SMM10, 19 March: non-ferrous entity enterprises often face the pressure of inventory management, order management, credit risk, capital, profit and so on. How to avoid risk and carry out high-benefit risk management to realize steady management is a big difficulty. At the "2018 China Nonferrous Metals Industry Annual meeting and 2019 (SMM) Metal Price Forecast Conference" hosted by Shanghai Nonferrous Metals Network (SMM), Liu Dongdong, assistant general manager and marketing director of Huatai Great Wall Capital Management Co., Ltd., combined with a case study, shows in detail how nonferrous enterprises use metal derivatives for risk management.

There are some problems that often exist in the use of futures arbitrage: the occupation of funds, the pressure to pursue insurance, the shortage of liquidity, the avoidance of risks, but at the same time to give up the possibility of potential profits; the strategy is not flexible enough. The use of option risk management strategy has four advantages, such as nonlinear profit and loss structure, higher capital utilization efficiency, more fault tolerance and more diversified profit methods.

The advantages of using option risk management strategy are: nonlinear profit and loss structure; higher capital utilization efficiency; more fault tolerance; more diversified profit methods.

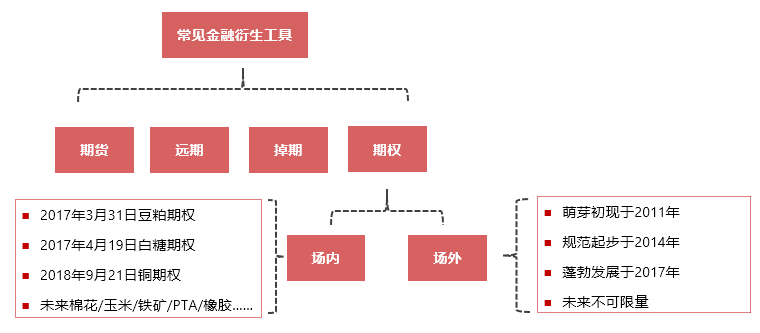

Options solve six problems in the industrial chain: price risk problem, capital circulation problem, credit risk problem, multiple strategy problem, service chain problem, position confidentiality problem.

The application of options in non-ferrous metal industry has three characteristics: low profit margin in the industry, unable to pay the "high" ordinary option cost, relatively high value of goods, high capital pressure, and the need to improve the efficiency of capital utilization. The industry is mature, the price difference is stable, the market fluctuation as a whole is small, and there are occasional pulse bands. For this reason, it is mainly composed of rolling covered put option, supplemented by a small amount of spread option / neckline option / trinomial neckline option, virtual or real value option and less flat value option, and the main method is rolling covered put option, supplemented by a small number of spread option / neckline option / trinomial neckline option combination. It is mainly based on direction / volatility trading, and there are fewer arbitrage opportunities than black / chemical industry.

He cited some specific examples, more detailed discussion of the application of options in the non-ferrous metal industry.

Case analysis

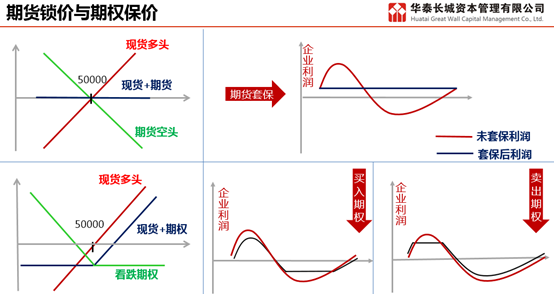

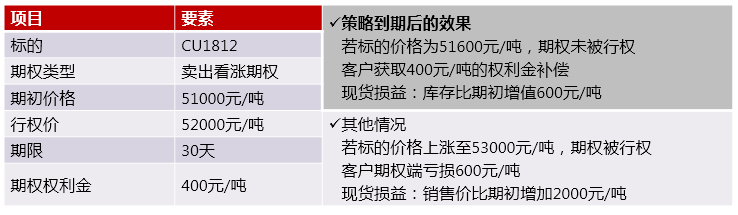

Inventory risk Management-sell call options

A copper smelter / trader holds inventory, the disk CU1812 price is 51000 yuan / ton;

The contradiction between supply and demand in the short term has eased, prices do not have the momentum to continue to soar, at the same time, it is difficult to fall sharply;

Option strategy: sell a call option with a 30-day exercise price of 52000 yuan per ton.

Risk tip: if prices rise sharply, customers need to make constant margin calls. If prices fall sharply, pay attention to timely sales or hedges at the spot end.

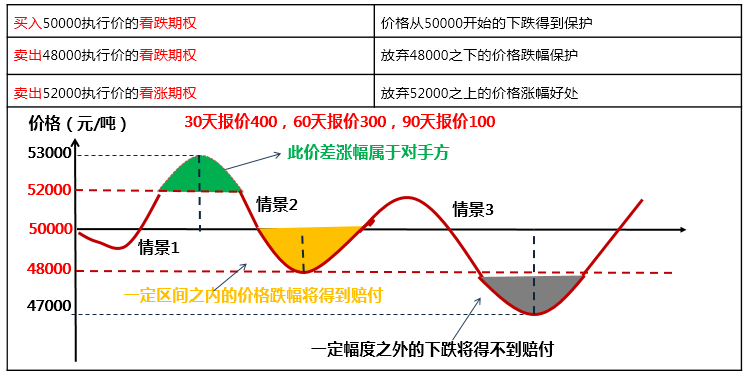

Inventory risk Management-Construction of trinomial put option portfolio

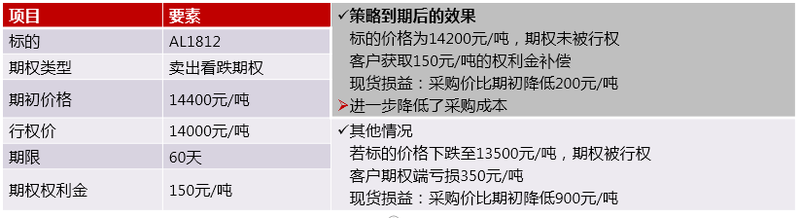

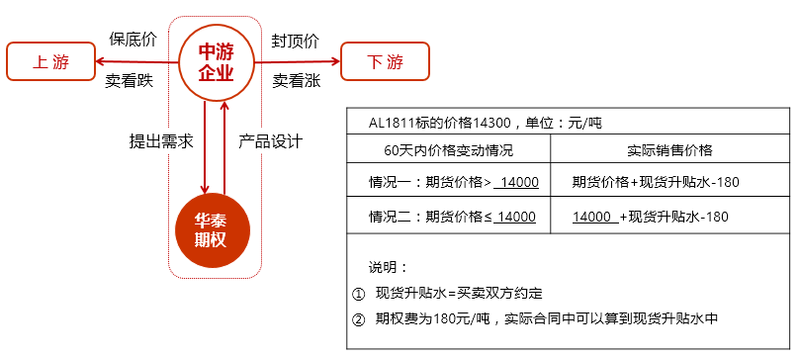

Order Raw material Purchasing risk Management-sell put option

A cable enterprise has won the bid order, the need to purchase raw material aluminum;

It is considered that the short-term fluctuation of aluminum price, if the price falls to 14000 yuan / ton, is willing to purchase raw materials in advance according to this price;

Sell false put options, the rights of about 150 yuan / ton, collect royalties to subsidize procurement costs.

Risk tip: a margin call is required if the price falls sharply. If the price rises sharply, we should pay attention to the timely purchase and replenishment of the goods.

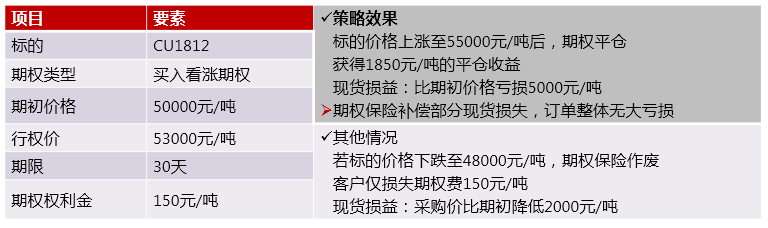

Order Raw material Purchasing risk Management-call option

A transformer enterprise has won the bid order, need to purchase raw material copper, the order price already contains 3000 yuan / ton raw material price increase safety margin;

It is considered that the copper price is uncertain, the macro is weak, the demand is general, there is the possibility of falling, at the same time, the inventory is on the low side, it is also possible to rise sharply.

Buy deep virtual call options as insurance, the payment of rights is about 150 yuan / ton.

Conclusion: no matter how much the price goes up, the customer's highest locked purchase price is 53000-150-53150 yuan / ton, while retaining the room for profit from the price fall.

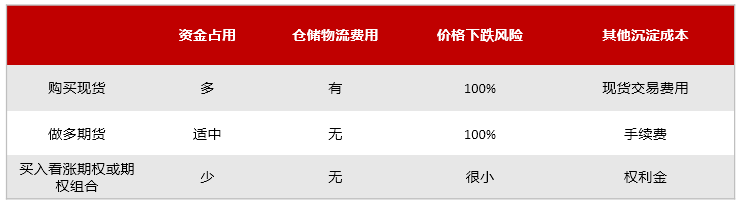

Risk Management characteristics of different tools

How do you choose when you judge that prices are going to go up?

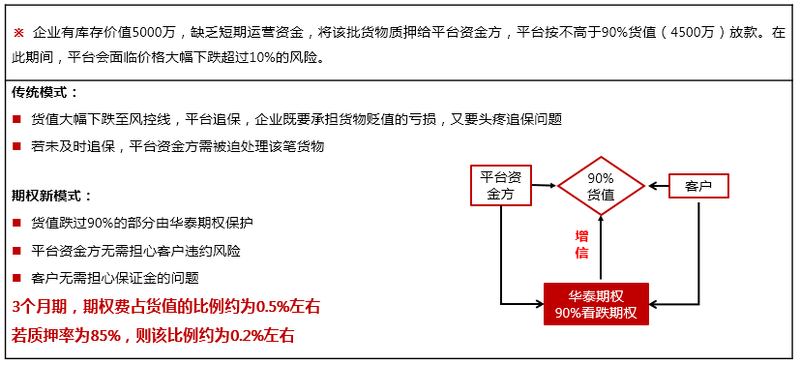

How does the option avoid the credit risk in the pledge financing of the right of goods?

Options also have other applications in cargo rights financing:

A downstream enterprise needs to purchase copper, but there is a lack of funds.

Assume that the reasonable cost of capital is 8%, but the enterprise subjectively feels that the fixed cost of capital is too high.

The following options are available:

The cost of capital is 6%, but if the price rises by more than 5%, downstream companies need to sell 30% of their profits.

Think about it: what kind of option is this? What is the combined cost?

Trade with rights

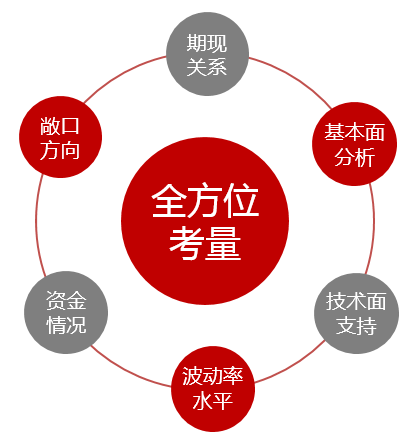

How to develop an effective hedge Strategy

The eye of the futures is the direction, the eye of the option is the fluctuation

Standardized set selection futures, personalized set selection options

Homeopathic arbitrage option

Choose options with small and large, with financial problems

Concussion option

Summary

Finally, Liu Dongdong made a summary of his operational experience. He believed that:

Call options recommend short-term low-frequency operations, timely appearance.

Put options recommend medium-term rolling operations and pay attention to stops or hedges.

From the absolute income point of view, the call option return is always smaller than the futures, but the yield point of view is not necessarily.

From the point of view of absolute risk, the risk of put option is always smaller than that of futures, but the relative risk is not necessarily.

Whether to "buy" or "sell" requires a comprehensive consideration of the odds of success and odds.

![Platinum Prices Stop Falling and Rebound, Spot Market Discounts Widen Slightly, Trading Muted [SMM Daily Review]](https://imgqn.smm.cn/usercenter/wDeWQ20251217171734.jpeg)

![Silver Price Corrective Rebound, Spot Parity Transactions Quietly Await Guidance [SMM Daily Review]](https://imgqn.smm.cn/usercenter/nQsOk20251217171736.jpg)