Jinchengxin anunció en la noche del 22 de mayo que la empresa celebró la 22.ª reunión de la 5.ª Junta Directiva el 8 de mayo de 2025 y la 2.ª Junta General Extraordinaria de Accionistas de 2025 el 26 de mayo de 2025, en las cuales se revisó y aprobó la «Propuesta sobre la inversión planificada y construcción del proyecto minero de cobre-oro-plata Alacran». La empresa acordó invertir aproximadamente 231 millones de dólares en la construcción del proyecto minero de cobre-oro-plata Alacran con base en la proporción de participación esperada (55%). Actualmente, la participación accionaria de la empresa en la mina de cobre-oro-plata Alacran ha aumentado al 97,5%, y en consecuencia la empresa planea incrementar la inversión en construcción del proyecto en 178,67 millones de dólares conforme al cambio en la proporción de participación, elevando la inversión acumulada a aproximadamente 409,89 millones de dólares. Aparte de los cambios mencionados en la proporción de contribución de la empresa y el monto de inversión correspondiente, la estimación de inversión, el plan de construcción y otros aspectos del proyecto minero de cobre-oro-plata Alacran permanecen sin cambios, basándose aún en el estudio de factibilidad (FS) del yacimiento de cobre-oro-plata Alacran completado en diciembre de 2023 (adoptando el estándar NI 43-101).

Respecto a (1) Descripción general del proyecto, Jinchengxin anunció:

Proyecto de inversión: proyecto de minería a cielo abierto y beneficio de la mina de cobre-oro-plata Alacran. Con base en el estudio de factibilidad (FS) del yacimiento de cobre-oro-plata Alacran completado en diciembre de 2023 (adoptando el estándar NI 43-101), el contenido principal del diseño del proyecto es el siguiente: Escala de diseño: Este proyecto es un proyecto de minería y beneficio. La mina adopta minería a cielo abierto, con un mineral total dentro del límite del tajo diseñado de 97,9 millones de toneladas métricas. La mina produce mineral de óxido superficial y relaves previamente extraídos y almacenados (relaves antiguos), así como mineral mixto y mineral primario. Para las diferentes propiedades del mineral, se diseñan una planta de molienda-flotación y una planta de separación gravimétrica. La planta de molienda-flotación procesa principalmente mineral primario y mineral mixto, mientras que la planta de separación gravimétrica procesa mineral de óxido superficial y relaves antiguos. La planta de molienda-flotación tiene una capacidad de procesamiento diseñada de 17.600 tm/día, con productos finales de concentrados de cobre y concentrados de oro-plata; la planta de separación gravimétrica tiene una capacidad de procesamiento diseñada de 2.400 tm/día, con productos finales de concentrados de oro-plata. Se espera que el proyecto recupere acumulativamente 797 millones de libras de cobre, 550.000 onzas de oro y 5,35 millones de onzas de plata. Estimación de inversión: La estimación de inversión del proyecto es de 420,4 millones de dólares, destinados a la remoción de infraestructura de la mina a cielo abierto, sitio industrial minero, estación de trituración primaria de mineral bruto, acopio de mineral grueso, planta de molienda-flotación y planta de separación gravimétrica, sistema de espesamiento y filtración de concentrados, sistema de espesamiento y transporte de relaves, instalación de almacenamiento de relaves, caminos mineros, sistema de suministro de agua, subestación reductora principal, líneas de suministro eléctrico externo, caminos externos, campamento de oficinas y viviendas, instalaciones de tratamiento de aguas residuales, etc. Monto de inversión de la empresa: La empresa planea invertir aproximadamente 409,89 millones de dólares según una proporción de participación accionaria del 97,5%, un aumento de 178,67 millones de dólares sobre el monto previamente aprobado. Plan de construcción y vida útil: El período de construcción del proyecto es de 2 años, y la vida útil de la mina tras su finalización se estima en 14,2 años. Previsión de beneficios económicos: El valor presente neto (VPN) después de impuestos del proyecto es de 360 millones de dólares (tasa de descuento del 8%), la tasa interna de retorno (TIR) es del 23,8%, y el período de recuperación de la inversión se estima en 3 años. El cálculo de beneficios económicos se basa en precios del cobre de 3,99 USD/libra, precios del oro de 1.715 USD/onza y precios de la plata de 22,19 USD/onza. Para más detalles sobre el estudio de factibilidad (FS) del yacimiento de cobre-oro-plata Alacran, consulte el "Anuncio de Progreso de Jinchengxin sobre el Proyecto de Cobre-Oro-Plata San Matías" publicado por la empresa el 19 de diciembre de 2023.

Respecto al impacto de esta inversión en la empresa cotizada, Jinchengxin declaró: (1) Una vez que el proyecto entre en producción, se espera que tenga cierto impacto en el desarrollo comercial futuro y el rendimiento operativo de la empresa, lo cual es favorable para la mayor expansión de la empresa en el campo del desarrollo de recursos mineros, mejorando la estructura industrial de la empresa y promoviendo el desarrollo sostenido, estable y saludable de la empresa. (2) Esta inversión en la construcción posterior del proyecto minero de cobre-oro-plata Alacran según la proporción de participación accionaria está en línea con el plan de desarrollo a largo plazo de la empresa, es favorable para promover el desarrollo sostenido, estable y saludable de la empresa, y no perjudica los intereses de la empresa y los accionistas, especialmente los accionistas minoritarios.

Jinchengxin anunció en la noche del 17 de mayo que la Evaluación de Impacto Ambiental (EIA) de su mina de cobre-oro-plata Alacran en Colombia recibió recientemente la aprobación formal de la Autoridad Nacional de Licencias Ambientales (ANLA) de Colombia. La empresa implementará posteriormente todos los requisitos del permiso ambiental para garantizar la coexistencia armoniosa entre las operaciones del proyecto y las comunidades locales. Según el estudio de factibilidad completado en diciembre de 2023, el proyecto de la mina de cobre-oro-plata Alacran es un proyecto de minería a cielo abierto y beneficio con una inversión estimada de 420 millones de dólares, un mineral total dentro del límite del tajo diseñado de 97,9 millones de toneladas métricas, y una recuperación acumulada esperada de 797 millones de libras de cobre, 550.000 onzas de oro y 5,35 millones de onzas de plata. La empresa previamente revisó y aprobó una inversión de aproximadamente 231 millones de dólares basada en una participación esperada del 55% para construir el proyecto. Actualmente, la participación accionaria de la empresa en la mina de cobre-oro-plata Alacran ha aumentado al 97,5%, y la empresa seguirá los procedimientos de revisión correspondientes para la inversión en construcción del proyecto de acuerdo con los estatutos de la empresa y realizará las divulgaciones oportunas.

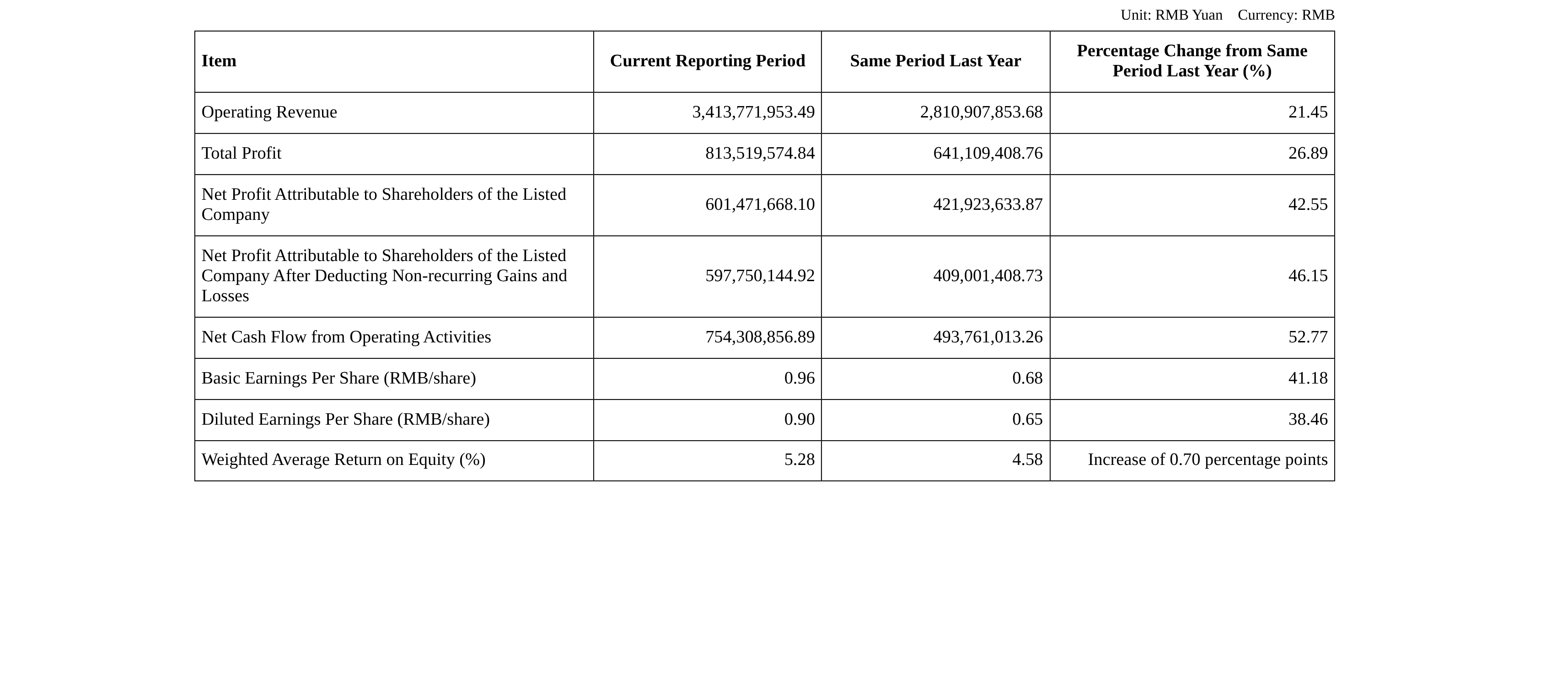

El informe del primer trimestre de 2026 de Jinchengxin divulgado el 28 de abril mostró: La empresa logró ingresos operativos totales de 3.414 millones de yuanes, un aumento interanual del 21,45%; el beneficio neto atribuible a la empresa matriz fue de 601 millones de yuanes, un aumento interanual del 42,55%.

Respecto a las razones del aumento en los ingresos operativos y el beneficio neto del primer trimestre, Jinchengxin anunció: Esto se debió principalmente al aumento de las ventas de productos de recursos minerales (cátodos de cobre, concentrados de cobre, mineral de hierro) y al alza de los precios de los productos de mineral de cobre durante el período.

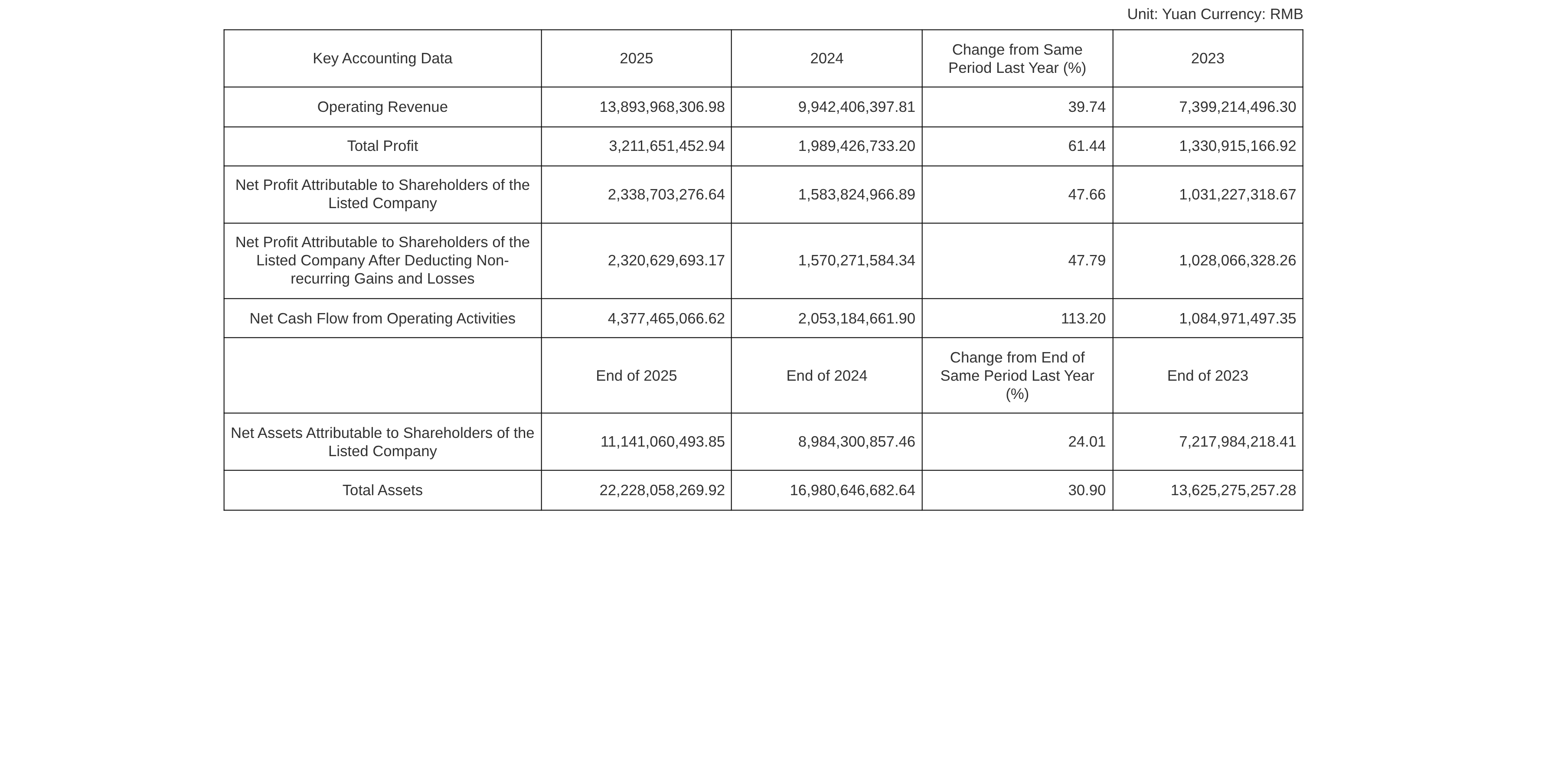

El informe anual 2025 de Jinchengxin mostró: La empresa logró ingresos de 13.894 millones de yuanes en 2025, un aumento interanual del 39,74%; el beneficio neto atribuible a la empresa matriz fue de 2.339 millones de yuanes, un aumento interanual del 47,66%.

Jinchengxin declaró en su informe anual 2025: Los ingresos operativos aumentaron un 39,74% interanual y el beneficio neto atribuible a los accionistas de la empresa cotizada aumentó un 47,66% interanual durante el período, principalmente debido al aumento de la producción y la eficiencia en los proyectos mineros propios del negocio de desarrollo de recursos minerales durante el período del informe.

Además, Jinchengxin declaró en la plataforma interactiva el 28 de abril que el inventario de productos de mineral de cobre de la empresa aumentó a finales del año 2025 y al cierre del primer trimestre de 2026, principalmente porque la temporada de lluvias local (noviembre-abril) afectó las condiciones viales y el transporte en las carreteras periféricas de la mina de cobre Dikulushi en la RDC, y los productos minerales producidos aún no se habían vendido externamente.

El comentario de China Post Securities sobre el informe de resultados de Jinchengxin indicó: El segmento de recursos registró un crecimiento impulsado por volumen, mientras que el negocio de servicios mineros se vio ligeramente afectado. Por segmento de negocio, el negocio de recursos mineros alcanzó ingresos/beneficio bruto de 6.986/3.121 mil millones de yuanes en 2025, con un aumento interanual del 117,67%/130,20%, mientras que el negocio de servicios mineros logró ingresos/beneficio bruto combinados de 6.613/1.515 mil millones de yuanes, con un aumento del 1,06%/descenso del 13,47% interanual. El negocio minero experimentó aumentos tanto en volumen como en precio, mientras que la caída en servicios mineros se debió principalmente a que la mina de cobre Lubambe fue convertida en unidad interna tras su adquisición, lo que resultó en menores ingresos y beneficio bruto reconocidos, y algunos proyectos se vieron afectados por la disminución de volúmenes de trabajo/ramp-up de producción. Volumen: Las ventas de cobre metálico en 2025 fueron de 92.700 toneladas, un aumento interanual del 88,16%; las ventas de mineral de fosfato fueron de 357.400 toneladas, una disminución interanual del 1,00%. El crecimiento en la producción y ventas de cobre metálico se debió principalmente a que la mina de cobre Lonshi alcanzó plena producción, las minas de cobre Dikulushi y Lonshi superaron los planes de producción, y la mina de cobre Lubambe fue consolidada durante todo el año. En el primer trimestre de 2026, la producción/ventas de cobre metálico fueron de 22.400/18.100 toneladas, afectadas principalmente por la disminución de la ley y la temporada de lluvias. Precio: Los precios del cobre subieron un 7,62% interanual en 2025 y un 36,72% interanual en el primer trimestre de 2026. Se espera que la producción crezca de manera constante en 2026, con un significativo potencial de expansión a largo plazo. En 2026, los proyectos de recursos propios de la empresa planean producir 100.300 toneladas de cobre metálico (equivalente) y vender 99.700 toneladas de cobre metálico (equivalente), y producir y vender 300.000 toneladas de mineral de fosfato; el proyecto de magnetita Yisitanxinshan planea producir y vender 1,25 millones de toneladas de concentrados de mineral de hierro. A más largo plazo, se espera que la zona minera norte de la mina de fosfato Liangchahe entre en funcionamiento a finales de 2028, con una capacidad anual que se expandirá de 300.000 a 800.000 toneladas; tras la puesta en producción de la zona este de la mina de cobre Lonshi, la producción anual podrá expandirse de 40.000 a 100.000 toneladas; la mina de cobre Lubambe está en proceso de transformación tecnológica, y tras su finalización se espera que produzca 35.000 toneladas de cobre anuales; la empresa posee una participación del 97,5% en la mina de cobre-oro-plata San Matías, que se encuentra en fase de aprobación de la evaluación de impacto ambiental. Advertencias de riesgo: riesgos de fluctuación de precios; avance del proyecto por debajo de las expectativas; demanda downstream por debajo de las expectativas; supuestos del modelo que no se ajustan a la realidad; riesgos de políticas que superan las expectativas, etc.