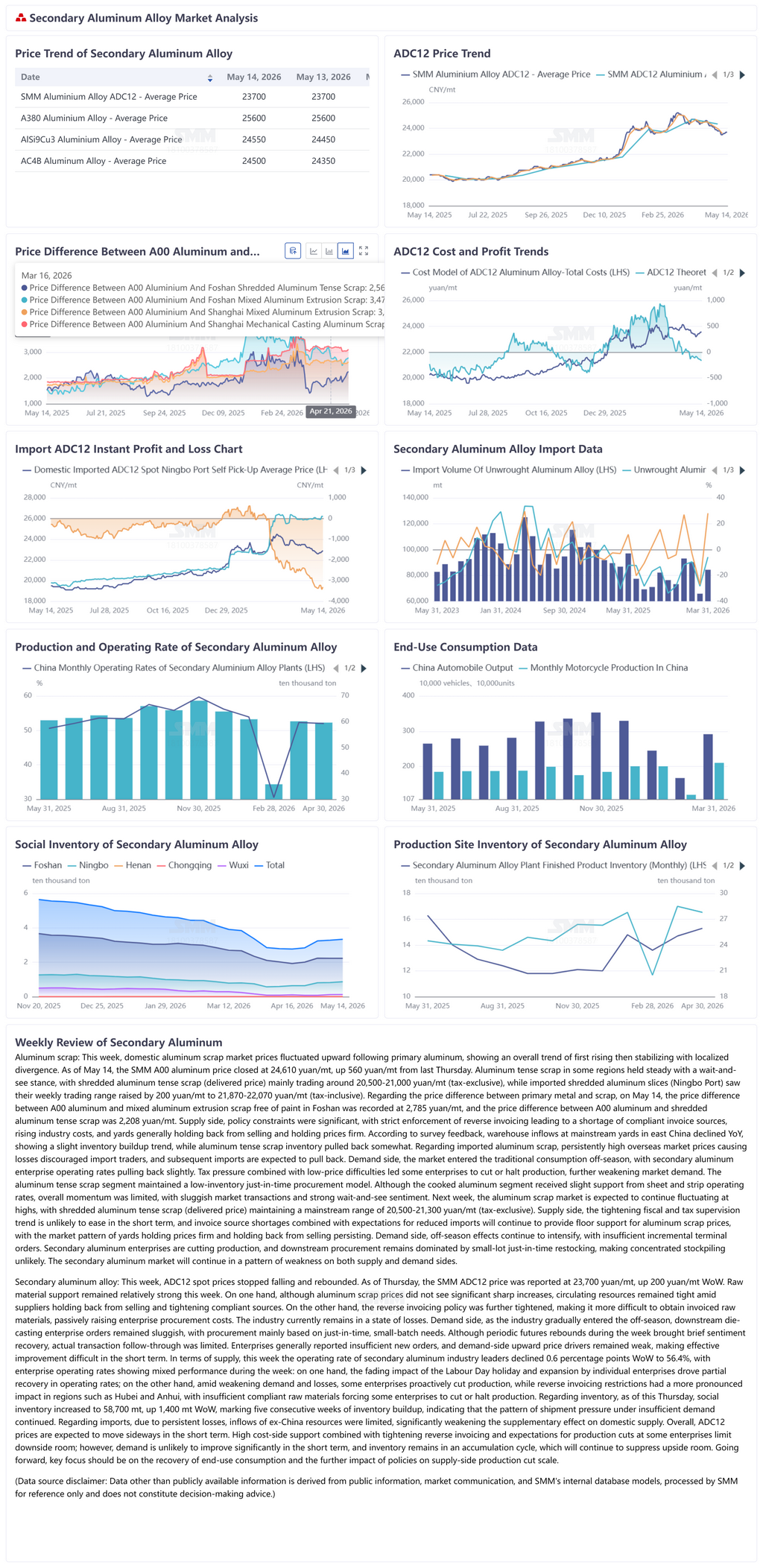

Aluminum scrap: This week, China's aluminum scrap market prices fluctuated upward following primary aluminum, overall showing a pattern of first rising then stabilizing, with localized divergence. As of May 14, SMM A00 aluminum closed at 24,610 yuan/mt, up 560 yuan/mt WoW from Thursday. Aluminum tense scrap in some regions held steady with a wait-and-see stance. Shredded aluminum tense scrap (delivered price) traded in a mainstream range of 20,500-21,000 yuan/mt (tax-exclusive), while imported shredded aluminum slices (Ningbo Port) saw their weekly trading range raised by 200 yuan/mt to 21,870-22,070 yuan/mt (tax-inclusive). On the price difference between primary metal and scrap, on May 14, the price difference between A00 aluminum and mixed aluminum extrusion scrap free of paint in Foshan was recorded at 2,785 yuan/mt, and the price difference between A00 aluminum and shredded aluminum tense scrap was 2,208 yuan/mt. Supply side, policy constraints were significant, as strict enforcement of reverse invoicing led to a shortage of compliant invoice sources, pushing up industry costs, with stockyards generally holding back from selling and holding prices firm. According to survey feedback, warehouse inflows at mainstream stockyards in east China declined YoY, showing a slight inventory buildup trend, while aluminum tense scrap inventory pulled back somewhat. On imported aluminum scrap, persistently high overseas market prices creating an inverted spread made import traders more cautious, and subsequent imports are expected to pull back. Demand side, the market entered the traditional consumption off-season. Secondary aluminum enterprises saw operating rates pull back slightly. Tax pressure combined with low-price difficulties caused some enterprises to cut production or halt operations, further weakening market demand. Aluminum tense scrap maintained a low-inventory just-in-time procurement model. Although cooked aluminum was slightly supported by sheet and strip operating rates, overall momentum was limited, with sluggish market transactions and strong wait-and-see sentiment. Next week, the aluminum scrap market is expected to continue fluctuating at highs, with shredded aluminum tense scrap (delivered price) maintaining a mainstream range of 20,500-21,300 yuan/mt (tax-exclusive). Supply side, the tightening fiscal and tax supervision trend is unlikely to ease in the short term, and invoice source shortages combined with expectations of reduced imports will continue to provide floor support for aluminum scrap prices, with the market pattern of stockyards holding prices firm and holding back from selling persisting. Demand side, off-season effects will continue to intensify, with insufficient incremental end-user orders. Secondary aluminum enterprises are trending toward production cuts, and downstream procurement will remain dominated by small-order just-in-time restocking, making concentrated stockpiling unlikely. The secondary aluminum market will continue its pattern of weak supply and demand.

Secondary aluminum alloy: ADC12 spot prices stopped falling and rebounded this week. As of Thursday, the SMM ADC12 price was quoted at 23,700 yuan/mt, up 200 yuan/mt WoW. Raw material support remained relatively strong this week. On one hand, although aluminum scrap prices did not see significant increases, circulating resources remained tight amid suppliers holding back from selling and tightening of compliant sources. On the other hand, the reverse invoicing policy was further tightened, making it more difficult to obtain invoiced raw materials, passively pushing up enterprise procurement costs. The industry remained in a state of cost-driven losses. Demand side, as the industry gradually entered the off-season, downstream die-casting enterprises continued to see sluggish orders, with procurement mainly driven by rigid demand in small batches. Although the periodic rebound in futures during the week brought brief sentiment recovery, actual transaction follow-through was limited. Enterprises generally reported insufficient new orders, and demand-side upward price drivers remained weak, making effective improvement difficult in the short term. In terms of supply, the operating rate of secondary aluminum industry leaders declined 0.6 percentage points WoW to 56.4% this week, with enterprise operations showing mixed performance: on one hand, the fading impact of the Labour Day holiday and capacity expansion by individual enterprises drove partial recovery in operations; on the other hand, amid weakening demand and losses, some enterprises proactively cut production, while restrictions on reverse invoicing had a more pronounced impact in regions such as Hubei and Anhui, with insufficient compliant raw materials forcing some enterprises to reduce or halt production. Inventory side, as of Thursday, social inventory increased to 58,700 mt, up 1,400 mt WoW, marking five consecutive weeks of inventory buildup, indicating continued pressure on shipments amid insufficient demand. Import side, due to persistent losses, inflows of ex-China resources remained limited, significantly weakening their supplementary role in China's supply. Overall, ADC12 prices are expected to move sideways in the short term. Cost side, elevated support combined with tightening of reverse invoicing and expectations for production cuts at some enterprises limit downside room; however, demand is unlikely to improve significantly in the short term, and inventory remains in an accumulation cycle, which will continue to suppress upside room. Going forward, the key focus will be on the recovery of end-use consumption and the further impact of policies on the scale of production cuts on the supply side.

![Raw Material Divergence Keeps Costs Elevated, Aluminum Fluoride Sees Low Operating Rates and Stagnant Prices in a Stalemate SMM May 14 News: [SMM Fluoride Salts Weekly Review]](https://imgqn.smm.cn/usercenter/wvGIW20251217171655.jpg)

![[SMM Aluminum News] LME Inventory Down 0.65% to 346,500 mt on May 14, Drops 12.49% Over a Month](https://imgqn.smm.cn/usercenter/uoPaX20251217171651.jpg)