El 12 de mayo de 2026, la vicepresidenta de SMM, Wang Cong (Shirley Wang), asistió a la Conferencia Anual del Cobalt Institute celebrada en Madrid, España. En esta conferencia anual del Cobalt Institute, SMM y el Cobalt Institute organizaron conjuntamente un subforo titulado «El panorama ESG de China: perspectivas prácticas para la cadena de valor del cobalto». SMM pronunció un discurso inaugural sobre la situación actual y las perspectivas del mercado chino de cobalto, compartiendo análisis sobre el patrón de oferta y demanda y las tendencias de precios del mercado chino de cobalto, con un análisis sistemático desde tres dimensiones: cambios en la estructura de la oferta, perspectivas de producción y demanda de uso final.

Como miembro del Cobalt Institute, SMM siempre se ha comprometido a colaborar con organizaciones internacionales de la industria del cobalto, empresas y organismos de normalización para construir una cadena de valor y un sistema de información de mercado del cobalto más eficiente e integral. Como uno de los mayores proveedores de servicios de información sobre metales no ferrosos de China, SMM ha aprovechado plenamente sus ventajas globales para establecer un sistema de información de valor de ecosistema completo centrado en China, que abarca la minería upstream (RDC + Indonesia), el procesamiento midstream, los materiales para baterías y el comercio downstream, la fabricación de celdas y baterías, y las aplicaciones terminales de nuevas energías y electrónica de consumo. SMM ha participado en la conferencia del Cobalt Institute y pronunciado discursos principales durante tres años consecutivos.

I. Análisis de la oferta del mercado

1.1 Oferta total de China y cambios en la estructura de materias primas

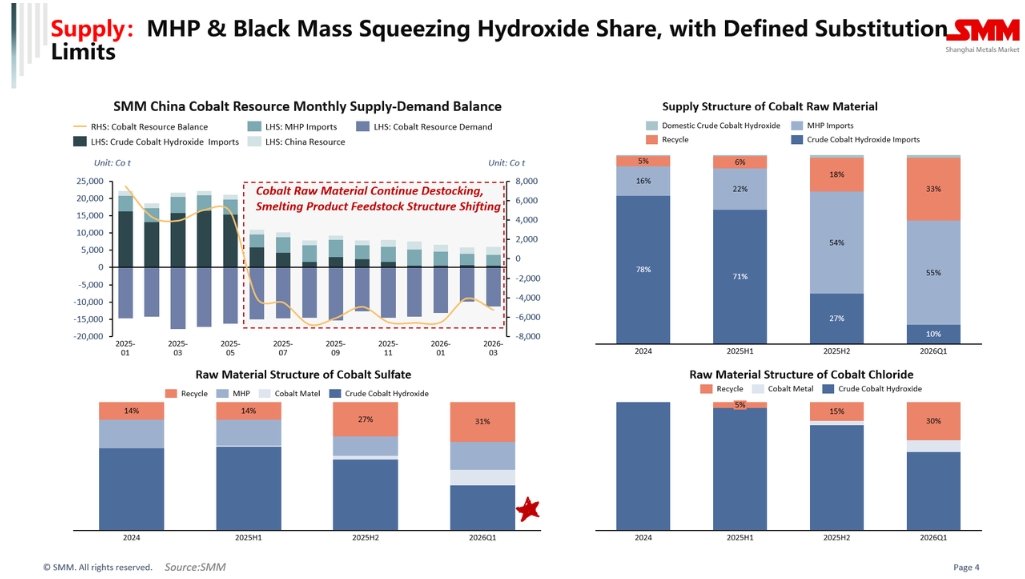

Desde el segundo trimestre del año pasado, la oferta efectiva de hidróxido de cobalto crudo ha disminuido significativamente. A corto plazo, el MHP, la masa negra y otras materias primas están desplazando la cuota de mercado del hidróxido de cobalto, una tendencia que merece atención continua.

En cuanto a la estructura de materias primas de los productos de cobalto, en el primer trimestre de este año, el hidróxido de cobalto representó solo aproximadamente el 10 % de la estructura de materias primas, las importaciones de MHP aumentaron a más del 15 %, y las materias primas recicladas ascendieron a más del 30 %. Entre ellas, en la composición de materias primas del sulfato de cobalto, la proporción de materias primas recicladas aumentó significativamente, con los productos intermedios de cobalto cayendo a menos del 40 %, y la masa negra con alto contenido de cobalto alcanzando el 30 %. Este cambio estructural refleja un profundo ajuste en curso en el suministro de materias primas de cobalto de China.

1.2 Perspectiva de producción

La producción de productos de cobalto reciclado de China fue de aproximadamente 24.000 t en 2025, y se espera que se acerque a 30.000 t en 2026, con una tendencia a medio y largo plazo de incremento gradual.

En cuanto al suministro de MHP, la producción de este mes se vio afectada en cierta medida por la escasez de azufre a corto plazo, pero a largo plazo, se espera que el suministro de cobalto procedente de MHP continúe aumentando.

II. Análisis de la demanda de uso final

2.1 Mercado de vehículos de nueva energía (NEV)

La cuota de mercado de los materiales ternarios continuó siendo erosionada por el LFP, limitando el crecimiento general. Mientras tanto, afectado por los altos precios del cobalto y la oferta ajustada, el consumo de cobalto por tonelada de precursor disminuyó. En el primer trimestre de este año, el consumo ponderado de cobalto por tonelada de precursor cayó por debajo de 0,06 t en contenido metálico. No obstante, la demanda total de cobalto del mercado de NEV continuó creciendo, pero la tasa de crecimiento fue inferior a la prevista anteriormente.

2.2 Mercado de productos 3C

El mercado de productos 3C también enfrentó una presión significativa. Desde finales del año pasado, el fuerte aumento de los precios de los chips impulsó al alza los precios de los productos 3C. Además, para hacer frente a la presión de costes, algunas empresas redujeron el uso de cobalto en los materiales catódicos mediante la mezcla con NCM, y se espera que la demanda de cobalto para aplicaciones 3C disminuya este año.Sin embargo, a medio y largo plazo, la demanda de cobalto de los productos 3C aún tiene margen de crecimiento.

III. Tendencias y perspectivas de precios

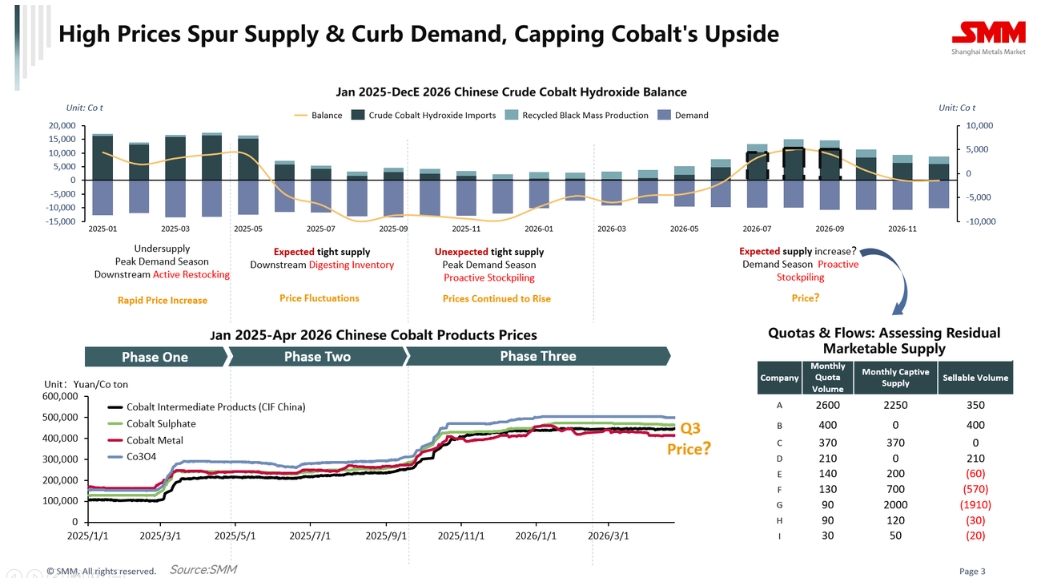

En cuanto a las tendencias de precios del cobalto, aunque los cálculos teóricos sugieren que en el segundo y tercer trimestre de 2026, las llegadas concentradas de productos intermedios de cobalto previamente acumulados a los puertos harán que el balance de oferta y demanda de materias primas de cobalto cambie temporalmente a un estado de acumulación de inventarios, ejerciendo presión a la baja sobre los precios del cobalto, la cantidad limitada de productos intermedios de cobalto disponibles en el mercado, restringida por los niveles de inventario y el ritmo de ventas del mercado, proporcionará un fuerte soporte a los precios del cobalto. Se espera que los precios suban ligeramente en los próximos meses, pero existe un claro techo al alza.

También señaló que los niveles de inventario de materias primas, el suministro de otras materias primas (como MHP y cobalto refinado), y el ritmo de envío de productos intermedios de cobalto son las mayores incertidumbres que afectan la tendencia de los precios.