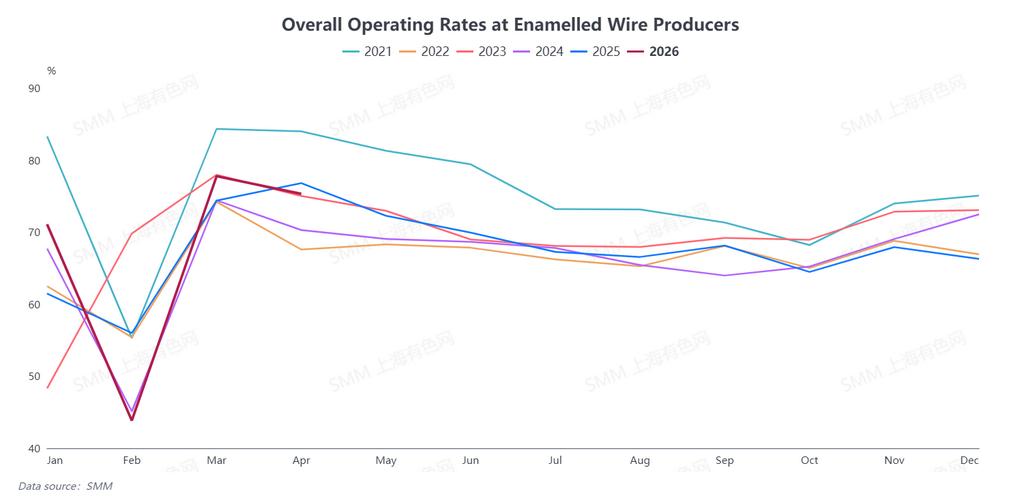

Según SMM, la tasa de operación integral de la industria de alambre esmaltado en abril fue del 75,31%, una caída de 2,44 puntos porcentuales intermensual y de 1,48 puntos porcentuales interanual. En concreto, la tasa de operación de las grandes empresas fue del 80,19%, la de las medianas del 62,86% y la de las pequeñas del 71,53%.

En abril, la tasa de operación del sector cayó tanto intermensual como interanualmente, afectada por múltiples factores, entre ellos la disminución de la demanda de electrodomésticos por parte de los usuarios finales, el agotamiento de la demanda de aprovisionamiento posterior debido a pedidos concentrados anticipados y los precios del cobre bajo presión en niveles elevados. En cuanto a la demanda, se observó una clara divergencia estructural: la demanda del sector de nuevas energías y electricidad se mantuvo sólida, proporcionando un fuerte respaldo a la industria, mientras que la demanda del sector de electrodomésticos cayó por encima de las expectativas, lastrando significativamente las operaciones del sector. Además, los bajos precios del cobre en marzo estimularon una liberación concentrada de pedidos, agotando prematuramente la demanda de almacenamiento posterior. Los altos precios del cobre en abril frenaron aún más el crecimiento de nuevos pedidos. La demanda en motores industriales tradicionales, vehículos de dos ruedas y otros sectores también mostró un desempeño mediocre, con un debilitamiento del sentimiento del sector.

En cuanto a inventarios, las empresas de alambre esmaltado acumularon inventarios de producto terminado antes del feriado del Día del Trabajo, pero la disposición de los compradores aguas abajo para retirar mercancía fue débil y el ritmo de envíos tras el feriado se desaceleró, elevando los días de inventario de producto terminado del sector a 10,79 días, con niveles de inventario generales ligeramente al alza.

SMM prevé que la tasa de operación de la industria de alambre esmaltado en mayo sea del 72,04%, una caída de 3,27 puntos porcentuales intermensual y de 0,21 puntos porcentuales interanual. Al entrar en mayo, los pedidos de la industria de alambre esmaltado mostraron una tendencia a la baja. Según SMM, aunque la demanda del sector eléctrico y de nuevas energías se mantuvo positiva, el desempeño del segmento de electrodomésticos continuó en declive, con empresas relacionadas reportando pedidos con caídas superiores al 20% interanual y viéndose obligadas a iniciar recortes de producción y estrategias de reducción de inventarios. Además, la industria de alambre esmaltado entrará en la temporada baja tradicional a finales de mayo. Sumado a las interrupciones de producción por el feriado del Día del Trabajo, múltiples factores arrastran conjuntamente la tasa de operación del sector a continuar su retroceso.

![El mercado de cobre blíster sigue ajustado; se espera que los cargos de refinación en China se mantengan estables en junio [Análisis SMM]](https://imgqn.smm.cn/usercenter/jlrsy20251217171711.jpg)

![Inventario social de cobre en las principales regiones de China se mantiene estable respecto a la semana anterior [Datos semanales de SMM]](https://imgqn.smm.cn/usercenter/GfvuY20251217171708.jpg)