SMM News, March 6,

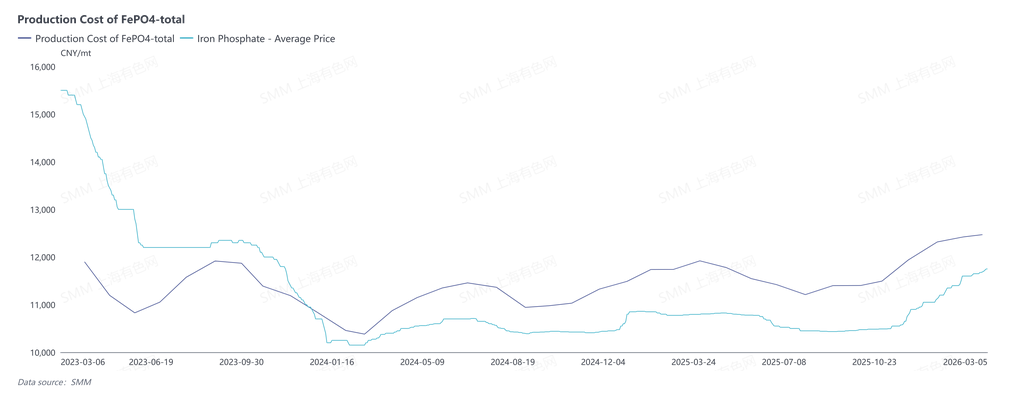

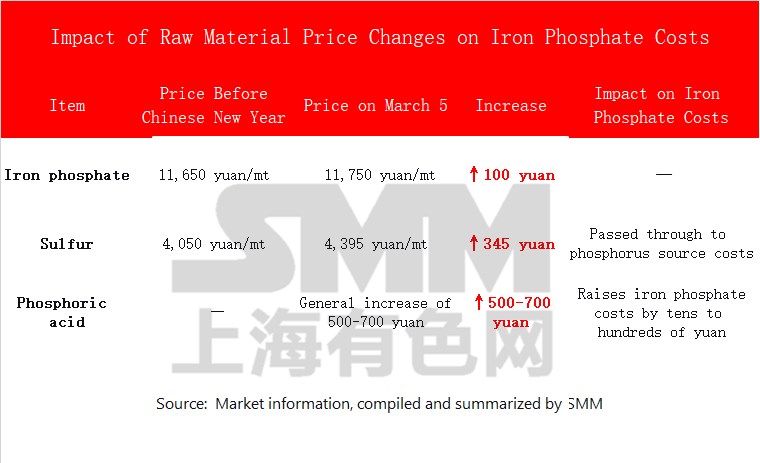

Key points: After the Chinese New Year, the price of iron phosphate rose by 100 yuan/mt, but it has not yet been implemented. Upstream, phosphoric acid suddenly jumped by 500-700 yuan/mt, directly wiping out the entire increase and even causing a negative spread. The root cause of this round of price hikes lies in sulphur: tight global supply coupled with the US-Iran geopolitical conflict sent sulphur prices surging by 345 yuan/mt, driving a broad-based rise in phosphorus source costs. Previously, sulphur price increases faced significant resistance in being passed downstream from the agricultural segment; this time, they have been transmitted downstream across the board. Iron phosphate enterprises have once again become the “middle layer”: the price increase is merely an illusion of cost pass-through, and profit improvement remains a luxury.After the Chinese New Year, the iron phosphate market finally saw the long-awaited signal of recovery. As of March 5, 2026, the delivery-to-factory price, tax included, per mt of iron phosphate rose from 11,650 yuan before the holiday to 11,750 yuan, a slight increase of 100 yuan/mt. Although the increase was relatively small, it at least offered a brief respite to the long-strained cost side.

However, before anyone could catch their breath, on March 5, phosphoric acid prices suddenly rose across the board by 500-700 yuan/mt—before iron phosphate enterprises had time to celebrate, the “cleaver” on the cost side had already come down.

Up 100 yuan, yet “taken” for more. On the surface, the rise in iron phosphate prices looks positive. But breaking down the cost structure, the truth is far from encouraging.

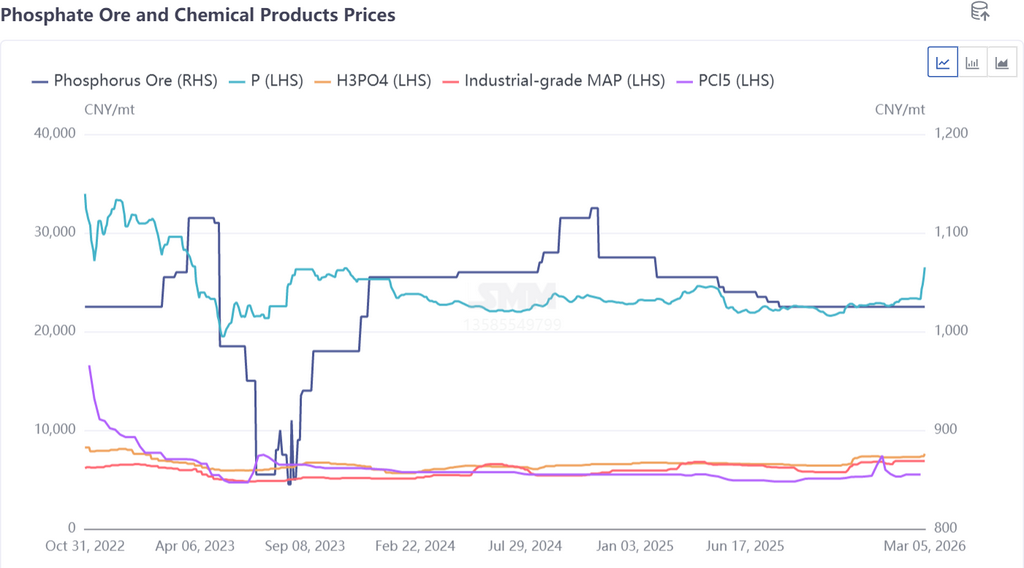

On March 5, 2026, phosphoric acid prices were generally raised by 500-700 yuan/mt. Based on phosphoric acid’s share in iron phosphate costs, this item alone will lift iron phosphate production costs by anywhere from tens to several hundred yuan—meaning that the newly gained 100 yuan, before it even had time to settle, was largely “taken” by the raw material side, and may even turn into a negative spread. This is especially true for the iron-route process, where the cost impact is greater.

Why did phosphoric acid suddenly rise? It was that same “old acquaintance”—sulphur

Geopolitics “adds fuel to the fire”

If tight supply and demand is an “old topic,” then the US-Iran geopolitical conflict that broke out on February 28, 2026 poured a bucket of oil onto an already taut sulphur supply chain.

China’s dependence on sulphur imports exceeds 50%, with Middle Eastern supply accounting for as much as 56.2%; Iran is also China’s second-largest source of sulphur imports from the Middle East. After the escalation of the conflict, navigation through the Strait of Hormuz was impeded, and short-term supply from Iran essentially dropped to zero. Other sulphur-producing countries in the Middle East simultaneously restricted shipments and sharply raised prices, causing the effective global circulation volume of sulphur to plunge by more than 10%.Although phosphoric acid enterprises only made concentrated price adjustments on March 5 (an industry practice among major producers to adjust prices on the 5th), in reality, phosphoric acid production costs had already begun rising on February 28. It simply took some time for the pass-through to reach the iron phosphate segment.

Looking back at this round of price fluctuations, iron phosphate enterprises have once again fallen into a familiar predicament:

Downstream: iron phosphate prices finally rose, by 100 yuan/mt.

Upstream: phosphoric acid prices surged by 500-700 yuan/mt, and cost pressure was rapidly transmitted.

Root cause: sulphur rose by 345 yuan/mt, with geopolitical conflict intensifying tight supply.

The 100-yuan gain, before it could be pocketed, was “shared away” in large part—if not entirely—by upstream phosphorus sources. Iron phosphate enterprises once again played the role of the “middle layer”: upstream raw materials rose, downstream pass-through was not smooth, and profit margins were repeatedly squeezed.

Conclusion: The passive position remains unchanged, and profit improvement is still a luxury.

This round of iron phosphate price increases was essentially a cost-driven, passive adjustment rather than a demand boost leading to profit improvement. The sulphur–phosphoric acid–iron phosphate cost pass-through chain is clear and brutal: sulphur rises, phosphoric acid follows, iron phosphate costs are lifted accordingly, and most (if not all) of the price increase is swallowed by the raw material side.

Against the backdrop of an unchanged pattern of tight global sulphur supply and ongoing geopolitical risks, iron phosphate enterprises will still face the severe test of elevated costs and thin profits. The fruits of the price-hike “revolution” have once again been “stolen” by sulphur and phosphoric acid.

Last ferrous sulphate incident: Iron phosphate rose by 500 yuan yet “no profit to be made”? A price frenzy swallowed by costs [SMM Analysis]

https://t.smm.cn/c2S7z8oT

Note: If you have any additions or corrections to the details mentioned in this article, please feel free to contact us at any time. Contact information is as follows:

Tel: 021-20707860 (or add WeChat 13585549799) Yang Chaoxing, thank you!