Recent Volatility in the Copper Scrap Market: China, Japan, and Korea Spot Shortage Reshapes Trading Dynamics

Recently, the copper scrap raw material market has been experiencing significant volatility. According to recent surveys and price point feedback from SMM, there is a prominent spot shortage of copper scrap raw materials in China, Japan, and South Korea. This tight supply landscape is reshaping both domestic and international trade price trends within the region.

What exactly is causing this severe "hard-to-find" shortage in the Asian copper scrap market? And what kind of trading tug-of-war is hidden behind the elevated offers?

Why the Spot Shortage? Three Factors Triggering a "Butterfly Effect"

The current situation of scarce spot availability and tight supply in the China, Japan, and South Korea markets is not caused by a single factor, but rather a combination of recent dynamics on both the supply and demand sides:

Copper Price Corrections Triggering Upstream "Reluctance to Sell": Recent pullbacks in copper prices have squeezed the profit margins of upstream stockholders, causing a widespread reluctance to sell. Meanwhile, market pricing coefficients continue to climb. This gap in psychological expectations between buyers and sellers has directly dampened overall market trading activity.

Weak Consumption Season Coupled with High Copper Prices Leading to a General Drop in February Imports: Looking back at February this year, copper scrap import volumes in China, Japan, and South Korea all showed a significant downward trend. On one hand, China—the largest copper scrap consumer in Asia and globally—celebrated the traditional Lunar New Year in February. Widespread factory closures and holidays drastically reduced the actual throughput for the month. On the other hand, sustained high copper prices in February also severely suppressed the procurement willingness of downstream processing enterprises, leading to postponed orders.

The "Lag Effect" of Previous Import Declines Emerging: The most direct consequence of the overall decline in February imports is the current scarcity of port and domestic spot inventories, setting the tone for the current "tight supply."

Price Trend Analysis: Domestic and International Prices Pushed Up, Trading Suppressed

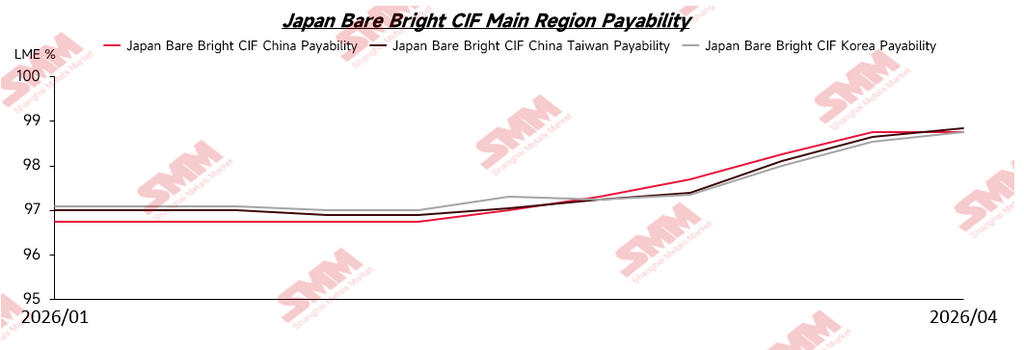

Supported strongly by the continuous shortage of spot supply, the center of gravity for domestic copper scrap prices in China, Japan, and South Korea is steadily shifting upward. The tight supply and trading heat in the domestic market are rapidly transmitting to the international market, sparking an even more intense price tug-of-war.

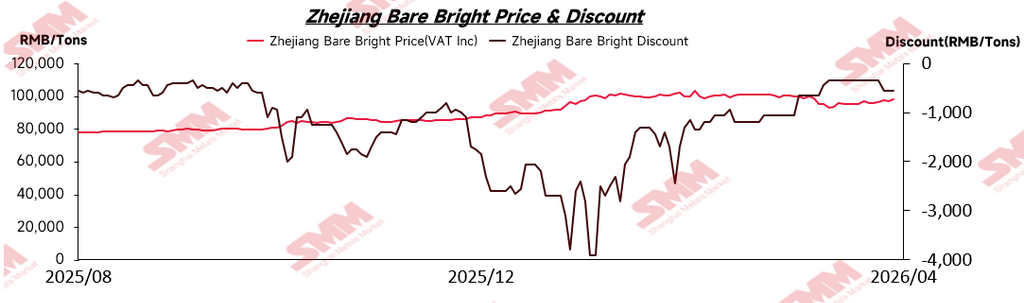

Recently, China's imported tax-included copper scrap market has faced multiple pressures. Driven by tightening overall spot supply, copper price corrections, and a shortage of market tax invoice resources, the discount margins for Bare Bright copper have continued to narrow and remained at squeezed levels. The resonance of these factors even caused the price of tax-included Bare Bright copper to briefly surpass that of refined copper, creating a rare "price inversion." Looking ahead, it is expected that until the invoice shortage issue is substantially alleviated, the situation of squeezed Bare Bright discounts will persist for some time.

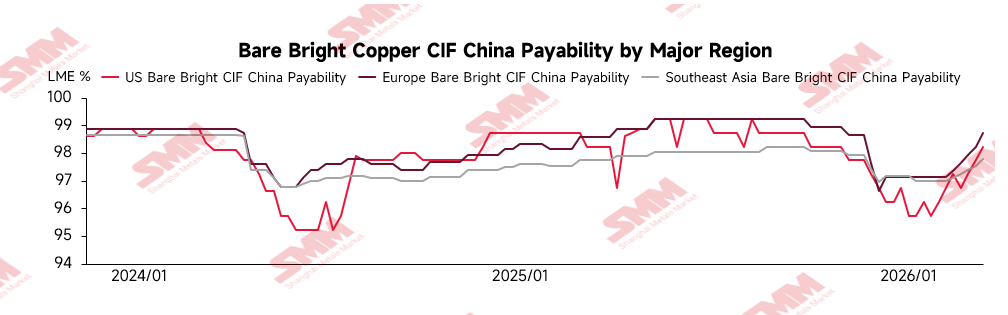

Furthermore, according to SMM, the recent phased correction in copper prices has further stimulated the price-supporting sentiment among overseas stockholders. Currently, overseas copper scrap traders hold a firm stance on Bare Bright copper offers, with their pricing coefficients against the LME briefly surging to a high range of 99% - 99.5%.

However, data feedback from SMM's actual transaction tracking shows a clear stalemate between buyers and sellers, with the market's true transaction center of gravity remaining deadlocked in the 98.5% - 99% range.

Why are High Offers Hard to Materialize? The Core Lies in the "Economic Substitutability" Tipping Point

For downstream processing enterprises, the core advantage of copper scrap lies in its price advantage over refined copper (cathode). When the pricing coefficient of Bare Bright copper breaks above 99% or even higher, its actual tax-included delivered cost will be essentially on par with refined copper. Once this price advantage is lost, the economic substitutability of copper scrap is significantly reduced. Downstream buyers will naturally shift their procurement to refined copper, thereby forming a natural "ceiling" that suppresses high offers for copper scrap.

Summary and Market Outlook

Overall, the "tight supply-demand balance" in the CJK copper scrap market is expected to persist in the short term, and the tug-of-war between upstream reluctance to sell and downstream fear of high prices will intensify. At this critical juncture where Bare Bright copper prices approach parity with refined copper, accurately grasping every price fluctuation and coefficient change is crucial for corporate procurement and sales strategies.