SMM, May 29:

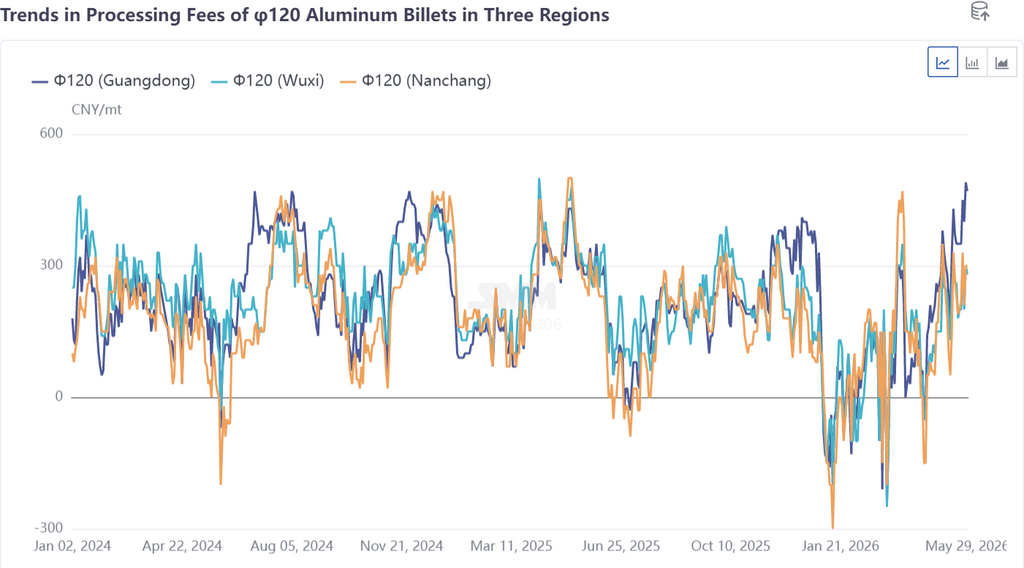

Since late April, aluminum billet processing fees in China's three major consumption regions have seen a strong rebound, with south China taking the lead. The φ120 aluminum billet (Guangdong) hit a Q2 low of -40 yuan/mt on April 16 in terms of negative processing fees, then rose rapidly, approaching the 500 yuan/mt mark by month-end in May, and reaching a new yearly high of 490 yuan/mt on May 28. SMM believes there are three main reasons:

1. Aluminum price pullback and Shanghai-Guangdong price spread factors: Since mid-to-late April, spot aluminum prices in the three major consumption regions pulled back sharply by over 1,000 yuan/mt, which helped boost downstream purchasing sentiment. The price spread between east China and south China stayed high — as of May 29, the Shanghai-Guangdong price spread remained as high as 150 yuan/mt. The willingness to ship aluminum billet from north China to south China for sale was insufficient, causing an imbalance in inter-regional cargo flow.

2. Supply-side disruption factors: Recently, from the supply side, as China is further regulating aluminum capacity operations, some regions — particularly south-west China — experienced liquid aluminum undersupply, causing some billet plants to passively cut production despite high processing fees. Meanwhile, the weak performance of aluminum billet processing fees since Q1 led to concerns over profitability for aluminum billet enterprises. Some regional billet plants reduced production efficiency and planned ahead to achieve marginal production cuts through production line maintenance, equipment servicing, product switching, and raw material reduction. In late May, some enterprises still had plans to carry out short-term production shutdowns for maintenance as scheduled.

3. Mild recovery on the demand side: Over the past week, the operating rate of China's aluminum extrusion industry was recorded at 57.6%, up 0.2 percentage points WoW, with the industry's operating rate continuing a mild recovery trend. In terms of architectural extrusion, some enterprises organized production based on large-scale engineering project orders on hand, providing support for overall operating rates. Enterprises in the Shandong region reported that with temperatures steadily rising recently, north China entered the construction window period, boosting end-use demand for home renovation, door and window replacement, and other segments. In terms of industrial extrusion, the recent phased weakening of aluminum prices increased downstream purchase willingness, driving order growth and boosting operating rates. In addition, PV frame enterprises in Hebei reported that some delivery orders were due in early June, with production schedules increasing this week, driving operating rates to rise. Overall, although the real estate market recovery remained weak, large-scale engineering orders on hand offered volume advantages with longer delivery cycles, providing stable support for recent operating rates. Combined with rising temperatures boosting home renovation and door/window consumption, architectural extrusion operating rates are expected to continue recovering, with stable rigid demand from downstream in south China. Industrial extrusion fundamentals showed strong resilience with stable downstream manufacturing rigid demand, but caution is needed regarding subsequent aluminum price fluctuations that may suppress downstream purchasing sentiment. The aluminum extrusion operating rate is expected to continue its upward trend next week.

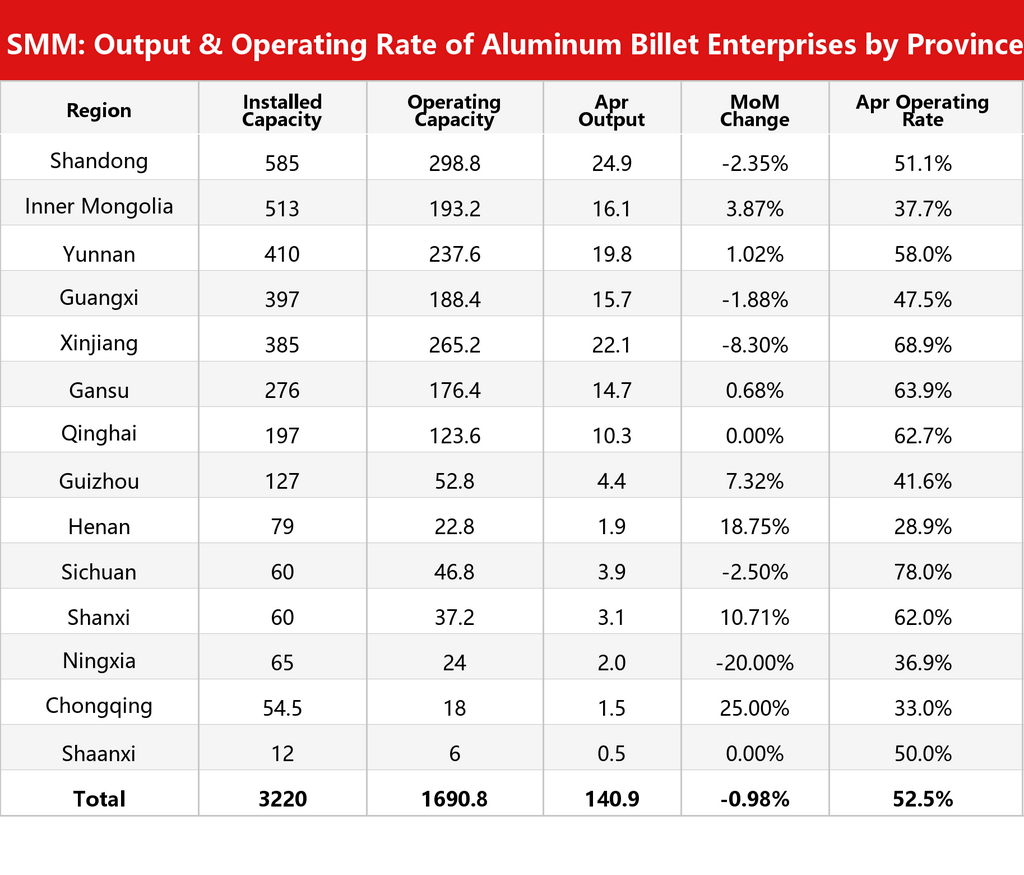

Review of Primary Aluminum Billet Supply in China, April-May: Insufficient Production Momentum at Enterprises, Operating Rate Rebound Falling Short of Expectations

In April, the aluminum billet operating rate pulled back slightly by 0.7 percentage points MoM to 52.5%, down 3.6 percentage points YoY. In April, China's aluminum billet sector maintained stable operations overall, but slightly below the previous month's expectations and still lower compared to the peak season levels of the same period in previous years, with the intensifying cut-throat competition remaining a severe challenge. As the rush period for PV and battery panel export orders came to an end, industrial billet orders pulled back. Combined with the renewed weakening of aluminum billet processing fees in the first half of April, some medium-to-large aluminum billet enterprises carried out preemptive production cuts. The supply-demand structural imbalance continued to become more prominent, with persistently high resistance to industry shipments. Meanwhile, competition in aluminum billet processing fees grew increasingly fierce, and the cut-throat competition trend continued to intensify. At this stage, the market has widely adopted a business model of low-price volume sales, and the procurement side has also generally followed market trends and purchased based on prevailing prices, which has become the industry norm. Considering the current industry landscape, the aluminum billet market is unlikely to see a strong reversal in the short term, but the resilience of the aluminum billet market since May has exceeded our expectations.

Looking ahead to May, it is worth noting that as the transition from off-season to peak season progresses, the period from May to July enters a high-incidence season for phased production suspensions and cuts in the aluminum billet sector, with signs of this already emerging in south-west China. Although aluminum billet processing fees in three regions showed signs of bottoming out since late April, the performance since Q1 has raised concerns about the profitability of aluminum billet enterprises. Production efficiency at billet plants in some regions has weakened, with enterprises resorting to production line maintenance, equipment servicing, product switching, and raw material reductions to achieve marginal production cuts. The operating rate of aluminum billets in China is expected to show no significant improvement in May. Overall, direct exports of aluminum billets are still in the early stage of ramping up, while the recovering processing fees in China are favorable for the production enthusiasm of aluminum billet enterprises. Primary aluminum price fluctuation trends, the pace of profile end-user export orders, and the sustainability of elevated processing fees will be the core factors determining the aluminum billet market trajectory and driving market recovery. SMM expects the aluminum billet supply side in China to rebound steadily in May, with the operating rate expected to edge up slightly to around 53.8%.

(May production data are forecast values only. Data source disclaimer: Data other than publicly available information are derived by SMM based on public information, market communication, and SMM's internal database models, and are for reference only and do not constitute decision-making advice.)

![[SMM Aluminum Flash News] Rising UK Aluminium Scrap Exports Raise Concerns Over Domestic Supply Security](https://imgqn.smm.cn/usercenter/LFPBA20251217171653.jpg)

![[SMM Aluminum Flash News] UK Scrap Aluminium Sector Needs 25% Annual Growth to Meet Future Demand](https://imgqn.smm.cn/usercenter/EVjRH20251217171653.jpg)