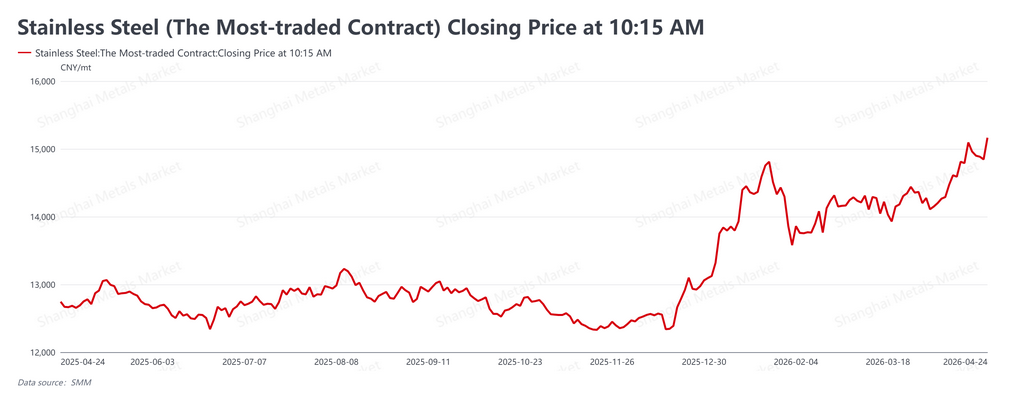

Chinese stainless steel futures closed the final week of the traditional "Silver April" peak-demand season on a firm note (April 20-24, 2026), with the most-active SHFE contract (SS2606) settling at RMB 15,165/mt (approximately $2,221/mt) on April 24, up RMB 70/mt (about $10/mt) from the previous Friday. The gains were driven almost entirely by Friday's session, after news of Indonesian RKAB mining-quota cuts and maintenance at major laterite ore mines shifted market attention from macro policy to supply-side cost support.

Macro backdrop: domestic stimulus, easing overseas risk premium

On the macro side, Chinese policymakers continued to reinforce growth expectations. The National Development and Reform Commission confirmed it would accelerate the deployment of RMB 800 billion (approximately $117 billion) in new policy-based financial instruments and is drafting a fresh domestic-demand strategy, while the People's Bank of China reiterated its commitment to a moderately accommodative monetary stance. Overseas, hawkish comments from several Federal Reserve officials were offset by progress in Middle East ceasefire negotiations, which eased the energy-risk premium and allowed the market to refocus on industry-specific supply-demand dynamics.

Fundamentals: inventory draws, but real demand lags the price move

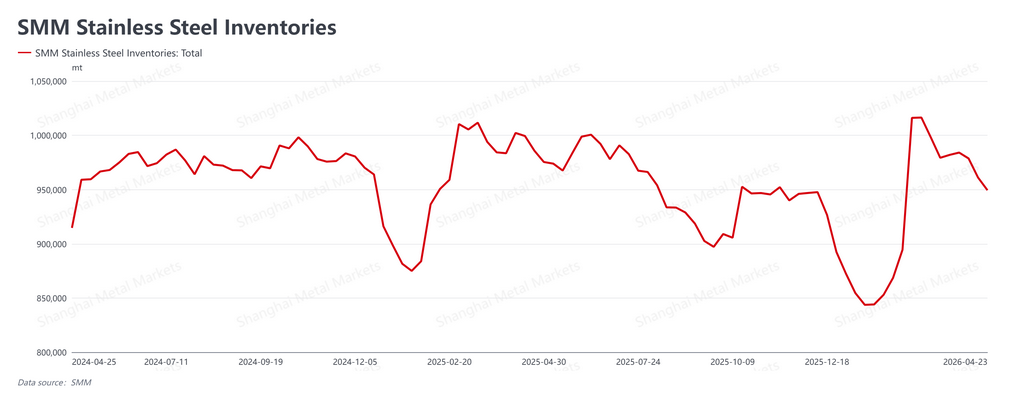

Inventory drawdowns accelerated through the week. SMM data shows social inventory fell to 949,400 mt, down 11,700 mt from 961,100 mt the week prior. The decline was driven by a combination of factors: active futures-spot arbitrage as the futures board rallied, price concessions from traders clearing stock, modest restocking ahead of the May Day holiday, and reduced mill allocations. That said, with spot prices tracking the futures board higher, end-users remained cautious about near-term volatility and purchasing did not translate into substantially higher volumes. Transactions were largely driven by arbitrage buying and delivery against existing orders — a pattern of "expectations leading, reality following" in which real demand has not yet caught up with the price move.

Cost side: Indonesian ore policy reinforces the bullish narrative

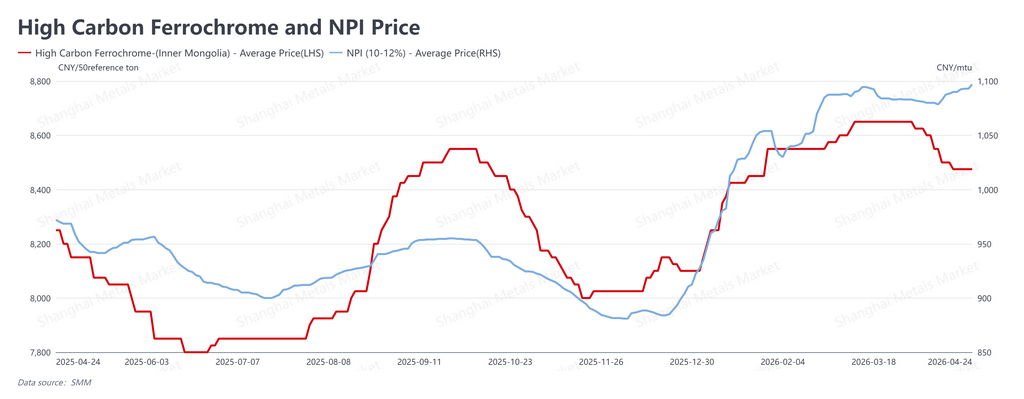

Cost-side support strengthened further. Friday's news of sharply reduced Indonesian RKAB initial quotas for 2026, together with maintenance at several major Indonesian nickel ore mines, reinforced bullish expectations for raw materials. As of April 24, Nickel Pig Iron (NPI) prices rose to RMB 1,097/nickel point (approximately $160.6/nickel point), while high-carbon ferrochrome held steady at RMB 8,475 per 50-base mt (approximately $1,241). Mill production costs have moved higher, though not as quickly as finished-product prices, meaning stainless steel mill margins are gradually recovering. With the supply-tightening narrative on raw materials intact, cost-side support underpinning stainless steel prices remains solid.

Outlook: firm bias into the post-holiday period, but watch the spot absorption rate

Stainless steel has stabilized at elevated levels heading into the May Day holiday period, supported by the Indonesian ore-policy narrative rather than by finished-goods demand. Even with Chinese mill output running high, the tightening raw-material story is giving finished steel a firmer floor. Post-holiday attention will focus on two variables: the rollout of Indonesia's RKAB quotas and the pace at which Chinese fiscal stimulus actually reaches the real economy. The SS2606 contract is expected to remain firm with an upward bias after the holiday, but the key risk to watch is whether physical demand can absorb current spot prices — if it cannot, the market remains vulnerable to a pullback from these highs.

![[SMM Analysis] Raw Material Policy Synergy Drives Cost Increase, Caution Prevails in Overseas Stainless Steel Demand](https://imgqn.smm.cn/usercenter/Btmsv20251217171733.jpg)

![[SMM Flash] Latest Market Update on Indonesian Sulfur](https://imgqn.smm.cn/usercenter/HfIIS20251217171709.jpg)