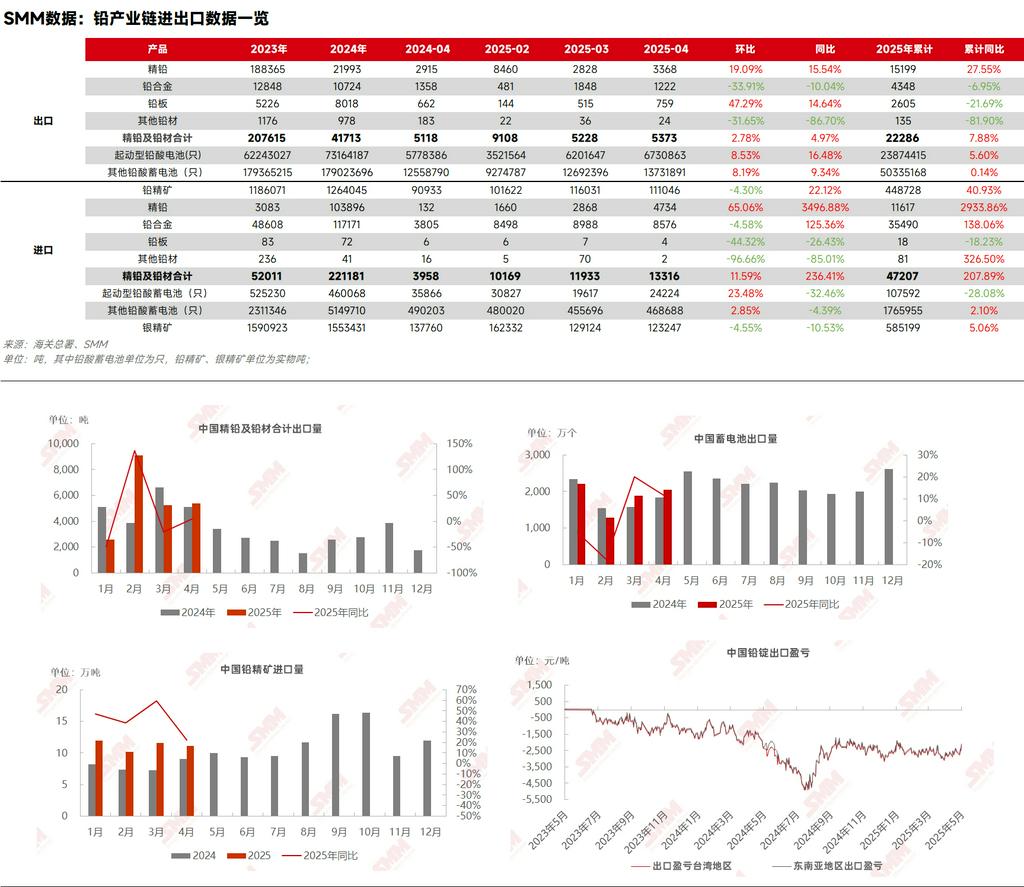

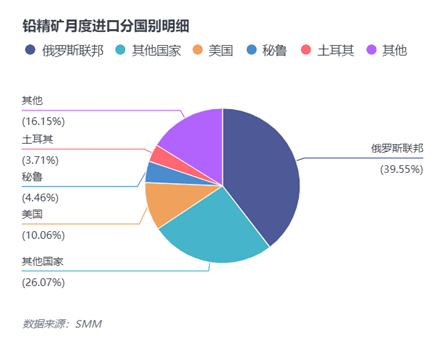

According to customs data, in April 2025, China's lead concentrate imports reached 111,046 mt, down 4.3% MoM and up 22.1% YoY. The cumulative lead concentrate imports for 2025 were approximately 448,700 mt, representing a 41% increase compared to 2024. By country, Russia, the US, and Peru were the main sources of lead concentrate imports in April.

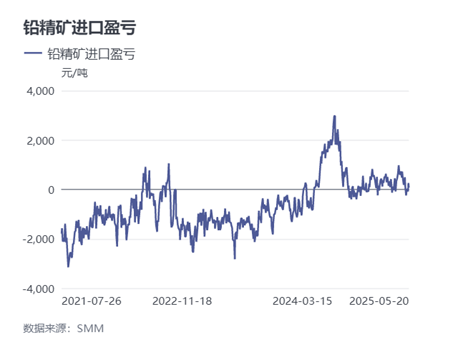

From the perspective of import profit/loss, despite the brief opening of the lead import window, the profitability of lead concentrate imports remained slim. Additionally, the tender and bid TC quotes for lead concentrates in the market continued to hover between -20 and -50 US dollars per dmt. Smelters primarily relied on imported ore ordered last year, with low enthusiasm for spot order purchases.

Despite the year-on-year increase of over 40% in lead concentrate imports, smelters indicated that lead concentrate TCs did not rebound in Q1 and Q2 2025. The strengthening of precious metal prices in Q1 2025 boosted the production enthusiasm of lead smelters, leading to an increase in lead smelter production YoY and a growing demand for silver concentrates or silver-bearing lead ores. In mid-to-late May, due to tight supply of lead-bearing recycled materials, domestic lead concentrate TCs may once again test a downward trend.

![Macro Weakness and Divergent Domestic and Overseas Fundamentals: LME Lead Prices Expected to Continue Outperforming SHFE [SMM Weekly Lead Market Forecast]](https://imgqn.smm.cn/usercenter/TmYox20251217171721.jpeg)

![Lead Prices Fluctuated Downward During the Week, Downstream Cautious Amid Fear of Price Decline, Purchase Willingness Low [SMM Refined Lead Spot Market Weekly Review]](https://imgqn.smm.cn/usercenter/lIHfM20251217171721.jpeg)

![SMM Primary Lead Smelter Weekly Operating Rate (May 29, 2026 - June 4, 2026) [SMM Primary Lead Smelting Operating Rate Weekly Review]](https://imgqn.smm.cn/usercenter/mfCMp20251217171721.jpeg)