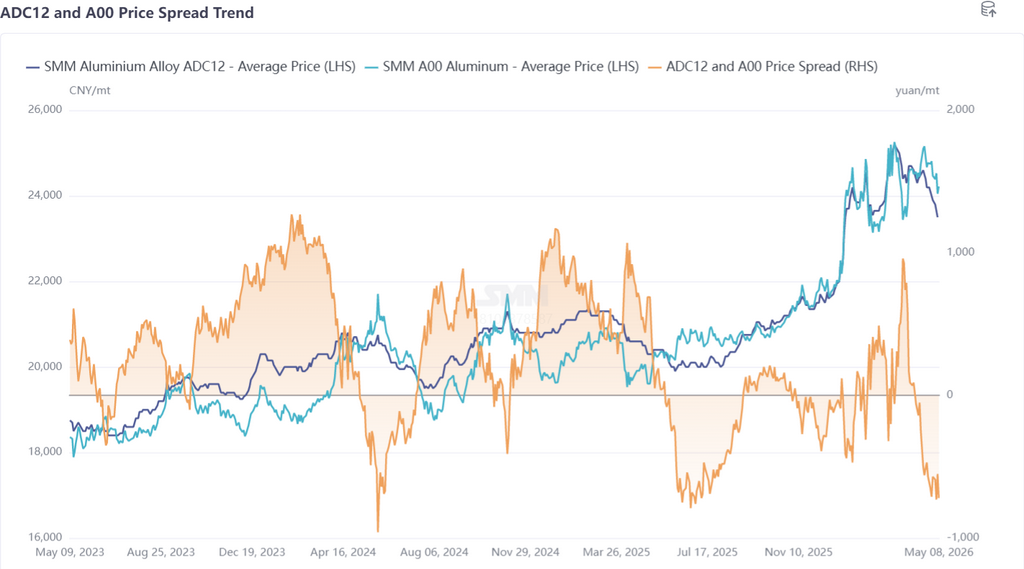

First, a review of secondary aluminum alloy price trends in April: On the futures side, the most-traded cast aluminum alloy contract first declined then rose in April, reaching a high of 24,250 yuan/mt, before turning into a continuous downward trend after mid-month. After May, the decline narrowed, and the contract was in the doldrums near 23,000 yuan/mt. On the spot side, ADC12 prices were overall under pressure in April, with upward momentum fading at the beginning of the month and the decline widening after mid-month. As of May 8, SMM ADC12 was quoted at 23,500 yuan/mt, a cumulative drop of 1,200 yuan/mt from early April.

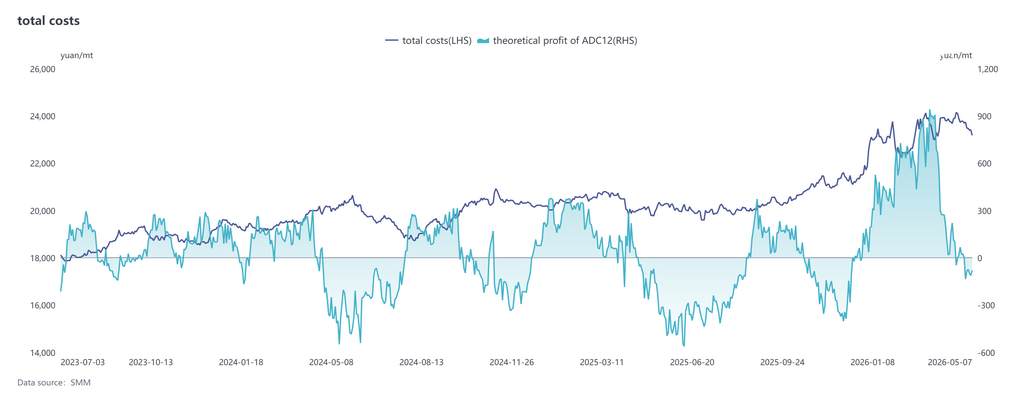

Cost side, according to the latest SMM data, the theoretical total cost of the ADC12 industry rose to 23,787 yuan/mt in April, edging up MoM from March, but the increase narrowed compared to the previous month. In terms of cost composition, aluminum scrap remained the dominant cost item, with per-mt cost rising to 21,569 yuan, and its share edging up slightly to 90.7%; copper cost increased marginally to 835 yuan/mt, with its share unchanged at 3.5%; silicon cost pulled back slightly to 478 yuan/mt, with its share shrinking to 2.0%. After entering May, ADC12 prices continued to decline, while aluminum scrap prices pulled back only marginally. The industry's theoretical profit shifted from gain to loss, and enterprise operational pressure became more pronounced.

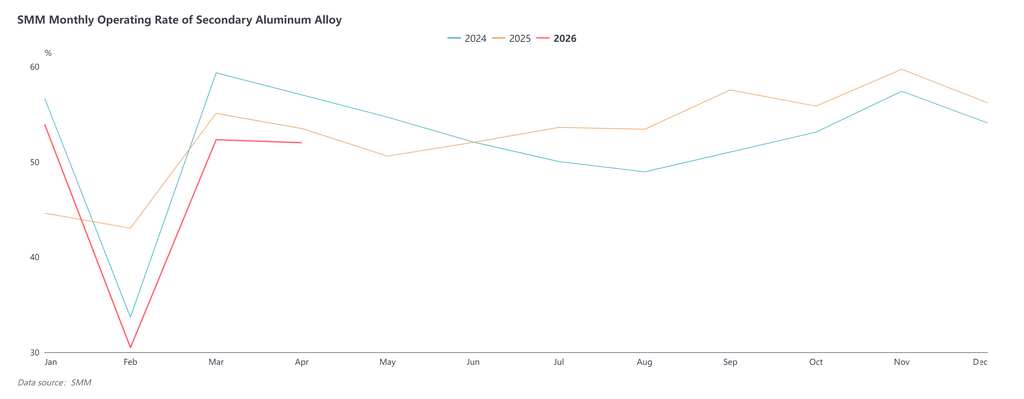

In April, the operating rate of the secondary aluminum alloy industry was 52.0%, edging down 0.3 percentage points MoM and declining 1.5 percentage points YoY, with notable divergence among enterprises. The relatively stable operating rate was mainly attributable to: ADC12 price declines stimulating a partial return of orders; improved export profits offsetting domestic volume reductions; and traders purchasing at low prices to fill part of the order gap. However, production cuts were also widespread, primarily due to consumption falling short of expectations, difficulties in procuring compliant raw materials, and restrictions on reverse invoicing, which forced some enterprises to passively reduce output. Overall, the operating rate in April edged down within a narrow range. In May, demand continued the weakening trend that began in mid-April, with downstream restocking willingness remaining weak and wait-and-see sentiment dominating. Reduced orders during the Labour Day holiday weighed on production, and post-holiday recovery room was limited. Under multiple pressures including the demand off-season, raw material issues, and invoicing problems, the operating rate in May still has room for further decline.

Overall, ADC12 prices in May are expected to continue in a narrow-range doldrums pattern, but downside room is relatively limited. On the pressure side, end-use demand remained persistently weak, social inventory and in-factory inventory stayed high, fundamentals lacked substantive positive drivers, and price rise momentum was insufficient. On the support side, persistently high raw material costs such as aluminum scrap, combined with reduced aluminum scrap imports, provided certain floor support for spot prices, and enterprises had limited willingness to significantly cut prices. In summary, ADC12 prices in May are expected to mainly fluctuate downward within a narrow range. Going forward, key attention should be paid to the transmission impact of Middle East geopolitical conflicts on aluminum prices, marginal changes in end-use demand, and aluminum scrap supply conditions.