacturing, particularly as hafnium dioxide in high-k metal gates for leading-edge chips. Growth in AI, high-performance computing, high-bandwidth memory, and advanced DRAM has steadily lifted hafnium consumption, given its rigid requirement in wafer fabrication.

On the supply side, China, a dominant refiner, imposed export controls on hafnium from H2 2025 to safeguard strategic resources. This created a significant overseas supply gap. Facing anticipated tightening, chipmakers and traders stockpiled, and some engaged in hedging, leading to a supply-demand imbalance that drove the price spike into early 2026.

In summary, the price rise stems from rising AI-driven semiconductor demand and supply shortages triggered by export controls. Since hafnium is a by-product of zirconium mining, capacity cannot be quickly ramped up, and developing alternative supply chains requires long validation and build-out cycles. Prices are therefore expected to remain elevated unless the supply-demand structure improves. For downstream users, building strategic supplier partnerships and appropriate inventories is currently the primary approach to managing price volatility.