SMM News, May 27:

Metals market:

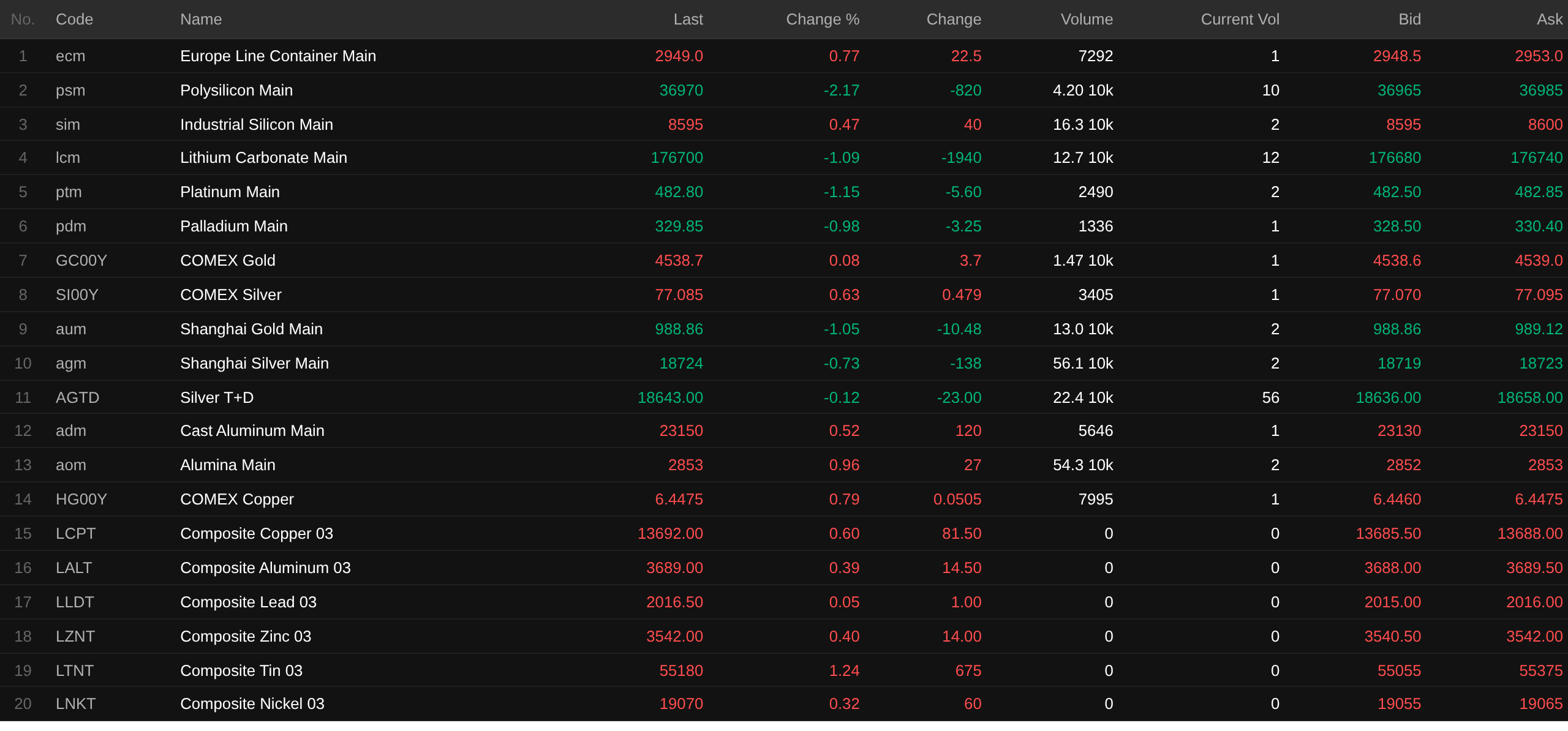

As of the midday close, most domestic base metals rose, while SHFE copper edged down. SHFE aluminum rose 0.8%. SHFE lead rose 0.33%, SHFE zinc fell 0.72%. SHFE tin rose 0.63%. SHFE nickel rose 1.91%.

In addition, the most-traded casting aluminum futures rose 0.52%, the most-traded alumina contract rose 0.96%. The most-traded lithium carbonate contract fell 1.09%. The most-traded silicon metal contract rose 0.47%. The most-traded polysilicon futures contract fell 2.17%.

Ferrous metals mostly fell. Iron ore fell 0.19%, rebar fell 0.69%, hot-rolled coil fell 0.44%, and stainless steel rose 1.49%. Coking coal and coke: the most-traded coking coal contract fell 1.48%, and the most-traded coke contract fell 1.77%.

Overseas base metals, as of 11:38, LME metals rose across the board. LME copper rose 0.6%. LME aluminum rose 0.39%. LME lead rose 0.05%. LME zinc rose 0.4%. LME tin rose 1.24%. LME nickel rose 0.32%.

Precious metals, as of 11:38, COMEX gold rose 0.08%, COMEX silver rose 0.63%. Domestic precious metals: the most-traded SHFE gold contract fell 1.05%, the most-traded SHFE silver contract fell 0.73%.

In addition, as of the midday close, the most-traded platinum futures contract fell 1.15%, and the most-traded palladium futures contract fell 0.98%.

As of the midday close, the most-traded Europe containerized freight index contract rose 0.77%, closing at 2,949 points.

As of 11:38 on May 27, midday futures quotes for selected contracts:

Spot Cargo and Fundamentals

Alumina:SMM statistics show that the scale of alumina projects under construction and under planning in Guinea has exceeded...

Macro Front

China:

[NBS: From January to April, profits of China's above-scale industrial enterprises rose 18.2%; non-ferrous metals sector profits surged 117.8%] NBS data showed that from January to April, total profits of China's above-scale industrial enterprises reached 2.44 trillion yuan, up 18.2% YoY. From January to April, the mining sector posted profits of 361.84 billion yuan, up 26.0% YoY; the manufacturing sector posted profits of 1.80 trillion yuan, up 20.4%; and the electricity, heat, gas, and water production and supply sector posted profits of 272.01 billion yuan, down 1.9%. From January to April, profitability of major industries was as follows: non-ferrous metals smelting and rolling processing (up 1.2x YoY), computer, communications, and other electronic equipment manufacturing (up 1.1x), chemical raw materials and chemical products manufacturing (up 73.4%), coal mining and washing (up 21.0%), textile (up 11.2%), petroleum and natural gas extraction (up 8.1%), petroleum, coal, and other fuel processing (turned from loss to profit), general equipment manufacturing (down 0.6%), electricity and heat production and supply (down 2.5%), special equipment manufacturing (down 7.2%), electrical machinery and equipment manufacturing (down 11.4%), agricultural and sideline food processing (down 11.8%), automobile manufacturing (down 16.8%), non-metallic minerals products (down 50.7%), and ferrous metals smelting and rolling processing (down 51.5%).

[PBOC Conducts 177.6 Billion Yuan in Open Market Reverse Repo Operations with Net Injection of 127.6 Billion Yuan in a Single Day] The PBOC conducted 177.6 billion yuan in 7-day reverse repo operations in the open market at an operation rate of 1.40%, unchanged from the previous day. 50 billion yuan in reverse repos matured today.

US Dollar:

As of 11:38, the US dollar index fell 0.05% to 99.1. According to Nikkei, Fed's Kashkari stated that the US Fed may implement a "series" of interest rate hikes in response to inflation concerns triggered by the Middle East situation. During the late-April FOMC meeting, the US Fed kept interest rates unchanged. Kashkari and two other officials dissented against the decision to include language in the Fed's statement hinting at future monetary easing. In a written interview, Kashkari said: "I think the next rate adjustment could be an interest rate cut, or it could be a rate hike." He used this to express his differing views. Kashkari said the outcome would depend on inflation trends, which depend on whether the Strait of Hormuz would reopen soon or remain effectively closed due to further damage to infrastructure in the region, the latter of which would exacerbate the global energy shortage. Kashkari said the concern was that long-term inflation expectations of enterprises and households "could become unanchored." He said the FOMC "may well need to respond forcefully," and rate hikes, or even a series of rate hikes, could be necessary measures.

According to CME "FedWatch": the probability of the US Fed keeping rates unchanged through June was 99.2%, with a 0.8% probability of a cumulative 25-basis-point interest rate cut. The probability of the US Fed keeping rates unchanged through July was 88.6%, with an 11.3% probability of a cumulative 25-basis-point rate hike and a 0% probability of a cumulative 25-basis-point interest rate cut. (Jin10 Data)

A CITIC Securities research report noted that the resilience of the global economy is being tested by the Middle East conflict, while a glimmer of hope for the resumption of navigation through the Strait of Hormuz has emerged. The US economy is likely to continue growing mildly but unevenly this year, the pace of the EU's weak recovery is being delayed, and Japan's private-sector demand is inevitably subject to disruptions from energy shortages. High oil prices are already pushing up global inflation, with headline inflation rates in Europe and the US likely to fluctuate at highs this year, while Japan's headline inflation rate may continue its mild performance. The US Fed may not cut interest rates at all this year, while potential rate hikes by the European and Japanese central banks are imminent, and the "unrestrained" fiscal stances of Japanese and European political circles could constitute a source of market risk this year. We maintain our view that US equities will outperform US Treasuries and the US dollar index will find support, while gold prices are expected to break out of their current range as tail risks to inflation dissipate.

Other currencies:

The Reserve Bank of New Zealand (RBNZ) kept rates unchanged for the third consecutive meeting, opting to continue observing the impact of the global energy shock on domestic consumption and medium-term inflation. The RBNZ's Monetary Policy Committee on Wednesday held the Official Cash Rate (OCR) at 2.25%, in line with market expectations. The RBNZ's latest projections show a rising likelihood of at least two 25bp rate hikes before year-end. In its post-meeting statement, the RBNZ said: "Taken together, the OCR will likely need to be raised sooner and by more than projected in the February Monetary Policy Statement." "The pace of hikes will depend on the relative impact of persistent wage and pricing behavior versus weakening economic activity on medium-term inflation pressures." Following the statement, NZD/USD rose. (Jin10 Data)

Bank of Japan (BoJ) Governor Ueda Kazuo said vigilance is needed regarding the impact of surging oil prices on underlying inflation trends, but did not clearly signal how this factor would influence next month's policy meeting outcome. Ueda said on Wednesday: "Japan's experience shows that oil price shocks are never just oil price shocks; they actually test the entire inflation mechanism." Reviewing the impact of oil crises since the 1970s, he noted: "We are in fact experiencing the fifth oil price shock." "If a temporary shock alters wages, inflation expectations, and corporate pricing behavior, it may evolve into persistent inflation." Ueda did not directly signal the future policy path, but as his remarks reflected concerns over the impact of high oil prices, markets may further strengthen speculation about the prospect of a rate hike at the BoJ's June meeting. Overnight swap market pricing shows traders currently assign roughly a 75% probability to a 25bp rate hike by the BoJ next month. (Jin10 Data)

Australia's April core inflation rate remained above the upper bound of the Reserve Bank of Australia's (RBA) target range, further reinforcing market expectations that the RBA will maintain its hawkish stance after consecutive rate hikes this year. Data on Wednesday showed the closely watched core inflation gauge—the annual trimmed mean inflation rate excluding volatile items—rose 3.4% YoY, in line with economists' expectations. The RBA targets keeping inflation near the midpoint of its 2%-3% target band. Interest rate swap markets currently price the probability of another rate hike in August at around 50%, down from 64% before the data release. Under the dual pressure of high borrowing costs and surging fuel prices driven by the Iran war, the Australian economy is beginning to show signs of weakness. The unemployment rate in April rose to a four-and-a-half-year high, while approximately one-third of enterprises reported declining revenue over the past four weeks, and half reported rising operating costs. The market widely expects that after raising rates at all three meetings earlier this year, the Reserve Bank of Australia will hold the cash rate unchanged at 4.35% in June. Sue-Ellen Luke, head of price statistics at the Australian Bureau of Statistics, said: "Automotive fuel prices currently remain 23.5% higher than before the outbreak of the Middle East conflict. The impact of rising oil prices is also reflected in goods and services with higher transportation and logistics costs." (Jin10 Data)

Data:

Today will see the release of the RBNZ interest rate decision as of May 27, Switzerland's May ZEW Investor Confidence Index, US weekly ADP employment change for the week ending May 9, and the US May Richmond Fed Manufacturing Index, among other data. In addition, attention should be paid to: Bank of Japan Governor Ueda Kazuo delivering a speech at a monetary policy conference hosted by the BOJ; the RBNZ releasing its interest rate decision and monetary policy statement; RBNZ Governor Breman holding a monetary policy press conference.

Crude oil:

As of 11:38, both benchmarks declined, with WTI down 2.03% and Brent down 1.75%. Oil prices fell in Asian early trading as traders weighed the prospects of a US-Iran deal. Front-month Brent crude declined. Despite a resurgence in hostilities, hopes remain for an agreement to reopen the Strait of Hormuz. Tehran signaled that the attacks would not derail negotiations, while US Secretary of State Rubio said it would take a few days to finalise a potential deal. Uncertainty remains high. Kieran Tomkins of Capital Economics noted that while crude oil options data suggest investors expect prices to pull back over the next three months, their conviction is unusually low. He said options indicate investors see a swift resumption of supply through the strait as the most likely outcome, but their implied expectations suggest a 37% probability that oil prices will exceed $100 per barrel in three months. (Zhitong Finance)

On the evening of May 26 local time, the Public Relations Department of the Islamic Revolutionary Guard Corps (IRGC) Navy announced that over the past 24 hours, 25 vessels including oil tankers, container ships, and other commercial vessels passed through the Strait of Hormuz with permission, under the coordination and security guarantee of the IRGC Navy. Meanwhile, the IRGC Navy stated that it is exercising "effective and authoritative" control over the Strait of Hormuz, and any act of aggression will be met with a severe response. (CCTV News) (Jin10 Data APP)

Spot market overview:

►

►

►

►

►

►

►

►

►

►

►

►

►

![Middle East Tensions Repeatedly Disrupted Markets, Intraday Copper Prices Retreated After Rapid Rise [SMM BC Copper Commentary]](https://imgqn.smm.cn/usercenter/kvwSZ20251217171710.jpg)

![East China Market Trading Active, Central China Remained Sluggish [SMM Spot Aluminum Midday Review]](https://imgqn.smm.cn/usercenter/IOKIL20251217171652.jpg)