Summary

Between 2025 and 2026, copper policy across the Americas underwent a notable strategic shift, as the global copper industry increasingly moved away from a traditional resource-efficiency model toward a framework centered on supply chain security, industrial resilience, and strategic resource control.

The United States, Canada, and Chile progressively incorporated copper into their respective critical minerals strategies, materially elevating copper’s strategic role within national security, energy transition, and advanced manufacturing agendas. At the same time, major copper-producing countries such as Chile and Peru continued refining mining taxation regimes, permitting systems, domestic smelting policies, and export structures; while Mexico tightened mining concession oversight and further integrated into the North American critical minerals supply chain framework.

Overall, copper-related policy across the Americas have increasingly focused on the following areas:

- Strengthening critical minerals and supply chain security frameworks;

- Expanding domestic smelting, refining, and downstream processing capacity;

- Accelerating mine permitting and strategic copper project development;

- Promoting recycled copper and circular economy systems;

- Reinforcing ESG, environmental, and community governance requirements.

Against the backdrop of slowing global copper mine supply growth, the ongoing energy transition, and rapidly expanding demand from AI infrastructure and power grid investment, policy shifts across the Americas are expected to exert medium- to long-term influence on global copper mine supply, smelting dynamics, TC/RC trends, and regional copper trade flows.

The United States

The United States has upgraded Copper from a conventional industrial metal into a “national security + critical minerals” issue. The related policies include Section 232, the Critical Minerals Strategy, FAST-41 permitting acceleration, and DOE funding for copper processing and recycling.

Section 232 Investigation and Copper Tariff Policy

In February 2025, the United States launched a Section 232 investigation into copper imports, imposing a 50% tariff on semi-finished copper products and copper-intensive derivative products, effective August 1, 2025.

Under the final amendment implemented on April 6, 2026, copper-intensive derivative products became subject to a 25% tariff based on full product value. However, if importers can demonstrate that at least 95% of the copper, steel, or aluminum content in the final product is sourced and smelted domestically within the United States, the tariff may be reduced to 10%.

FAST-41

FAST-41 accelerates permitting for U.S. copper mines, smelters, and supporting infrastructure projects, supporting future North American copper supply growth. For large-scale copper mining projects included under FAST-41 (such as new greenfield copper projects in Arizona), the average Federal Environmental Impact Statement (EIS) and cross-agency permitting timeline can be shortened by approximately 45%, reducing the average approval period from around 4.5 years to roughly 2.5 years, significantly lowering the time cost associated with multi-billion-dollar upfront capital investments.

Copper – Critical Minerals Strategy

Copper was officially added to the U.S. critical minerals list. The list serves as a reference framework for federal investment, permitting, and supply chain policies, positioning copper as a key metal for national security and the energy transition, while reducing dependence on China and overseas copper processing supply chains.

Department of Energy (DOE) Critical Minerals Funding

The DOE announced plans to provide up to US$500 million in support for critical material processing, recycling, and manufacturing projects, explicitly including copper-related projects.

EPA Primary Copper Smelting NESHAP RTR

The National Emission Standards for Hazardous Air Pollutants (NESHAP) Risk and Technology Review (RTR) for Primary Copper Smelting targets residual risks and technical standards for major emission sources at primary copper smelters, affecting pyrometallurgical smelting systems such as Miami and Kennecott. The updated standards require the remaining primary pyrometallurgical smelters and emerging recycled copper smelting facilities in the United States to install the highest-level particulate capture systems. This significantly increases compliance and operating costs per tonne of copper production. Older facilities that fail to meet the new standards may face closure risks, potentially reducing domestic refined copper output.

Objectives of the U.S. Copper Policies

- Reducing dependence on overseas copper processing;

- Promoting Domestic Reshoring of Copper Smelting and Processing;

- Strengthening Critical Mineral Supply Chain Security;

- Improving stability of North American manufacturing supply chains;

- Restructuring global trade patterns.

Through Section 232, FAST-41, the Critical Minerals Strategy, DOE critical mineral funding, and EPA-driven upgrades to primary copper smelters, the United States aims to accelerate and strengthen development across the entire domestic copper value chain, including mining, smelting, refined copper, copper fabrication, and recycled copper.

Comprehensive Impact of U.S. Copper Policies

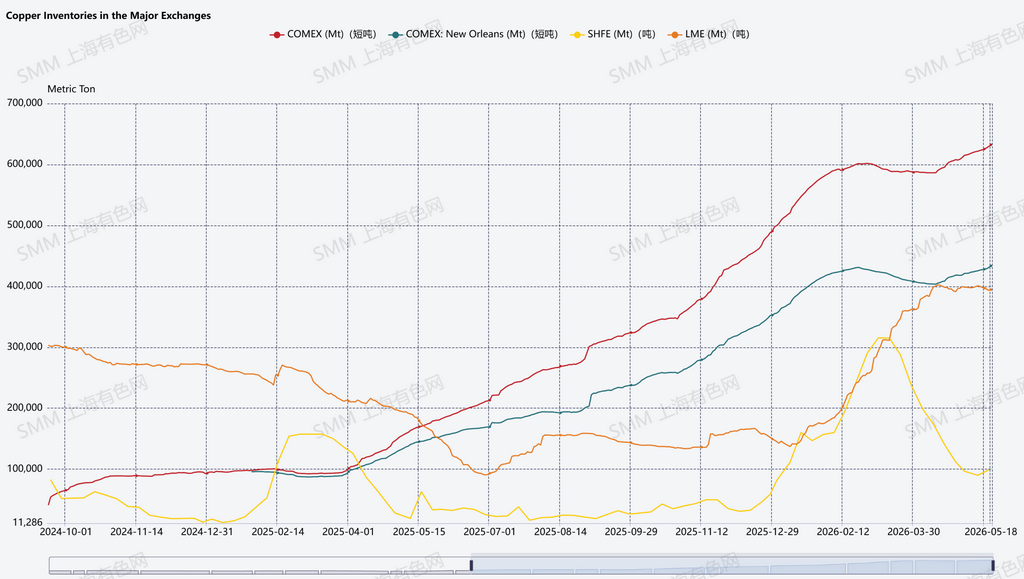

Global Copper Flows Shift Toward the United States; COMEX Inventories Continue Rising

Global copper inventory structures have undergone significant changes in recent years. As expectations for potential U.S. refined copper tariffs intensified, copper resources increasingly flowed into the U.S. COMEX system, while inventories in Asian LME warehouses declined sharply, leading to regional inventory reallocation.

Among the world’s three major exchange systems, COMEX inventories have risen steadily since 2025, while LME inventories experienced a significant decline during mid-2025. Meanwhile, SHFE inventories displayed periodic fluctuations influenced by post-Chinese New Year inventory accumulation and domestic demand cycles.

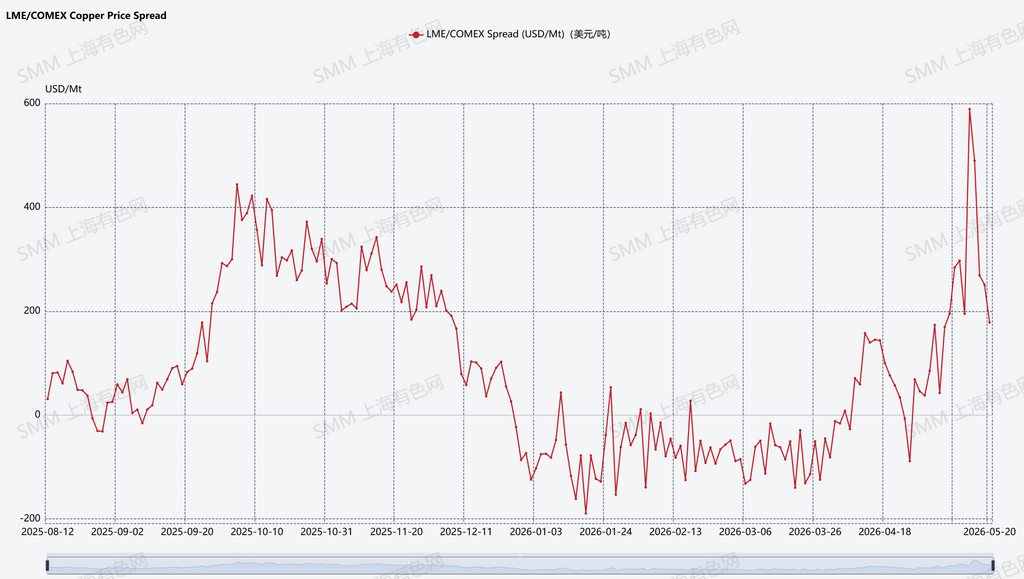

Intensifying Copper price fluctuations in the United States & Global copper resources are consistently flowing into North America.

Since 2025, volatility in the LME-COMEX copper spread has increased significantly. During Q4 2025, LME prices generally traded above COMEX. However, beginning in 2026, the LME-COMEX spread periodically turned negative, indicating that COMEX prices had started trading above LME prices and strengthening the U.S. regional premium structures.

Driven by the expectations of U.S. copper tariffs, the Section 232 investigation, and arbitrage trading activity, the COMEX inventories (particularly in New Orleans warehouses) accumulated rapidly, while inventories in Asian LME warehouses continued to decline. This reflected a clear flow of global copper resources into the United States, resulting in growing regional inventory imbalances.

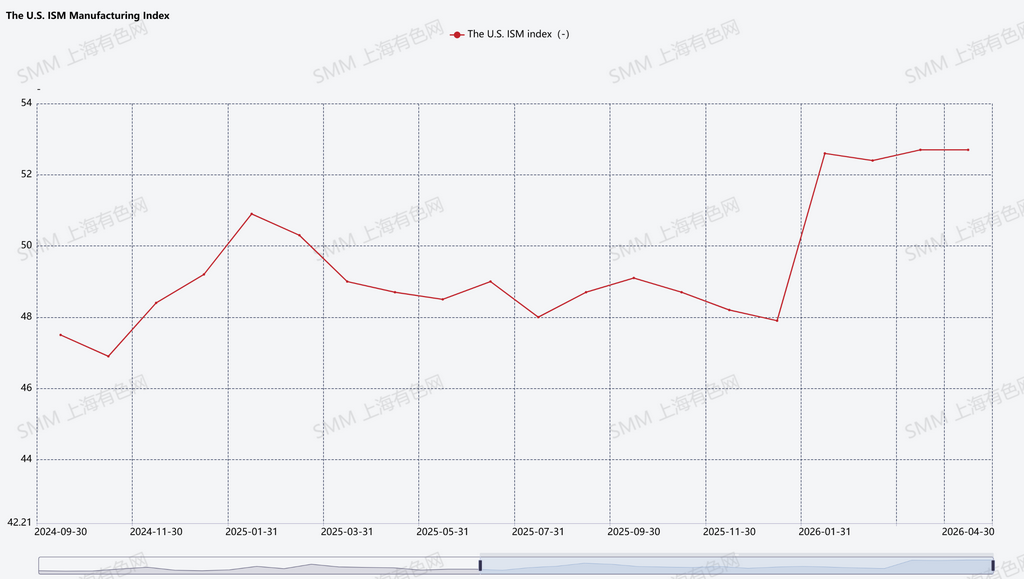

Manufacturing Recovery Supports North American Copper Demand Expectations

Since 2026, the U.S. ISM Manufacturing Index has remained in expansion territory, reflecting improving manufacturing activity. Driven by manufacturing reshoring, strengthened critical mineral security initiatives, domestic supply chain expansion, AI data center construction, power grid upgrades, and energy transition investment. The market is then expecting the industrial metals demand continued to be improved, reinforcing expectations for North American copper processing and manufacturing growth.

Impact on Copper Demand, Supply, and Prices

During 2025 to 2026, the U.S. copper-related policy gradually shifted from a traditional industrial metals framework toward a “critical minerals + supply chain security” model. Section 232 investigations, Critical mineral strategies, FAST-41 permitting acceleration, and DOE funding programs are all supporting domestic copper mining, copper processing, recycled copper, and manufacturing development within the United States.

On the demand side, manufacturing reshoring, AI data centers, power grid upgrades, and the energy transition continue to strengthen expectations for industrial copper demand. The recovery in the ISM Manufacturing Index also reflects improving U.S. industrial activity and stronger expectations for North American copper consumption.

On the supply side, under the combined influence of potential tariffs, arbitrage trading, and supply chain security strategies, global copper resources continue flowing into the United States. COMEX inventories have accumulated rapidly, while Asian LME warehouse inventories have continued declining, driving a broader regional reconfiguration of global copper inventories. Meanwhile, the United States is attempting to expand domestic refined copper, recycled copper, and copper fabrication capacity in order to reduce dependence on overseas refined copper and processing systems.

However, copper smelting and processing projects inherently involve long development cycles. From mining development and smelter construction to refined copper and fabrication projects, the process typically requires multiple stages including permitting, financing, environmental reviews, construction, and production ramp-up, often taking many years. The average timeline from copper discovery to commercial production now approaches 18 years globally, while smelting and processing projects generally require approximately 3 to 5 years from approval to startup, followed by an additional 1 to 3 years to achieve stable full-capacity operations. In addition, strict environmental regulations in the U.S. continue to constrain expansion of traditional pyrometallurgical smelting capacity. As a result, the U.S. dependence on imported refined copper is unlikely to change significantly in the short term.

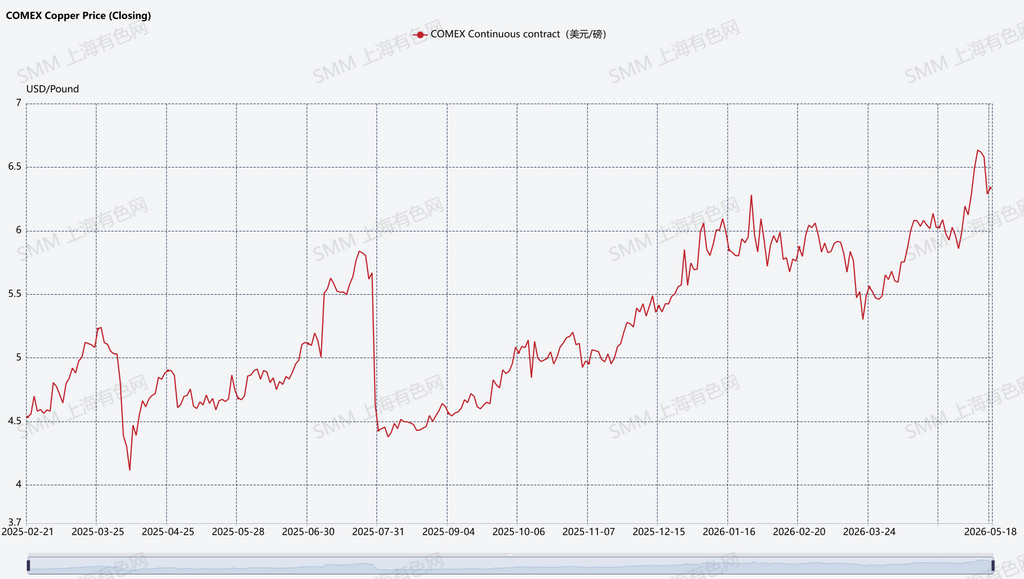

From a pricing perspective, the U.S. copper policies and tariff expectations have significantly increased volatility in the global copper market. The concerns of the rising future costs for refined copper entering the U.S. had pushed COMEX copper prices above LME prices periodically, leading to a sharp widening in the LME-COMEX spread.

As the U.S. regional premiums increased, arbitrage windows opened and encouraged global traders to redirect copper resources into the U.S. and further accelerated COMEX inventory accumulation.

Overall, current volatility in copper prices, widening regional spreads, and shifts in inventory structures fundamentally are generally affected by the U.S. policy expectations and ongoing supply chain restructuring. Over the medium to long term, global energy transition investment, AI infrastructure development, and competition for critical minerals are expected to continue supporting copper demand growth. However, policy uncertainty and regional supply chain adjustments are also likely to sustain elevated copper price volatility and regional price differentials.