Magnesium Exports Hit Peak in March, Driven by Overseas Stockpiling and Post-Holiday Shipment Resonance

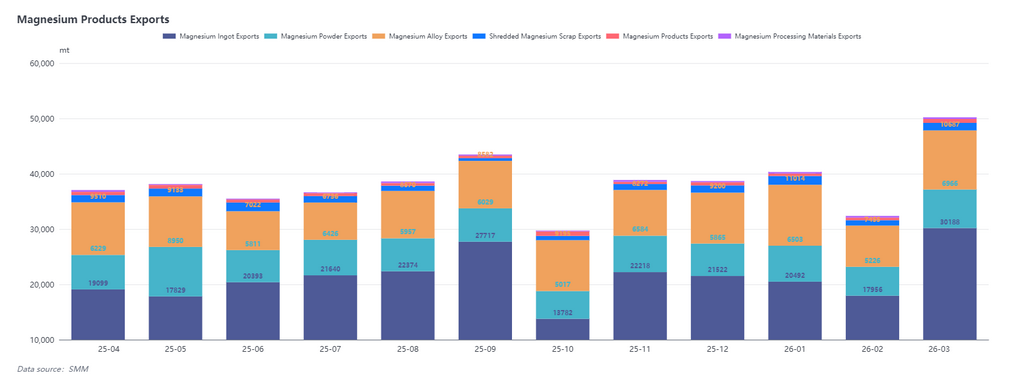

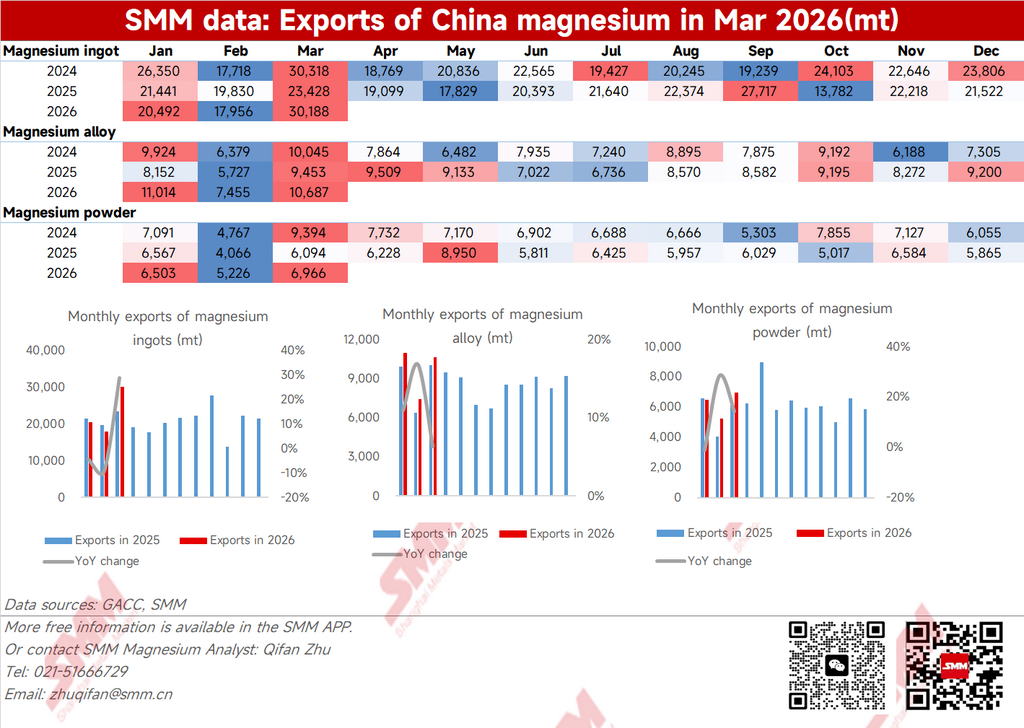

In March 2026, China's magnesium product exports reached 50,200 mt, up 55% MoM and up 21% YoY, hitting a recent export peak. Historical data showed that export highs in 2022 and 2024 also occurred in March, with export volumes largely comparable to March 2026. In contrast, overall export performance in 2025 was weak, down 6.24% YoY. Affected by tariff policy changes and the European energy crisis, exports remained sluggish in H1 2025; September became the relative peak month of that year due to the export rush effect ahead of tightened export policies.

There were two main reasons for the sharp rise in exports in March this year: first, magnesium prices were at low levels in December 2025, prompting downstream enterprises outside China to seize the opportunity to place orders and stockpile, coinciding with the Q1 procurement period; second, due to the Chinese New Year holiday, overseas clients concentrated their orders before early February, while a large number of orders delayed by the holiday were shipped in bulk in March, jointly pushing up the month's export volume.

Magnesium Ingot Led the Gains, Magnesium Alloy Grew Steadily, Magnesium Powder Recovery Boosted March Exports

By product, magnesium ingot exports hit a near one-year high in March, while magnesium alloy maintained a steady growth trend.

In March 2026, magnesium ingot exports reached 30,200 mt, up 68.12% MoM, with cumulative YoY growth of 6.08%. Price-wise, magnesium ingot export prices remained generally stable with a slight upward trend from February to March, only rising toward month-end due to sentiment among factories to hold prices firm and hold back from selling. The stable pricing environment provided favorable conditions for the placement of export orders and trader stockpiling. In addition, some order tenders were released early in early February, and combined with traders' expectations of ocean freight rate fluctuations, some shipping slots in early March were locked in advance, driving concentrated magnesium ingot shipments in the first ten days of March.

In March 2026, magnesium powder exports totaled 6,966 mt, up 33.3% MoM, with cumulative YoY growth of 11.77%. Since the beginning of 2026, export orders for magnesium powder have gradually recovered, with monthly demand being steadily released. Magnesium powder enterprises mostly purchased raw materials as needed and maintained a stable production and shipment pace. Orders shipped in March included some orders signed in Q4 2025 and early this year.

In March 2026, magnesium alloy exports totaled 10,700 mt, up 43.35% MoM, with cumulative YoY growth of 24.96%. Since the beginning of this year, export orders for magnesium alloy have performed well. According to an SMM survey, magnesium alloy export orders have been steadily scheduled through April this year. Demand for magnesium alloy from the overseas automotive market is growing steadily, with multiple die-casting and forming technologies gradually entering mass production, boosting incremental magnesium alloy demand both outside China and within China simultaneously.

Concentrated Demand Release from Europe and Japan, Canada Leading Magnesium Alloy Exports

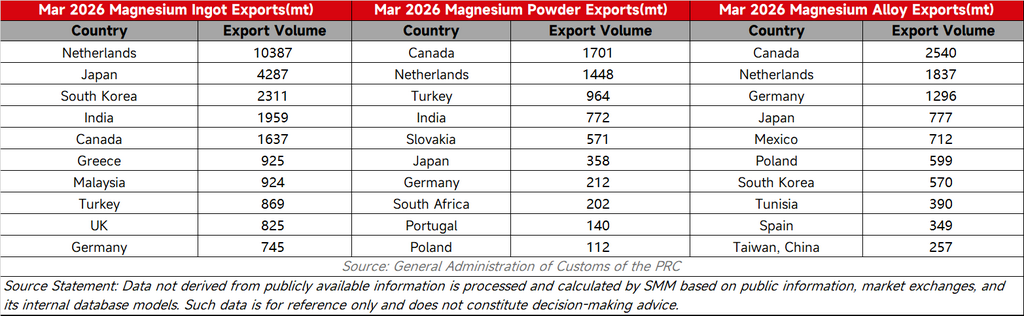

Exports by destination, in March 2026, China's magnesium ingot exports to the Netherlands reached 10,400 mt, accounting for 34%. Overall demand in Europe rose significantly, driven by two factors: first, tender orders from the earlier period were placed in bulk in February; second, expectations of rising ocean freight rates prompted a large volume of orders to be shipped in March. In addition, magnesium ingot exports to Japan in March totaled 4,287 mt, up 234% MoM, mainly because tightening export policies toward Japan triggered panic stockpiling among downstream enterprises, front-loading demand and pushing monthly exports to a peak.

Magnesium powder and magnesium alloy side, Canada has become a major export destination. Since 2026, China's magnesium alloy exports to Canada have continued to edge up, surpassing Europe. This shift was primarily boosted by growing demand from the automotive and aerospace sectors in the North American market, driving the release of magnesium alloy orders.

Market Outlook: Strong Exports but Lingering Concerns — Q2 Trend Remains to Be Seen

Looking ahead to Q2, the high export levels in March released a positive signal, indicating that overall ex-China demand is rebounding this year. Major markets such as Europe and North America have gradually emerged from the buffer period of 2025, with consumption demand recovering steadily. However, whether this growth trend can be sustained remains to be seen. Historically, after concentrated shipments in March, exports typically pull back notably in April and May. Moreover, escalating geopolitical conflicts since March 2026 have introduced uncertainties to export orders, and their impact on the aluminum industry and energy markets may manifest with a lag in Q2. Whether exports in 2026 can maintain the positive momentum still depends on the pace of new order releases outside China, fluctuations in the ocean freight market, and subsequent adjustments to China's export policies.

![[SMM Analysis] China's Magnesium Market Diverges: Tightening Export Controls & Softening Domestic Prices](https://imgqn.smm.cn/usercenter/mLwgx20251217171723.jpeg)