This insight follows panel discussions at SMM’s London H1 2026 seminar, where one theme stood out clearly: funds are trumping fundamentals in today’s copper market.

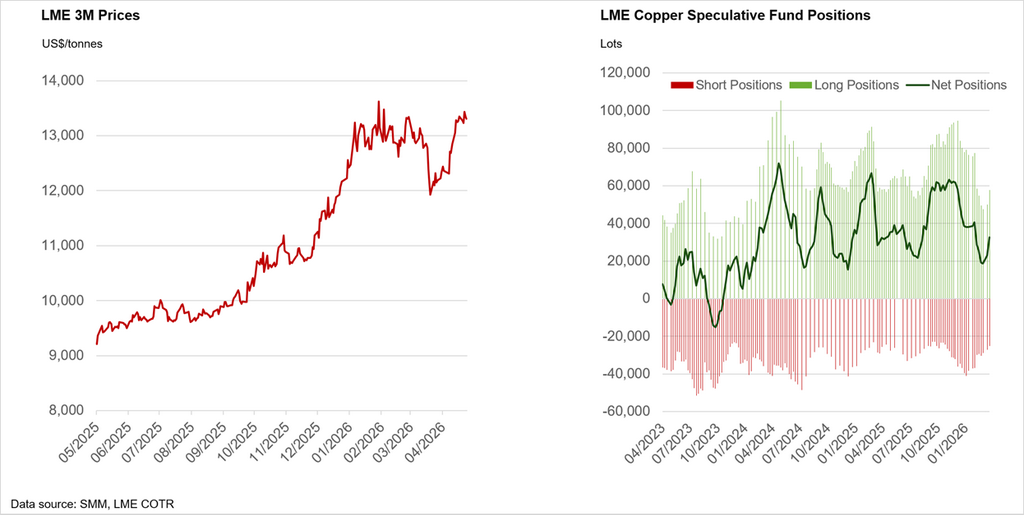

At first glance, the setup looks contradictory. There is no clear physical shortage of copper: near-term time spreads are in contango, signalling adequate supply; SMM forecasts a small global refined surplus in 2026; global exchange stocks are rising. On traditional metrics, prices should be softer. Yet LME copper remains elevated at around $13,000/t. This leads us to believe that copper is no longer trading purely on market fundamentals.

So What Is Driving Copper Higher?

- Financial flows dominate price formation

Speculative inflows since the middle of last year have played a key role in pushing copper higher. The recent rally following the initial shock of the US-Iran war is no exception. While some capital has rotated into energy markets recently, inflows into copper and broader commodities have remained resilient, supported by macro funds and systematic positioning. Momentum-driven strategies (CTAs, macro funds) have reinforced upside moves, especially during periods of positive price signals and cross-asset risk appetite. This can be seen from the bottom right hand-side chart which shows speculative positions from the LME’s Commitment of Traders Report (COTR).

There has also been selective physical support, particularly from China, where downstream buying and restocking have contributed to declining local inventories at times. However, this physical demand has been opportunistic rather than structural, and insufficient on its own to explain the persistence of elevated prices.

Overall, barring the initial geopolitical shock, copper price strength has been largely investor-led rather than consumer-led, with financial capital remaining the dominant marginal driver of price formation.

-

A persistent geopolitical premium

Supply risks remain elevated across key producing regions; energy and input cost volatility (e.g. sulphuric acid and diesel) adds uncertainty to production; trade fragmentation and resource nationalism are reshaping supply chains; copper is increasingly priced as a strategic resource, not just a commodity.

-

Policy distortions — particularly from the US

Tariff expectations and US government policy aimed at securing domestic supply chains — including potential import tariffs on copper, incentives for local processing, and broader reshoring of manufacturing — have triggered regional stockpiling. This has tightened availability ex-US and distorted global trade flows, as material is increasingly drawn into the US market. In effect, policy is creating artificial tightness in specific regions, even as the global market remains broadly balanced.

-

Structural narrative outweighs current balance

Electrification, grid expansion, and AI infrastructure continue to anchor long-term demand; supply constraints (declining ore grades, permitting delays) remain unresolved. As such, the market is pricing future deficits today, not current surplus.

Why Surplus Does Not Equal Lower Prices

The key misunderstanding in today’s market is treating copper like a static balance sheet. The surplus is marginal and unevenly distributed. Inventories are not necessarily located where demand is strongest. The market reacts to marginal tightness and risk, not annual average. Most importantly, copper is a forward-looking asset — it prices sentiment and expectations, not just spot fundamentals.

How Traders Think About Copper Now

Copper price formation has evolved into a multi‑layered system according to our panellists:

Price = Fundamentals + Financial Flows + Macro + Narrative

By this, we mean that copper prices are driven by four interacting components — Fundamentals, Financial Flows, Macro, and Narrative — and traders now analyse each layer in more depth to anticipate price direction. They:

- Watch financial conditions — positioning, flows, momentum, correlations

Traders look at who holds risk, how strong the flows are, and whether momentum is building or fading. Cross‑asset signals — especially from US equities and major commodity indices — show whether copper is trading as part of a broader risk‑on move or reacting to something more specific.

-

Track macro drivers — interest rates, policy, USD, liquidity

Copper reacts quickly to shifts in US real yields, Fed expectations, and the strength of the dollar. Easier financial conditions or a weaker USD can lift prices even when demand is soft. Global liquidity trends, including China’s credit cycle, influence how much speculative capital enters the market.

-

Monitor policy and geopolitics — tariffs, sanctions, trade flows, disruptions

Policy decisions now move copper as much as fundamentals. Tariffs, sanctions, and export controls reshape trade flows and create regional imbalances. Geopolitical tensions and supply disruptions — from strikes to permitting delays — reinforce the market’s focus on future scarcity.

-

Stay grounded in physical stress points — inventories, premiums, scrap

Headline stocks matter less than where the metal sits. Traders watch regional inventory tightness, premiums, treatment charges, and scrap availability to understand real physical stress. These signals reveal whether the market is genuinely tight or simply trading a narrative.

The consensus is that as long as capital flows remain strong, geopolitical risks persist, and the market prices future scarcity, copper can stay elevated — even in surplus.

Where Next for Copper?

As for immediate near-term dynamics, the copper market is treading water, increasingly driven by headline risk. Recent price action has been closely tied to developments around the Iran crisis, highlighting just how far copper has shifted into the macro arena.

The closure of the Strait of Hormuz presents a two-sided risk for copper:

-

On the bullish side, the Gulf is a major exporter of sulphur, a critical input for sulphuric acid used in leaching processes. With solvent extraction and electrowinning accounting for roughly a quarter of global refined output, continued disruptions to acid supply could tighten production, particularly in the DRC, and support prices.

-

On the bearish side, higher energy prices risk triggering a broader slowdown in global manufacturing, weakening copper demand. The longer the disruptions persist, the greater the downside risk to consumption.

With investors firmly in control of price formation, copper has effectively become part of a multi-asset macro trade on the trajectory of the Iran conflict. In this environment, both bulls and bears are less anchored to supply-demand balances and more dependent on the next geopolitical headline.

Author: Shairaz Ahmed, Principal Market Analyst

For more information or to discuss market dynamics, you can contact me on shairazahmed@smm.cn