Las exportaciones de productos de magnesio arrancaron con fuerza en enero-febrero de 2026, con un aumento acumulado de 3.400 t

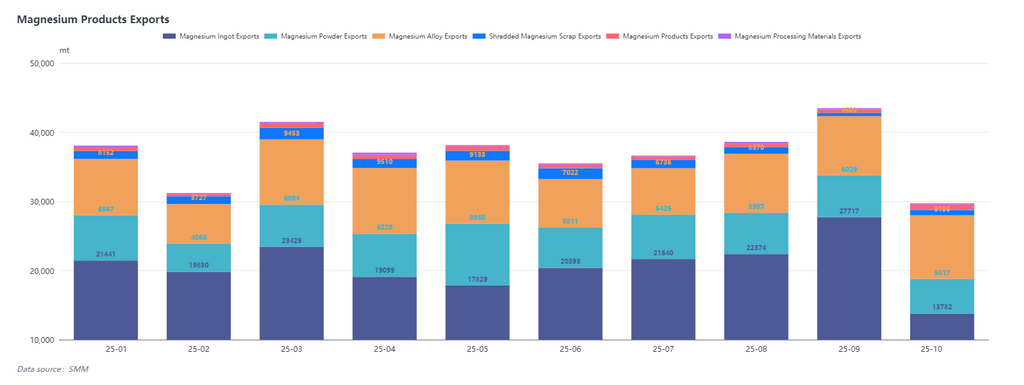

En enero de 2026, las exportaciones chinas de productos de magnesio mostraron un sólido desempeño y alcanzaron 40.300 t, un 6 % más interanual y un 4,2 % más que en diciembre de 2025. Hubo dos razones principales: primero, los pedidos se concentraron en el cuarto trimestre de 2025, cuando los precios del magnesio siguieron bajando, y las empresas aguas abajo fuera de China fueron asegurando sucesivamente los pedidos del primer trimestre de 2026 a partir de octubre. Sumado a unas exportaciones generalmente débiles en el primer semestre, la demanda repuntó al cierre del año, impulsando un fuerte aumento de las exportaciones en enero; segundo, debido al feriado del Año Nuevo chino en febrero, los comerciantes optaron en su mayoría por concentrar los envíos en enero, cuando la capacidad de transporte marítimo era suficiente, lo que elevó aún más la escala de las exportaciones. En conjunto, enero sentó una base sólida para el mercado exportador de magnesio de todo el año.

En febrero de 2026, las exportaciones totales de productos de magnesio fueron de 32.300 t, un 3,7 % más interanual y un 1,96 % menos intermensual. Aunque las exportaciones de febrero retrocedieron respecto al mes anterior por el feriado del Año Nuevo chino, el nivel general siguió estando por encima del mismo período de 2025. Las exportaciones acumuladas de enero-febrero alcanzaron 72.700 t, un aumento de 3.400 t frente al mismo período del año pasado, con un arranque general positivo.

La aleación de magnesio lideró el crecimiento exportador al inicio del año; el lingote de magnesio estuvo bajo presión, mientras que el polvo de magnesio se mantuvo estable

Por producto, el aumento de la demanda de exportación al comienzo de 2026 provino principalmente de la aleación de magnesio.

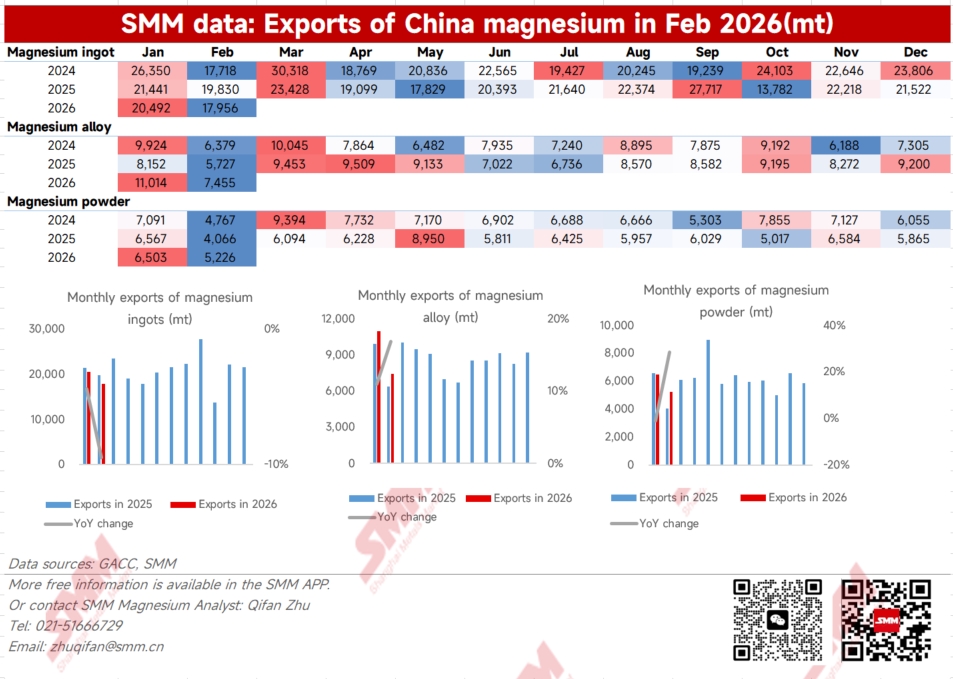

Lingote de magnesio: En enero de 2026, las exportaciones chinas de lingote de magnesio fueron de 20.500 t, un 4,79 % menos intermensual; en febrero, las exportaciones fueron de 18.000 t. Las exportaciones acumuladas de enero-febrero cayeron un 6,8 % interanual.

Por estructura regional, la caída de las exportaciones provino principalmente del mercado europeo. En enero, las exportaciones a los Países Bajos fueron de solo 3.353 t, un 33,73 % menos intermensual. La razón principal fueron factores estacionales: a mediados de diciembre de 2025, la acumulación de inventarios en puertos fuera de China ya era suficiente, mientras que el consumo se desaceleró durante las fiestas navideñas. En particular, los comerciantes en Europa emitieron menos pedidos de lingote de magnesio, lo que provocó un marcado retroceso de las exportaciones.

Aleación de magnesio: En enero de 2026, las exportaciones chinas de aleación de magnesio alcanzaron 11.000 t, un 19,72 % más intermensual, marcando un nuevo máximo mensual en casi un año; en febrero, las exportaciones fueron de 7.455 t. Las exportaciones acumuladas de enero-febrero aumentaron un 33,07% interanual.

Al observar la tendencia de todo 2025, las exportaciones de aleaciones de magnesio fluctuaron de forma significativa, pero tras entrar en el tercer trimestre, la demanda fuera de China se recuperó gradualmente y se estabilizó. En 2026, este impulso de crecimiento continuó en enero, con una liberación concentrada de pedidos, impulsada principalmente por la prisa de las empresas por completar los envíos antes del Año Nuevo chino y por calendarios de producción a plena capacidad. Según la encuesta de SMM, los pedidos de exportación de aleaciones de magnesio ya se han programado de forma estable hasta abril de este año, lo que indica una fuerte resiliencia de la demanda fuera de China. En general, se espera que las exportaciones de aleaciones de magnesio se conviertan en un importante respaldo para el crecimiento del comercio exterior de productos de magnesio en 2026, y debe seguirse de cerca la ejecución de los pedidos y los cambios en la demanda fuera de China.

Polvo de magnesio: En enero de 2026, las exportaciones chinas de polvo de magnesio fueron de 6.503 tm, un 10,88% más intermensual; las exportaciones de febrero fueron de 5.226 tm. Las exportaciones acumuladas de enero-febrero aumentaron un 10,3% interanual.

En general, las exportaciones de polvo de magnesio se mantuvieron relativamente estables, con pedidos de comercio exterior basados principalmente en compras según necesidad. Las exportaciones aumentaron ligeramente a comienzos de año, y la continuidad de este impulso de crecimiento seguirá dependiendo del desempeño exportador de marzo.

Las exportaciones de lingotes de magnesio a los Países Bajos cayeron significativamente, mientras que las exportaciones de aleaciones de magnesio a Canadá registraron un fuerte crecimiento

Por mercado de destino en términos de exportaciones,

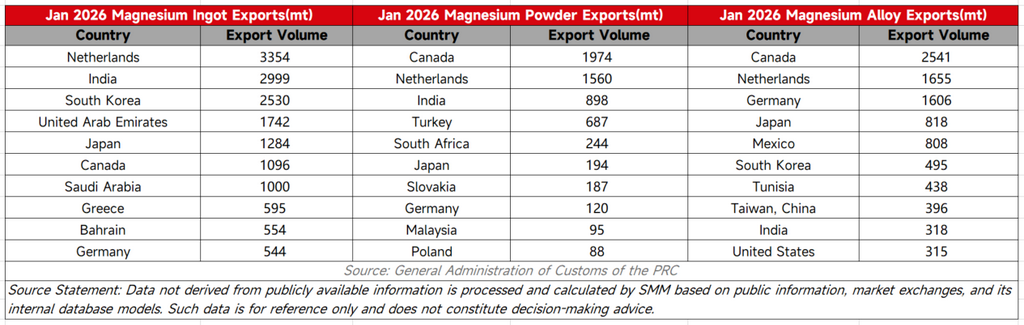

los principales mercados de demanda de lingotes de magnesio siguieron concentrados en los Países Bajos, India y Corea del Sur. La caída de las exportaciones provino principalmente del mercado neerlandés, mientras que la demanda del mercado indio se mantuvo estable. Además, las exportaciones a Japón fueron de 1.284 tm en enero y 1.938 tm en febrero, sin una caída general evidente. Canadá siguió siendo el principal destino de las aleaciones de magnesio y del polvo de magnesio. Entre ellos, las exportaciones de aleaciones de magnesio a Canadá alcanzaron 2.541 tm, con un aumento relativamente destacado.

Los conflictos geopolíticos alteraron las cadenas de suministro, generando incertidumbre para las exportaciones de magnesio en el segundo trimestre

De cara a las exportaciones del segundo trimestre, el impacto de los conflictos geopolíticos sobre las cadenas globales de suministro se está haciendo cada vez más evidente. Según SMM, la escalada del conflicto entre Estados Unidos e Israel a comienzos de marzo ya ha provocado interrupciones del suministro en dos grandes plantas de aluminio de Oriente Medio: la planta de aluminio Qatalum, en Catar, fue cerrada por completo debido a un corte en el suministro de gas natural. Su capacidad nominal anual de aluminio primario era de 636.000 tm, y se prevé que complete un cierre ordenado para finales de marzo; la reanudación total de la producción requerirá entre 6 y 12 meses. Alba de Baréin declaró fuerza mayor debido a las interrupciones del transporte marítimo en el estrecho de Ormuz y no pudo cumplir los contratos de suministro. Como resultado, los pedidos de compra de materia prima de magnesio en el mercado de Oriente Medio se han paralizado desde marzo, y los envíos se han visto interrumpidos de forma generalizada.

Además, la crisis de suministro de aluminio se ha extendido aún más al mercado europeo, ejerciendo presión sobre los sectores de procesamiento de aleaciones de aluminio y de energía, y generando un importante lastre para la demanda de exportaciones de magnesio. Aunque el mercado de exportación de magnesio tuvo un buen comienzo en los dos primeros meses de 2026, las exportaciones posteriores a marzo y en el segundo trimestre afrontan una considerable incertidumbre debido a las perturbaciones geopolíticas, y la tendencia previamente estable podría romperse.

![[Análisis del mercado de magnesio de SMM] El mercado chino de magnesio muestra divergencia ante el endurecimiento de los controles de exportación y el debilitamiento de los precios internos](https://imgqn.smm.cn/usercenter/mLwgx20251217171723.jpeg)