News release: March 23, 2026

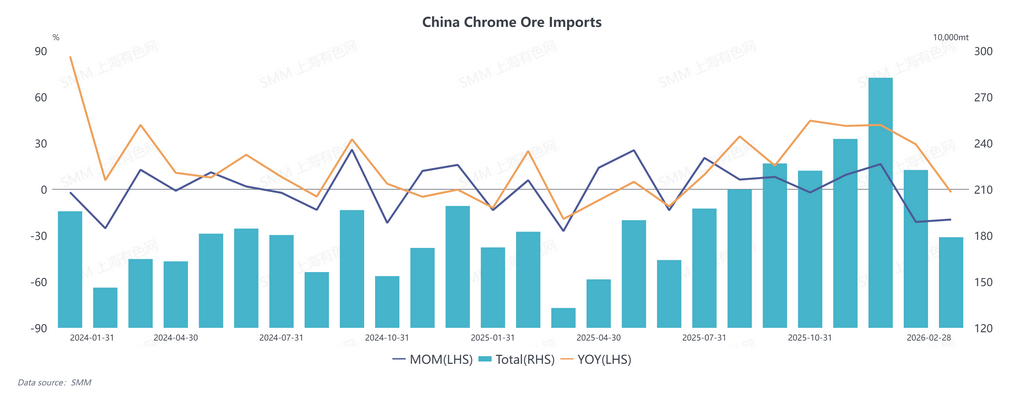

In January 2026, China's total chrome ore imports amounted to 2.2256 million tons, down 21.2% month-on-month and up 29.2% year-on-year. Specifically, imports from South Africa reached 1.8050 million tons, a month-on-month decrease of 19.4% and a year-on-year increase of 24.0%; imports from Turkey stood at 77,500 tons, dropping 35.0% month-on-month; and imports from Zimbabwe were 224,500 tons, declining 20.2% month-on-month.

In February 2026, China imported 1.7888 million tons of chrome ore in total, falling 19.6% month-on-month and 2.0% year-on-year. Among this volume, imports from South Africa were 1.4372 million tons, down 20.4% month-on-month and 10.1% year-on-year; imports from Turkey hit 107,100 tons, rising 38.1% month-on-month; and imports from Zimbabwe totaled 175,400 tons, a month-on-month drop of 21.9%.

Combined for January and February 2026, China’s cumulative chrome ore imports reached 4.0144 million tons, up 13.2% year-on-year. Breakdown by origin: imports from South Africa were 3.2422 million tons (up 6.2% year-on-year), imports from Turkey were 184,700 tons (up 55.8% year-on-year), and imports from Zimbabwe were 400,000 tons (up 70.3% year-on-year).

Affected by the rainy season, chrome ore mining and shipments in South Africa and Zimbabwe have been relatively constrained. According to South African customs data, South Africa’s total chrome ore exports in January 2026 were 2.1261 million tons, down 5.3% month-on-month and up 54.4% year-on-year, including 1.3831 million tons exported to China, a month-on-month decrease of 5.7% and a year-on-year surge of 138.3%. In addition, Zimbabwe has imposed additional export tariffs on chrome ore. Coupled with unresolved port congestion issues at the Port of Beira, chrome ore shipments have decreased accordingly. Escalating geopolitical conflicts worldwide have pushed up fuel prices and ocean freight rates, lifting the cost of overseas chrome ore and driving chrome ore prices to a relatively high level of 60 yuan per metric ton unit. On the downstream demand side, raw materials purchased for pre-holiday inventory have been consumed, while high ferrosilicon chromium production schedules have sustained steady and growing purchasing demand for chrome ore. Overall, buoyed by rising costs and robust demand, chrome ore prices are expected to maintain a strong trend in the short term.

![[SMM Analysis] Tungsten Prices Rally on Long Contract Prices & Tight Spot Supply](https://imgqn.smm.cn/production/admin/news/cn/thumb/gsyYF20180628085444.jpeg?imageView2/1/w/176/h/110/q/100)