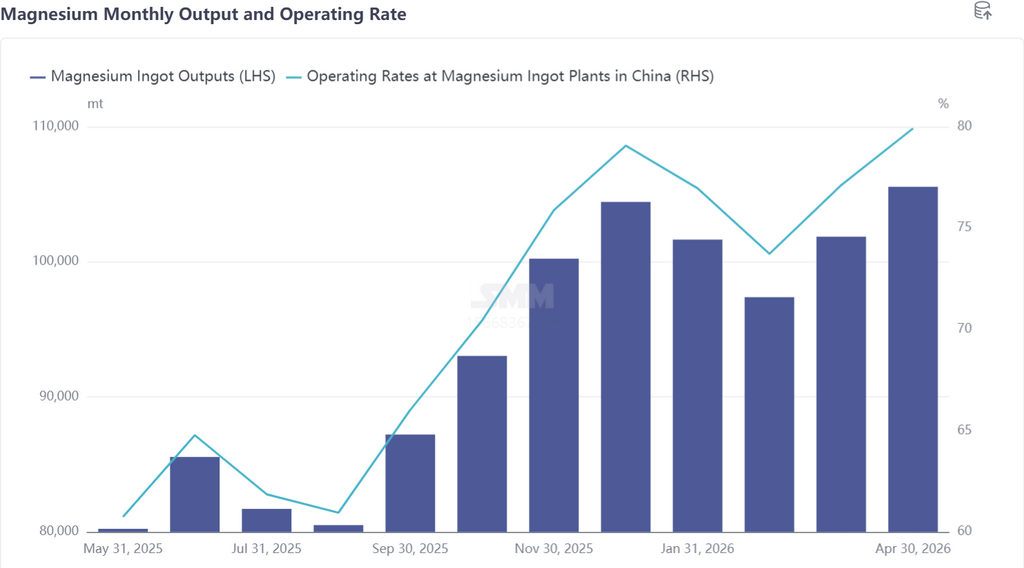

Primary magnesium production rose 3.63% MoM in April. April domestic primary magnesium production increased notably, mainly because magnesium prices rose steadily from late March and market conditions continued to recover. Rising magnesium prices drove profit restoration at smelters, prompting previously idled or low-load enterprises to resume production under profit incentives, while operating enterprises simultaneously raised their operating loads. Industry operating rates continued to climb, with enterprises collectively ramping up and resuming production, pushing April primary magnesium production to grow steadily.

By province, most primary magnesium smelters maintained stable production in April, while some increased output. Provinces with rising primary magnesium production in April were mainly Shaanxi and Xinjiang. Specifically, primary magnesium smelters in the main producing areas saw production increases, with Shaanxi's share of primary magnesium edging up slightly as two primary magnesium smelters resumed production and most operated at full capacity. In April, one primary magnesium smelter in Xinjiang gradually commissioned new capacity, and Xinjiang's share of primary magnesium production edged up.

Looking ahead to May, current magnesium prices are approaching the cost lines of primary magnesium smelters in the main producing areas. Some producers plan to halt production for maintenance in May, and primary magnesium production is expected to edge down slightly in May.

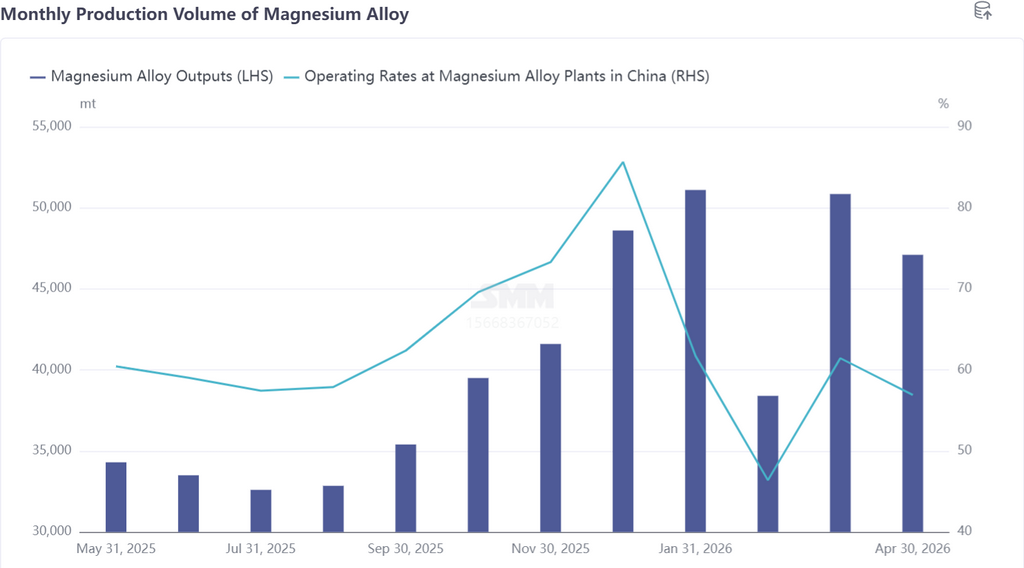

In April 2026, magnesium alloy production decreased 7.18% MoM. This round of decline in magnesium alloy production was caused by multiple factors on both the supply and demand sides: affected by the continued decline in magnesium ingot prices, the sentiment of rushing to buy amid continuous price rise and holding back amid price downturn spread among downstream players, with die-casting enterprises showing weak order willingness. This was compounded by the cancellation of some magnesium alloy orders by the two-wheeler industry, triggering a chain reaction that further pressured midstream processing orders. Meanwhile, after a fire incident at a die-casting plant, regional environmental protection supervision tightened, constraining production. Multiple factors dragged down magnesium alloy orders. Supply side, some alloy enterprises entered routine maintenance cycles, leading to phased production cuts, and production performance remained weak under multiple pressures. Magnesium alloy production is expected to continue its upward trend in May. Supply side, according to SMM, multiple magnesium alloy smelters raised their operating rates, and some magnesium alloy production lines at smelters that were under maintenance in April resumed production. A newly built magnesium alloy smelter was completed and put into operation, with magnesium alloy supply rising steadily. Demand side, die-casting equipment is being installed successively, and current magnesium alloy die-casting capacity is rising steadily. Moreover, stricter enforcement of the new national standard for two-wheelers may transmit policy-driven momentum upstream to drive a recovery in magnesium alloy orders. Overall, the magnesium alloy market is expected to see robust supply and demand in May, with magnesium alloy production growing steadily.

In early to mid-May, operating rates of China's primary magnesium smelters stayed high, with operating rates in major producing areas rising above 80%. Spot supply of magnesium ingots in the market was ample, and overall inventory pressure on smelters was relatively high. After the Labour Day holiday, some magnesium plants urgently needed to collect payments to pay electricity bills, distribute employee wages, and maintain daily operations, proactively offering price concessions to stimulate transactions. However, supported by raw material and production costs, the room for price adjustments by magnesium plants was limited, and the magnesium ingot price range remained at 16,000-16,500 yuan/mt in early to mid-May.

In mid to late May, after a prolonged gradual decline in magnesium prices in the earlier period, magnesium prices bottomed out driven by concentrated downstream restocking, but the overall rebound height was limited. Current market supply pressure is relatively high, and magnesium prices lack unilateral upward momentum. Meanwhile, from the perspective of costs and the supply-demand pattern, downside room for magnesium prices has also narrowed. On one hand, primary magnesium smelters are already approaching the break-even line and can hardly withstand significant deep price drops. On the other hand, current temperatures already meet the conditions for magnesium plants to halt production for maintenance. If prices continue to decline further, smelters may collectively halt production for maintenance to contract supply, ease market inventory pressure, and further support magnesium prices.