SMM April 27 News:

Metals market:

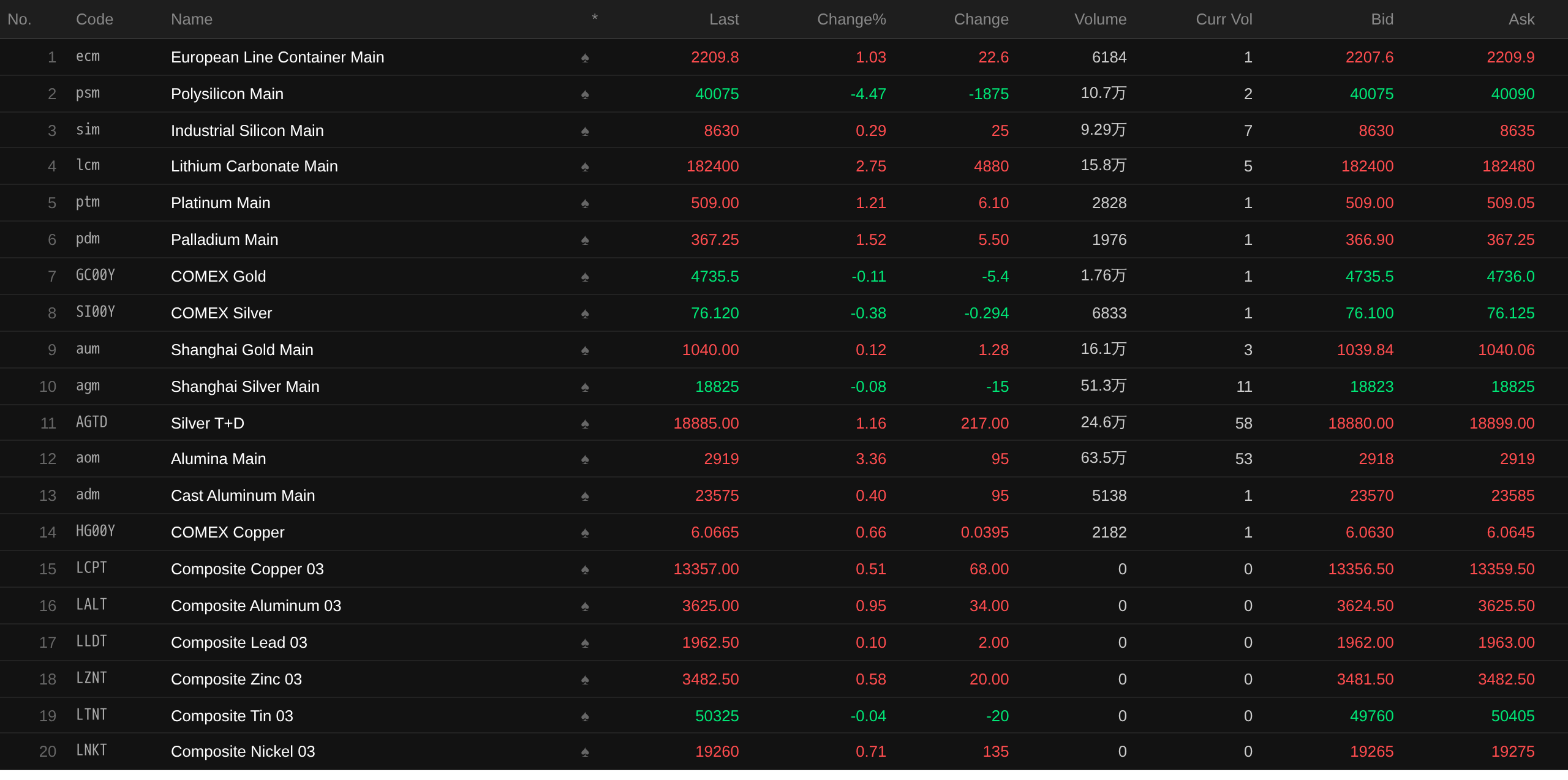

As of the midday close, domestic market base metals rose across the board. SHFE copper was up 0.38%, SHFE aluminum up 0.3%, SHFE lead up 0.3%, SHFE zinc up 0.7%, SHFE tin up 0.48%, and SHFE nickel up 2.62%.

In addition, the most-traded casting aluminum futures rose 0.4%, the most-traded alumina contract rose 3.36%, the most-traded lithium carbonate contract rose 2.75%, the most-traded silicon metal contract rose 0.29%, and the most-traded polysilicon futures fell 4.47%.

Ferrous metals mostly rose. Iron ore was flat at 786 yuan/mt, rebar edged up, hot-rolled coil rose 0.15%, and stainless steel rose 1.26%. Coking coal and coke: the most-traded coking coal contract rose 1.23%, and the most-traded coke contract rose 0.44%.

Overseas market base metals: as of 11:43, LME metals mostly rose. LME copper was up 0.51%, LME aluminum up 0.95%, LME lead up 0.1%, LME zinc up 0.58%, LME tin edged down, and LME nickel was up 0.71%.

Precious metals: as of 11:43, COMEX gold fell 0.11% and COMEX silver fell 0.38%. Domestic precious metals: the most-traded SHFE gold contract rose 0.12%, and the most-traded SHFE silver contract fell 0.08%.

In addition, as of the midday close, the most-traded platinum futures rose 1.21%, and the most-traded palladium futures rose 1.52%.

As of the midday close, the most-traded Europe containerized freight index contract rose 1.03% to 2,209.8 points.

As of 11:43 on April 27, midday futures quotes for selected contracts:

Spot and fundamentals

Copper:Today, Guangdong #1 copper cathode spot prices against the front-month contract: high-quality copper was quoted at a premium of 280 yuan/mt, flat with the previous trading day; standard-quality copper was quoted at a premium of 200 yuan/mt, flat with the previous trading day; SX-EW copper was quoted at a premium of 140 yuan/mt, flat with the previous trading day. The average price of Guangdong #1 copper cathode was 103,085 yuan/mt, up 290 yuan/mt from the previous trading day; the average price of SX-EW copper was 102,985 yuan/mt, up 290 yuan/mt from the previous trading day. Spot market: After the weekend, Guangdong inventory declined again, mainly due to fewer arrivals and some manufacturers stockpiling ahead of the holiday...

Macro front

China:

[NBS: January-March profits of China's above-scale industrial enterprises rose 15.5% YoY; non-ferrous sector profits surged 116.7% YoY]NBS data showed that from January to March, total profits of China's above-scale industrial enterprises reached 1.696 trillion yuan, up 15.5% YoY. From January to March, among above-scale industrial enterprises, state-controlled enterprises posted profits of 619.61 billion yuan (up 10.1% YoY), joint-stock enterprises 1.305 trillion yuan (up 20.9%), foreign-invested and Hong Kong, Macao, and Taiwan-invested enterprises 383.73 billion yuan (up 1.2%), and private enterprises 430.53 billion yuan (up 25.4%). Yu Weining, Chief Statistician of the Industrial Department of the National Bureau of Statistics (NBS), interpreted the industrial enterprise profit data for January–March 2026: In Q1, facing a complex economic environment, the CPC Central Committee and the State Council promptly stepped up macro regulation efforts and proactively implemented more active and effective macro policies. The industrial economy steadily rebounded, profits of above-designated-size industrial enterprises grew at a faster pace, profits in equipment manufacturing and high-tech manufacturing grew rapidly, profits in raw material manufacturing posted double-digit growth, and the efficiency of industrial enterprises continued to improve.

[National Energy Administration: China's Oil and Gas Supply Was Generally Stable and Orderly in Q1]The National Energy Administration held a press conference on April 27 to brief on the national energy situation and development achievements in Q1 2026. Xing Yiteng, Deputy Director of the Development Planning Department of the National Energy Administration, noted that energy security was effectively safeguarded. The impacts of the Venezuela crisis and the US-Israel-Iran conflict on China's energy supply were properly managed. In Q1, China's oil and gas supply was generally stable and orderly, with above-designated-size industrial crude oil and natural gas production up 1.3% and 3.0% YoY, respectively. Raw coal production remained stable despite a relatively high base in the same period last year, with above-designated-size industrial raw coal production up 0.1% YoY. The safety situation in the power sector was stable and improving, with efficient completion of power emergency responses to various natural disasters and successful completion of power supply assurance for the Chinese New Year and the Two Sessions. (Jin10 Data)

[PBOC Achieved a Net Withdrawal of 382 Billion Yuan via Reverse Repo Operations]The PBOC conducted 218.5 billion yuan of 7-day reverse repo operations today. As 600 billion yuan of 1-year MLF and 500 million yuan of 7-day reverse repo operations matured today, a net withdrawal of 382 billion yuan was achieved. (Jin10 Data APP)

US dollar:

As of 11:43, the US dollar index fell 0.08% to 98.42. Multiple sources revealed that the US Department of Justice was expected to conclude its criminal investigation into Fed Chairman Jerome Powell as early as Friday, thereby ending the standoff that could have delayed the appointment of Powell's successor. Sources said senior DOJ officials recently contacted several senators, including Republican Senator Tom Tillis, a member of the Senate Banking Committee, informing them of plans to drop the investigation into alleged cost overruns in the renovation of the US Fed's Washington headquarters and refer the matter to the Fed's internal watchdog. Powell's term is set to expire next month, but he indicated in March that he would remain in office until Trump's nominee for Fed Chairman, Kevin Warsh, is confirmed. According to the CME "Fed Watch" tool, the probability of the US Fed keeping interest rates unchanged in April was 100%. The probability of a cumulative 25-basis-point interest rate cut by June was 4.7%, while the probability of keeping rates unchanged was 95.3%. (Jin10 Data)

Data:

Germany's May GfK Consumer Confidence Index, the UK's April CBI Retail Sales Balance, and the US April Dallas Fed Business Activity Index are scheduled for release today.

Crude oil:

As of 11:43, oil prices in both markets rose, with WTI up 0.85% and Brent up 1.11%. Crude oil futures rose at the start of Monday's session as peace talks between the US and Iran reached an impasse, while oil shipments through the Strait of Hormuz remained limited, keeping global oil supply under sustained pressure. Crude oil futures prices swung wildly recently, as traders had to predict not only when oil exports from the Persian Gulf would resume, but also how long it would take for production in the region to recover to pre-war levels. Trump said on Sunday that Iran was facing growing domestic pressure due to its inability to export oil, which could cause long-term damage to its energy export infrastructure. Goldman Sachs analysts said on Sunday that they had pushed back their expectations for the Strait of Hormuz to return to normal export levels from mid-May to late June. Meanwhile, they raised their Q4 WTI crude oil price expectations from $75 per barrel to $83 per barrel. (Jin10 Data)

Citi raised its forecast for the average Brent crude oil price for the remainder of 2026 on Sunday evening local time, stating that if oil shipments through the Strait of Hormuz continued to be disrupted through the end of June, oil prices could rise to $150 per barrel. The bank raised its base-case average price forecasts for Brent crude oil in Q2, Q3, and Q4 of 2026 to $110, $95, and $80 per barrel, respectively. Citi also pushed back its expectations for the reopening of the Strait of Hormuz from mid-to-late April to the end of May. Citi stated: "Given that significant gaps remain between the two sides on their respective red-line issues, we believe the risks are tilted toward the upside for near-term bullish sentiment and H2 2026 base-case oil price forecasts." In the bullish scenario (30% probability), Citi assumed that oil shipment disruptions would persist through the end of June at a scale similar to the current level of disruption. Under this scenario, Brent prices could surge to $150 per barrel, with Q2 and Q3 2026 averages approaching $130 per barrel, before pulling back to around $100 in Q4. The bank also proposed a "super bullish" scenario in which the Strait of Hormuz remained closed beyond June, noting that this would have severe implications for the share of oil expenditure in both global and US economic output.

Spot Market Overview:

►

►

►

►

►

►

►

►

►

►

►

![Early Market Trading Volume Declined Overall, Demand Weakened but Transaction Center Held Steady [SMM Yangshan Spot Copper]](https://imgqn.smm.cn/usercenter/udUol20251217171712.jpg)

![Tight Bill Availability Combined with Month-End Reluctance to Sell, Downstream Pre-Holiday Stockpiling Supported Spot Premiums [SMM Shanghai Spot Copper]](https://imgqn.smm.cn/usercenter/xKfXl20251217171711.jpg)

![Macro Stalemate Combined with High-Price Suppression: SHFE Tin Weakened Then Rebounded, with Limited Pre-Holiday Stockpiling [SMM Tin Midday Review]](https://imgqn.smm.cn/usercenter/tyydv20251217171753.jpg)