SMM, April 20:

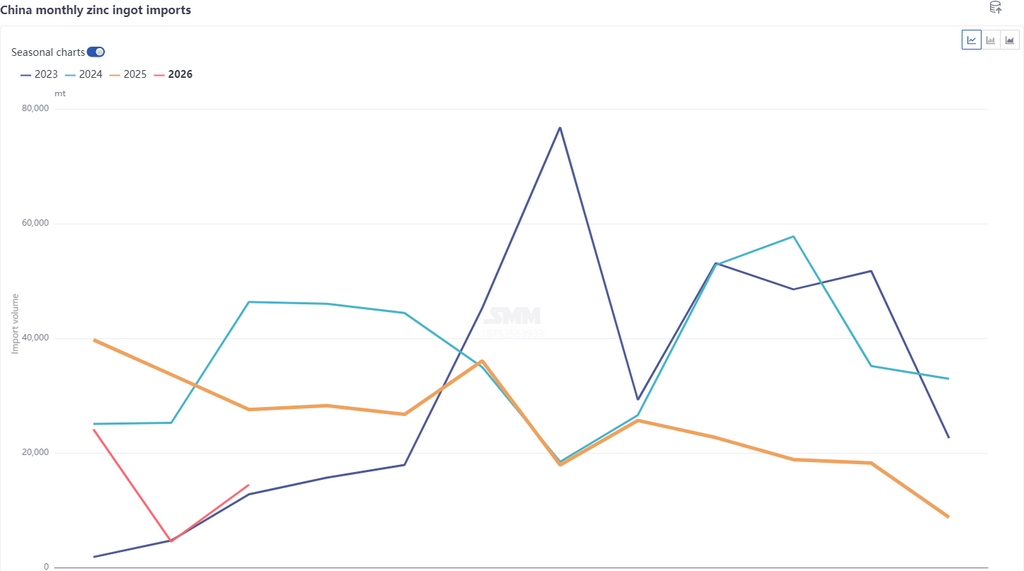

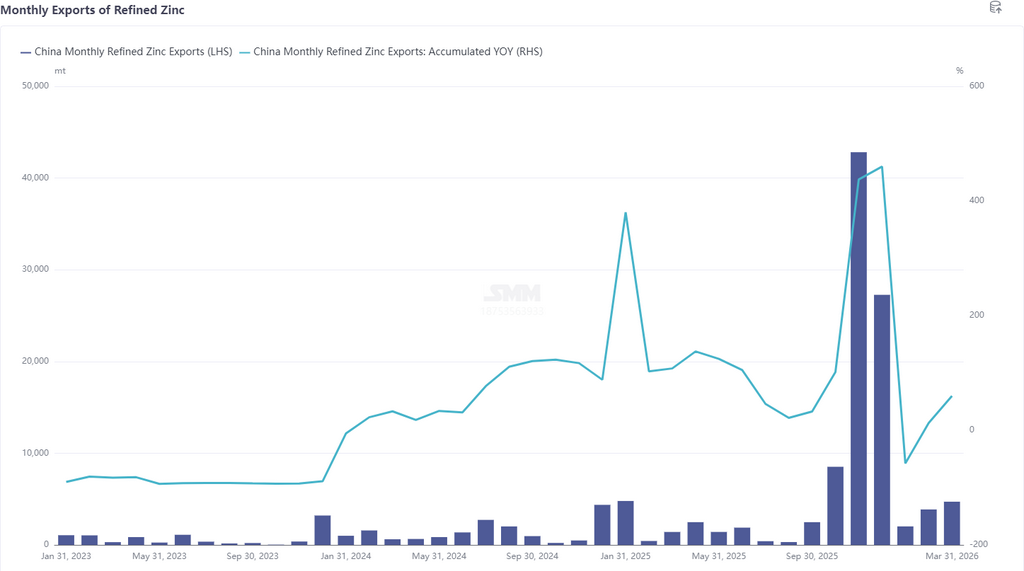

According to the latest customs data, refined zinc imports in March 2026 totaled 14,400 mt, up 9,900 mt or 220.14% MoM, down 47.53% YoY. Cumulative refined zinc imports from January to March reached 43,000 mt, down 57.32% YoY. Refined zinc exports in March were 4,700 mt, resulting in net exports of 32,500 mt of refined zinc from January to March.

By country, the top 3 refined zinc import sources in March were Kazakhstan (11,700 mt, 81.22%), Australia (900 mt, 6.33%), and South Korea (600 mt, 4.38%), with inflows primarily through Ordinary Trade mode. The top 3 export destinations in March were Vietnam (1,700 mt, 35.94%), Thailand (1,400 mt, 30.62%), and Indonesia (900 mt, 18.87%). Based on March import and export data, export data largely met expectations, but import data overall exceeded expectations. This was mainly because, although the zinc ingot import window remained closed, Kazakh zinc still arrived in March due to residual shipment issues, with imports increasing significantly MoM.

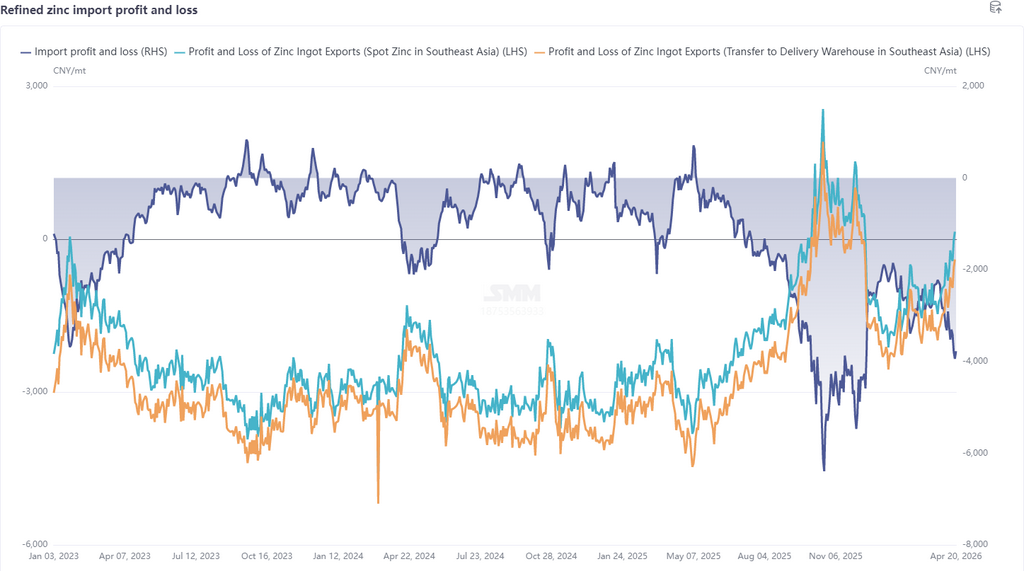

Entering April, on the macro front, uncertainties surrounding the Middle East geopolitical conflict remained significant, but tail risks of the conflict declined, market risk appetite improved, and attention turned to actual negotiation outcomes. Fundamentals side, the overseas market overall continued to run on the stronger side, with LME inventory sustaining a low level around 110,000 mt, LME Cash-3M hovering near a slight contango structure, and against the backdrop of energy shortages, European smelters underwent maintenance while overseas mines also faced expectations of diesel tightness, providing strong support on the supply side. In China, although domestic and import TCs continued to decline, with import TCs falling to around -$30/dmt, smelters maintained high production enthusiasm due to sulphuric acid prices surging to around 2,000 yuan/mt and minor metal profit support. April production is expected to still increase, yet with consumption falling short of expectations, social inventory accumulated again to 260,000 mt. Overall, with LME outperforming SHFE, the import ratio continued to correct downward to around 7, and the export window showed the possibility of opening. Imports of zinc ingots are expected to decline notably after the tail-end shipments of Kazakh zinc decrease in April, while exports are expected to increase. However, as the export window has not yet fully opened, the magnitude of the increase is expected to be limited.

Data Source Disclaimer: Data other than publicly available information is derived by SMM based on public information, market communication, and SMM's internal database models, and is for reference only and does not constitute decision-making advice.